Credit: GRI Institute

Credit: GRI InstituteEuropean Real Estate Outlook H1 2026: Stability, Selectivity, and Geopolitical Risk

GRI Barometer results reveal shifting city rankings, sector preferences, and the strategic priorities shaping deployment across Europe’s property markets

March 4, 2026Real Estate

Written by:Rory Hickman

Executive Summary

As presented by Diego Tavares, Partner and Managing Director Europe at the GRI Institute, during Europe GRI 2026 - Winter Edition in London, our latest GRI Industry Barometer shows a European real estate market moving from caution towards a more expansion-focused phase.

Sentiment has improved since our last survey in September 2025, supported by expectations of stable inflation and interest rates, although geopolitical and political uncertainty have become the dominant risks shaping strategy.

Residential remains the leading area of opportunity, with continued interest in logistics and alternative sectors, and signs of selective recovery in offices. Madrid and London maintain their top positions, while investor attention broadens to selected growth markets.

The outlook for 2026 reflects firmer foundations and renewed momentum, but disciplined and selective capital allocation will be essential.

Sentiment has improved since our last survey in September 2025, supported by expectations of stable inflation and interest rates, although geopolitical and political uncertainty have become the dominant risks shaping strategy.

Residential remains the leading area of opportunity, with continued interest in logistics and alternative sectors, and signs of selective recovery in offices. Madrid and London maintain their top positions, while investor attention broadens to selected growth markets.

The outlook for 2026 reflects firmer foundations and renewed momentum, but disciplined and selective capital allocation will be essential.

Key Takeaways

- Investor sentiment has shifted from caution to calibrated expansion, supported by greater macro stability and clearer financing conditions.

- Geopolitical and political uncertainty have overtaken regulatory and financial constraints as the primary risks shaping strategy in 2026.

- Capital is concentrating on structurally supported sectors such as residential and logistics, while remaining highly selective across cities and other asset classes.

► Download the PDF of the 'GRI Barometer: European Real Estate Outlook H1 2026' report here.

► Top 10 Cities

The GRI Institute’s latest Barometer survey assessed 27 cities - including major European capitals and key regional hubs - capturing the preferences of senior real estate leaders attending Europe GRI 2026 - Winter Edition.

Although the results indicate a high degree of continuity at the top of the rankings, with the four most favoured investment destinations - Madrid, London, Lisbon, and Milan - remaining unchanged since the previous survey in September 2025, there have been some more notable shifts lower down the table.

Madrid - Iberia’s sustained momentum

Interest in Southern Europe, and particularly Iberia, continues to strengthen. Madrid is viewed as a leading European investment destination, and although certain headwinds persist, the city continues to benefit from Spain’s strong macroeconomic growth and EU-backed structural support, reinforcing overall investor confidence.Spain is widely perceived as a relative safe haven for international capital, supported by macroeconomic resilience and improving sector fundamentals.

The ongoing rebound in tourism since Covid is expected to continue into 2026, underpinning further growth in hospitality. Market participants also point to optimism around potential government reforms and a supportive investment environment.

London - Stability and sectoral rotation

London maintains its position as a global investment centre, underpinned by transparency, liquidity, and institutional depth. Investors highlight consistent stability in the market, even amid broader geopolitical and economic uncertainty.There is, however, a clear shift in focus towards alternative and operational asset classes, including PBSA, life sciences, and light industrial. Retrofit and repositioning opportunities are also attracting attention, and investors are seeking value through active asset management strategies.

Lisbon and Milan - Diverging trajectories

Despite sustained interest in Iberia, Lisbon’s popularity has declined. Having shared second place with London in September 2025, it now sits in a more distant third position. While fundamentals remain supportive, relative momentum appears to have moderated.Milan, previously closer to Lisbon five months ago, remains in fourth. Italy continues to attract increasing investor interest, particularly in hospitality and luxury residential, and there is an expectation that Italian real estate growth could outpace much of the rest of Europe.

However, market participants also highlight inherent complexity and execution risk in Italy, alongside a weak domestic market and high construction costs. While the Winter Olympics have generated positive sentiment and visibility, structural challenges remain a consideration for investors.

Warsaw and the rise of CEE

Reinforcing a broader trend of growing interest in Central and Eastern Europe (CEE), Warsaw recorded one of the most significant improvements in the survey. The city rose from seventh place in the previous poll to joint fourth alongside Milan, displacing Paris from the top five.Sentiment towards Warsaw is cautiously positive, supported by solid Polish GDP growth and tightening office supply, which is bolstering prime rents and strengthening landlords’ positions. The residential rental and logistics sectors remain robust.

Although challenges such as limited new development without pre-lets, ongoing cost pressures, and vacancy in secondary assets persist, Poland continues to outperform much of the CEE region, where the outlook is characterised by moderate growth, stabilising inflation, and selective investment recovery.

Paris - Selective opportunities amid structural constraints

Warsaw’s advance has seen Paris fall out of the top five destinations, pushing the French capital into sixth place in the rankings.While some investors view the current market as offering attractive entry points, particularly in the redevelopment of obsolete office buildings and in managed residential strategies, sentiment in France remains tempered by domestic political uncertainty, weak investment volumes, low returns, and limited liquidity outside prime assets in core locations.

Germany - Opportunities overshadowed by headwinds

Barcelona and Berlin fell to the seventh and eighth spots, respectively. In Barcelona, sustained demand reflects confidence in the city’s long-term fundamentals and its positioning as a gateway to the broader Spanish market.Berlin, however, now shares eighth place with two newcomers to the top 10 - Hamburg and Dublin - reflecting an increase in tied votes in this edition of the survey.

Meanwhile, Frankfurt has slipped from ninth place in September down to the sixteenth spot - a marked decline in relative popularity.

Most notably, Munich has fallen from tenth place in the previous barometer to receiving no votes at all in the latest survey - a result that stands out and warrants close attention in the coming quarters.

While Germany continues to generate international interest - particularly in residential, data centres, logistics, and adaptive reuse - market participants on the ground report significant headwinds.

These include a substantial debt refinancing gap, pricing disparities between buyers and sellers, risk-averse lending conditions, and regulatory constraints, all of which are limiting transaction volumes and new development.

Completing the rankings

Rounding out the list, Prague ranks eleventh, while Rome and Stockholm share joint twelfth place alongside the option of “other city”. The increased number of votes for “other city” reinforces a growing trend towards exploring secondary and alternative locations beyond the traditional core markets.Manchester follows in fifteenth place, showing a decline in investor interest compared to previous surveys. While still a significant market, the city's appeal appears to be waning.

Frankfurt and Copenhagen sit in sixteenth place, reflecting challenges within Germany and Denmark. Athens ranks eighteenth, with Brussels and Luxembourg tied for nineteenth. These cities continue to attract attention, though to a lesser extent compared to more prominent hubs.

Finally, Amsterdam, Budapest, and Helsinki occupy the bottom positions, with limited investor interest indicating that while they remain on the radar, they face significant barriers to competing with higher-ranked destinations.

► Investor Outlook

Appetite for growth in a stabilising environment

A central question emerging from this edition of the Barometer is whether there is genuine appetite for new projects and fresh investment commitments across Europe.The findings suggest that, while caution remains, the overall tone has shifted decisively towards expansion since our last survey.

Inflation and interest rates - Foundations of decision-making

Inflation and interest rates continue to be the two most influential variables shaping investor strategy.

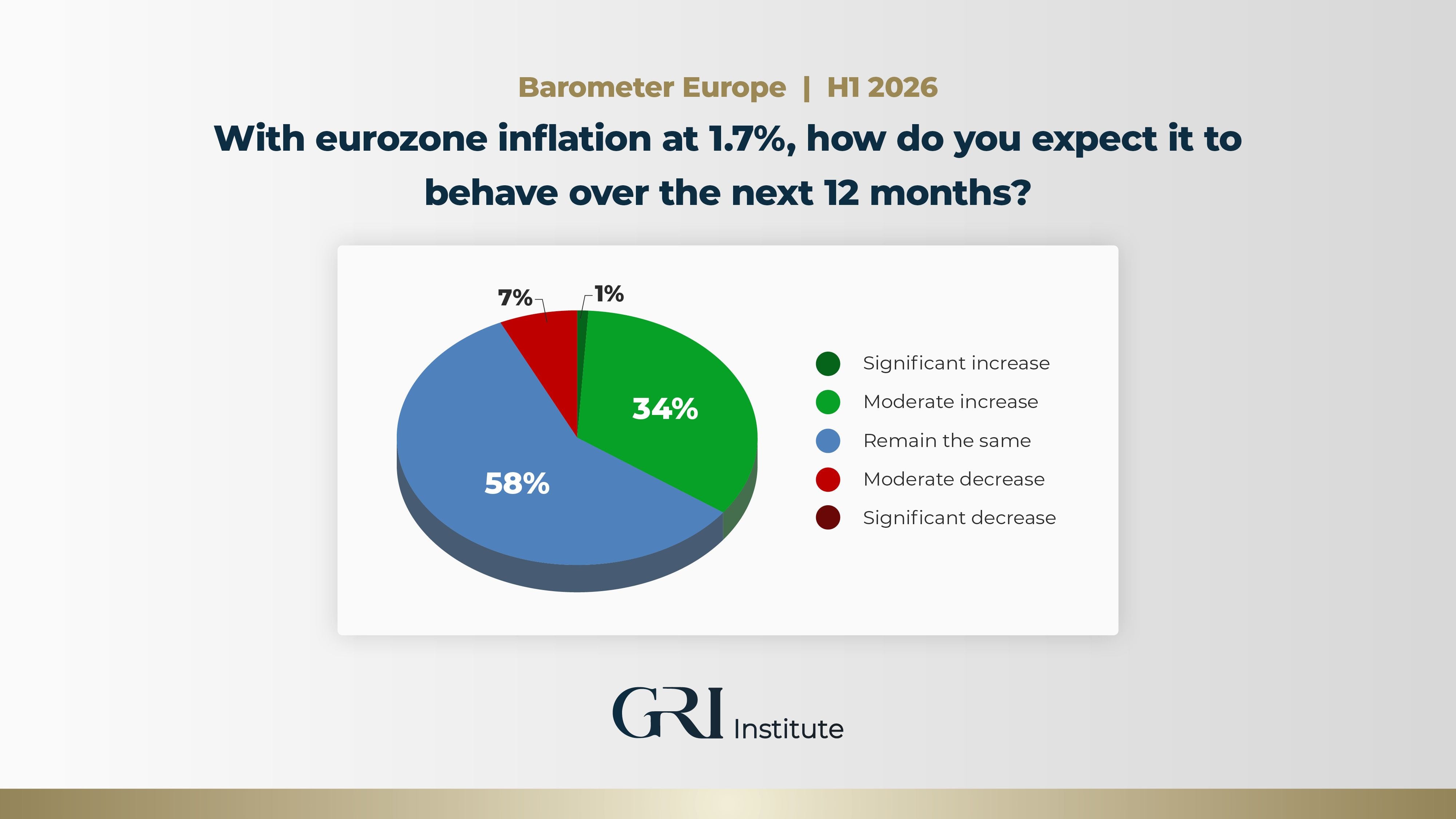

A majority of respondents - 58% - expect inflation to remain broadly stable over the next 12 months, while 34% anticipate a moderate increase. This suggests that, although inflationary pressures have not fully dissipated, most market participants believe the worst volatility is behind us.

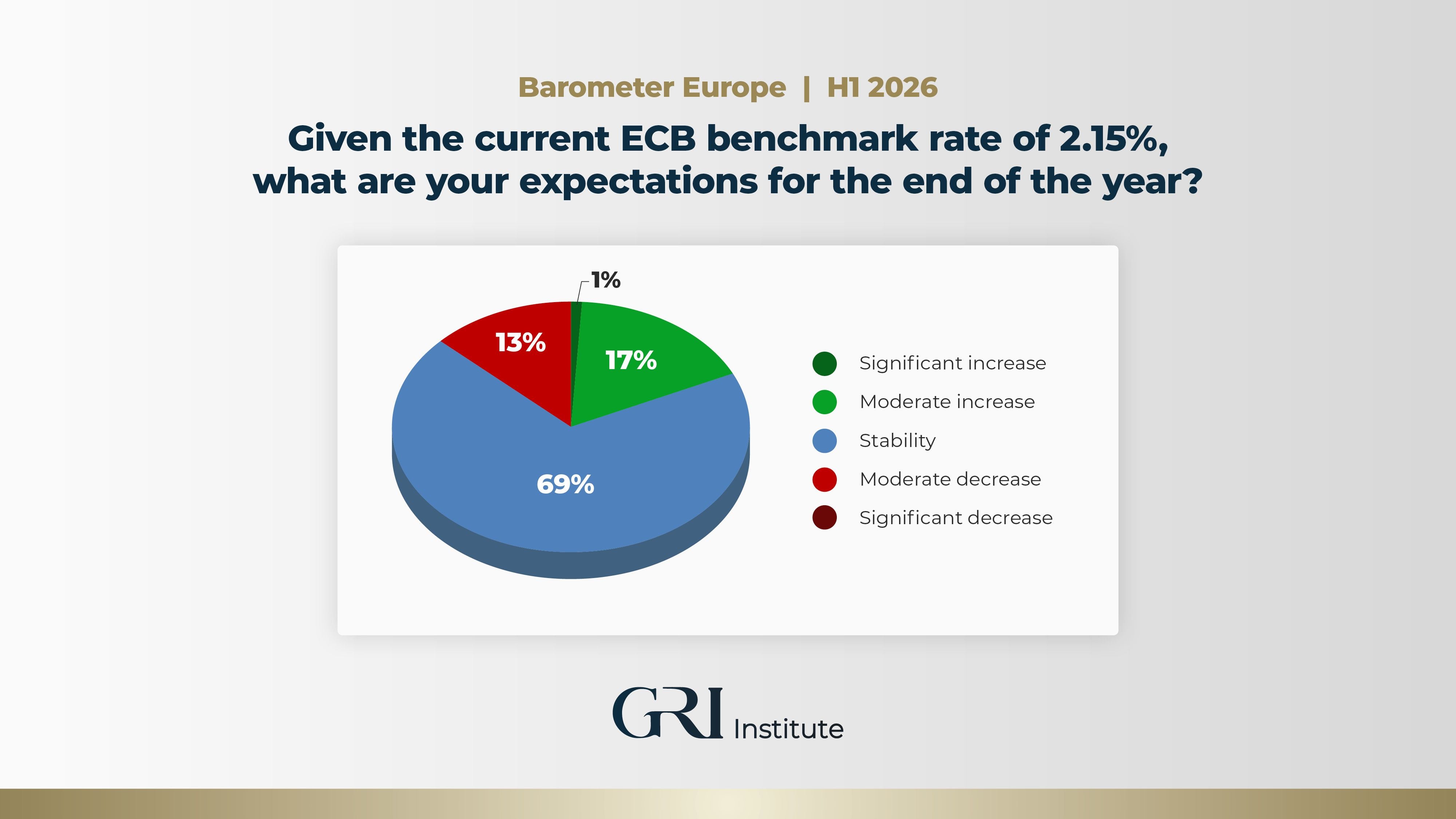

In parallel, 69% of respondents expect the European Central Bank (ECB) to maintain interest rate stability through to the end of 2026. This expectation of limited movement provides a more predictable financing backdrop, supporting underwriting assumptions and improving confidence in capital deployment.

Economic outlook - Stability with cautious optimism

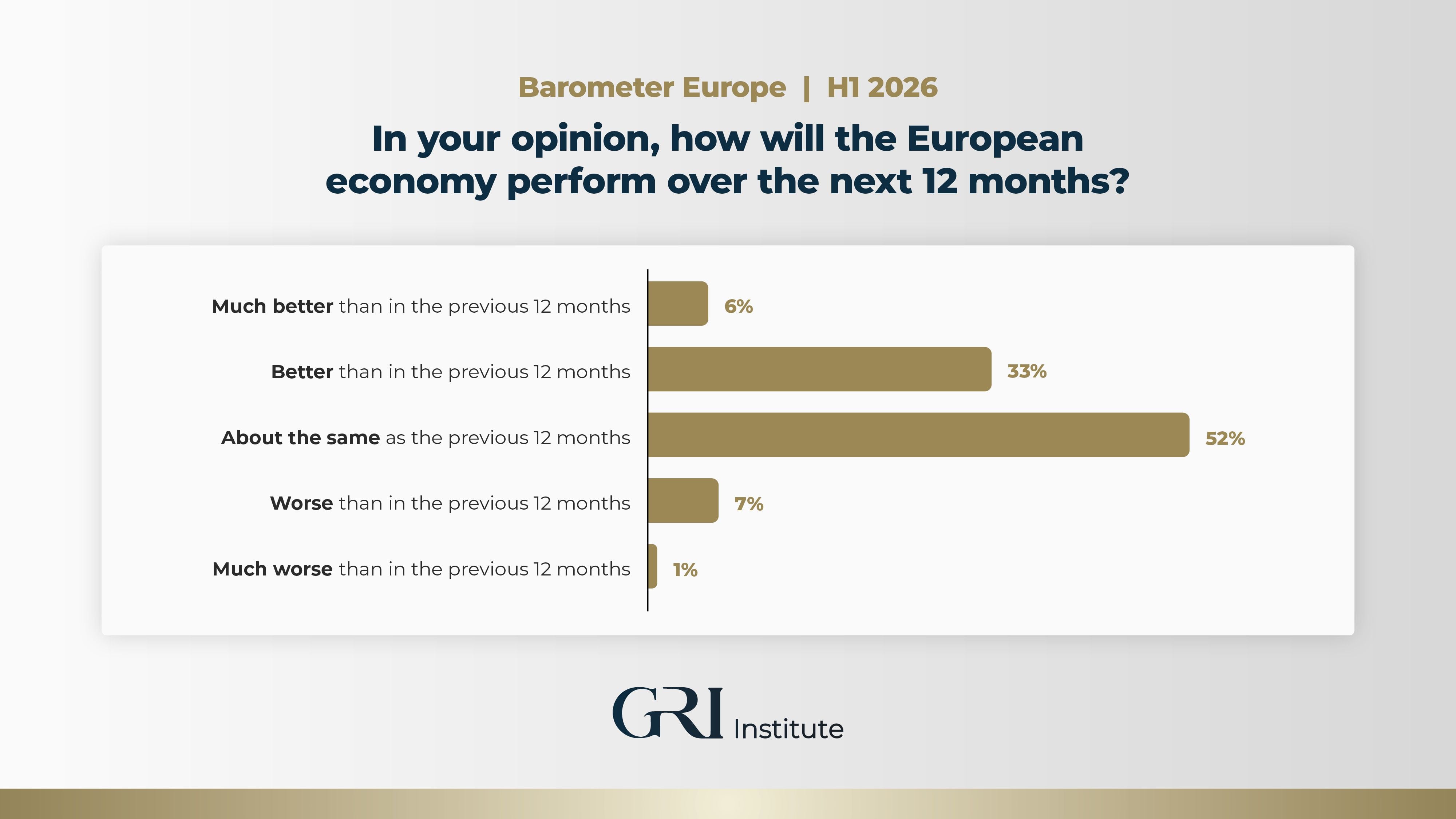

Looking at the broader European economy, sentiment is similarly steady. Over the next 12 months, 52% of decision-makers expect economic performance to be broadly in line with the previous year, while 39% anticipate an improvement.

Taken together, these figures point to a macro environment characterised by stability and cautious optimism rather than exuberance. For investors, predictability appears more important than rapid expansion.

Corporate strategy - A decisive shift towards growth

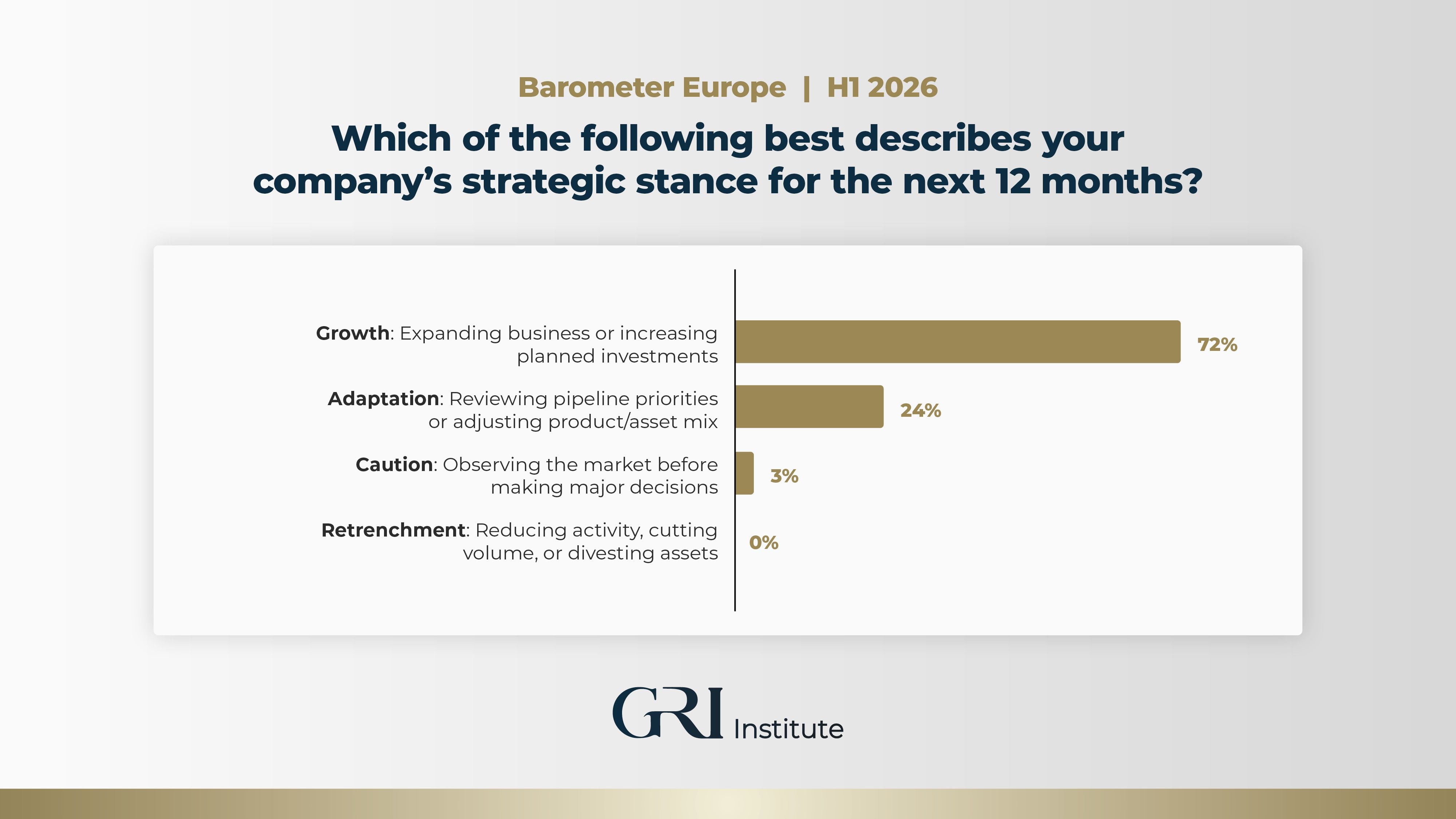

Within this context, company-level strategies have become notably more proactive.

Some 72% of respondents report that their organisations are prioritising growth - expanding business lines or increasing planned investments. A further 24% remain in adaptation mode, reviewing pipeline priorities or adjusting product and asset allocation strategies.

This marks a clear shift from September 2025, when a significant proportion of companies were maintaining existing plans or reassessing pipelines amid broader caution. In the latest survey, growth has become the dominant stance, while defensive or wait-and-see positions have reduced materially.

What could derail momentum?

Despite this constructive backdrop, investment appetite remains sensitive to external shocks.

The most significant potential disruptors identified by respondents include global geopolitical tensions, rising political uncertainty, and weak economic growth. Construction costs and inflation also remain relevant concerns, albeit to a lesser extent than in previous surveys.

Compared with September 2025 - when concerns were more evenly distributed across political uncertainty, geopolitical tensions, weak growth, financing conditions, and construction costs - the current results show a sharper concentration of risk perception around geopolitical tensions and political instability. These factors now clearly dominate the risk landscape.

Notably, traditional cost pressures such as inflation, financing, and construction appear less central to respondents’ thinking than before. This suggests that macro-political risk has overtaken purely economic or operational considerations as the primary influence on investment decisions over the next 12 months.

Supportive fundamentals with structural risks

Overall, the survey results suggest that European real estate leaders are operating in a more stable and predictable financial environment than in recent years. However, while economic fundamentals are broadly supportive, geopolitical and structural uncertainties continue to shape strategic decision-making and could quickly alter the trajectory of investment activity.► Sector Preferences

In addition to geographic preferences, this edition of the Barometer once again examined which asset classes investors consider to offer the most compelling opportunities today. The results point to a market that remains structurally driven, yet increasingly selective.

Investors continue to favour sectors supported by strong structural demand - particularly residential and logistics - while becoming more discerning in areas exposed to technological or macroeconomic risk.

Residential - Structural undersupply sustains dominance

The residential sector remains the clear frontrunner, with an even greater proportion of respondents selecting it as their number one opportunity compared with the previous survey.This sustained conviction is underpinned by a pan-European housing shortage and a persistent lack of affordable supply, set against continued demand growth. Structural imbalances across both ownership and rental markets continue to attract capital, particularly from long-term institutional investors.

That said, respondents also flag ongoing challenges. Regulatory intervention, rising construction costs, and labour shortages are constraining delivery and adding complexity to underwriting. While opportunities are abundant, execution risk remains a key consideration.

Alternatives - Strong fundamentals, marginal softening

Alternative assets retain their second place ranking, despite a slight decline in support compared with the last survey.Interest remains strong in PBSA, senior living, healthcare, and life sciences. Widespread undersupply continues to support the PBSA segment, while demographic trends - particularly Europe’s ageing population - underpin demand for senior living and healthcare-related assets.

Although life sciences is no longer viewed with the same post-pandemic intensity, it continues to attract interest as part of a broader appetite for niche and operationally driven sectors. Overall, alternatives remain attractive for investors seeking diversification and exposure to long-term structural drivers.

Logistics - Re-entering the top three

Logistics and warehousing have recorded one of the most notable improvements in this survey, rising from fifth place five months ago to enter the top three.This renewed momentum reflects sustained structural demand linked to e-commerce, supply chain optimisation, and last-mile delivery requirements. Investors also highlight the impact of technology and AI on warehousing efficiency and space utilisation.

Markets such as Spain, Germany, and parts of CEE are seen as particularly robust. Supply constraints in many locations continue to support rental growth and long-term fundamentals.

Data centres - High conviction, rising caution

Data centres have slipped to fourth place, accompanied by a discernible increase in investor caution since September.Global demand drivers remain compelling, including AI expansion, cloud computing growth, and digital infrastructure needs. The sector is also broadening beyond traditional FLAP-D markets, with new geographies emerging as viable hubs.

However, capital is increasingly pricing in risks related to regulation, power grid capacity, energy costs, land availability, financing structures, and technological obsolescence. Concerns about a potential AI-driven bubble have also tempered some of the more exuberant sentiment seen previously.

Hospitality - Positive fundamentals, softer sentiment

Despite expectations of continued tourism growth through 2026, the hospitality and hotels sector has slipped to fifth place.Tourism volumes have rebounded strongly post-Covid and are forecast to keep rising, particularly in Southern Europe. Investors continue to see opportunities in platform consolidation and operational value creation.

Nevertheless, concerns around potential oversaturation and new supply in certain markets appear to be moderating overall enthusiasm.

Offices - A notable resurgence

The office sector has staged a significant recovery in sentiment, climbing to sixth place after ranking last in the previous survey. It has overtaken both retail and infrastructure assets.The market remains highly bifurcated. Prime, well-located, and high-quality assets are performing relatively well, while secondary offices continue to struggle. Price misalignment between buyers and sellers is gradually improving, supporting selective transaction activity.

Spain, Italy, and the UK are viewed as comparatively stronger office markets, while Germany, France, and parts of CEE face greater challenges. Demand for flexible and co-working solutions is increasing, reflecting occupier adaptation to hybrid work models.

Retail - Polarised and selective

Retail continues to sit outside the majority of investors’ top priorities. The sector is increasingly polarised, with strong performance in selected cities and regions - notably in Spain and Italy - contrasted by ongoing weakness elsewhere.Prime high-street locations and retail parks are generally outperforming, while secondary assets face structural pressures. Given this uneven performance, retail remains a highly selective play.

Infrastructure - Falling to the bottom

Infrastructure has declined from sixth place in September to last position in the current rankings.While there is some crossover interest from real estate investors - particularly where infrastructure supports data centre requirements, such as energy supply and connectivity - it is not yet seen as a core focus for most respondents.

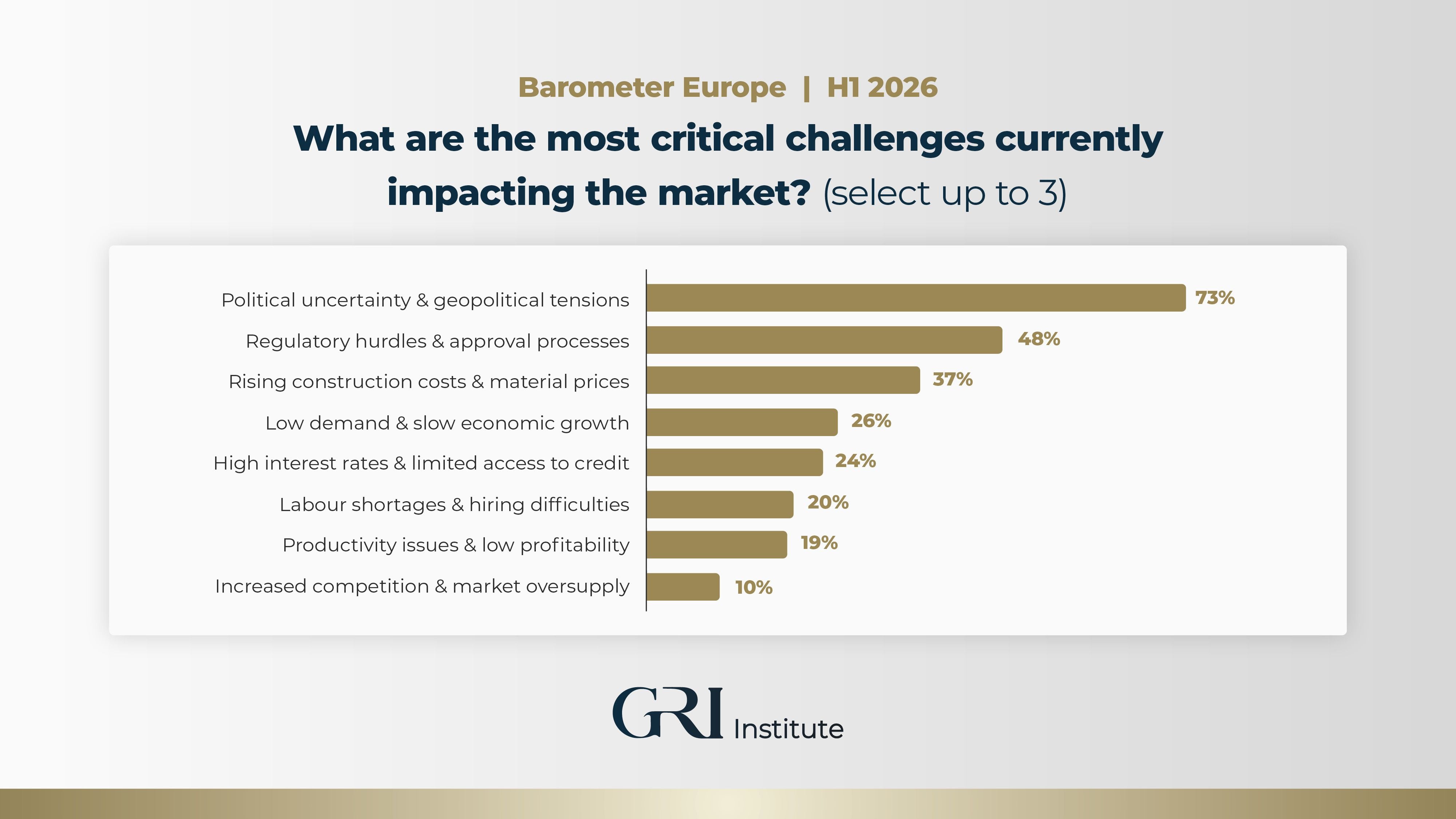

► Key Challenges

When assessing the most critical challenges currently impacting the European real estate market, this edition of the Barometer reveals a clear shift in priorities compared with September 2025.

Geopolitical risk moves decisively to the forefront

Political uncertainty and global geopolitical tensions are now the dominant concern, selected by 73% of respondents. This represents a marked rise in prominence and places macro-political risk firmly at the centre of investor thinking for 2026.In the previous survey, geopolitical and political uncertainty featured among the main concerns, but they did not lead the rankings. Their sharp ascent reflects a market increasingly shaped by global instability, trade tensions, electoral cycles, and broader systemic risks that extend beyond purely economic fundamentals.

The results suggest that investors are less preoccupied with operational constraints than with the potential for sudden, externally driven shocks.

Regulatory hurdles - Still critical, but no longer number one

Regulatory hurdles and approval processes now rank second, identified by 48% of respondents.In September 2025, regulation was the most significant obstacle, highlighted by 57% of participants. At that time, it was widely viewed as the primary bottleneck - slowing development timelines, increasing costs, and constraining the efficient execution of projects.

While regulatory complexity remains a substantial barrier in 2026, its relative importance has declined. This indicates that, although structural inefficiencies in planning and permitting persist, they are now overshadowed by broader macro-political uncertainties.

Construction costs - Easing, but still elevated

Rising construction costs and material prices are cited by 37% of respondents, placing them third in the ranking.In September 2025, construction costs were flagged by 49% of participants, reflecting the strong impact of inflationary pressures and supply chain disruptions at the time. The current lower percentage suggests that cost pressures, while still meaningful, are no longer escalating at the same pace and are becoming more predictable.

This aligns with broader survey findings indicating stabilising inflation expectations and improved financing visibility.

Financial constraints - Moderating concerns

Concerns around financial viability have eased compared with the previous survey.High interest rates and limited access to credit are now cited by 24% of respondents, down from 35% in September 2025. Similarly, productivity issues and low profitability, which previously concerned 40% of respondents, are now mentioned by 19%.

This shift suggests that financing conditions and margin compression, while still relevant, are perceived as less acute than six months ago. Greater clarity around monetary policy and improved pricing alignment may be contributing to this change in sentiment.

Demand, labour, and competition - Secondary but relevant

Low demand and slow economic growth are selected by 26% of respondents, broadly consistent with previous findings that positioned demand as a secondary challenge.Labour shortages and hiring difficulties are cited by 20%, indicating ongoing pressure in delivery capacity, albeit not at crisis levels.

Increased competition and market oversupply rank lowest, at 10%, suggesting that oversupply is not currently viewed as a systemic threat across most sectors or geographies.

A clear change in the risk landscape

Taken together, the comparison with September 2025 highlights a decisive evolution in the market’s perceived risk profile.Previously, the regulatory environment and financial constraints were seen as the most formidable barriers to progress. In 2026, the focus has shifted outward. Macro-political instability now dominates the narrative, while traditional cost, financing, and profitability concerns have receded in relative importance.

This transition underscores a market that is becoming more comfortable with economic and operational conditions, but increasingly alert to geopolitical volatility and political disruption as the principal variables that could reshape investment decisions in the year ahead.

► C-Circle Conclusions

Growth returns, but risk has shifted

The latest GRI Institute Barometer points to a European real estate market that has regained a degree of balance after several years of volatility.More stable expectations around inflation and interest rates have improved visibility, enabling companies to pivot from caution towards expansion. Growth is firmly back on the agenda, supported by clearer pricing, more predictable financing conditions, and renewed strategic conviction.

From a geographic perspective, capital continues to concentrate in markets perceived as transparent, liquid, and economically resilient. Iberia’s sustained appeal, London’s institutional depth, and Warsaw’s upward momentum reflect a search for relative stability combined with growth potential.

The growing presence of secondary and emerging cities in the rankings suggests that investors are broadening their lens, but doing so selectively.

At the sector level, structurally supported themes - particularly residential and logistics - remain central, while investors are more disciplined in segments exposed to technological or supply-side risks. The recovery in sentiment towards offices further reflects a market adjusting to repricing and differentiation.

The most notable change lies in the risk landscape. Operational and financing pressures have eased in relative importance, replaced by heightened concern around geopolitical and political instability. In the current environment, investors apparently feel more comfortable managing asset-level and economic variables, but remain highly alert to external shocks.

Overall, 2026 has begun with firmer foundations and a constructive outlook. However, disciplined capital allocation, selectivity, and active management will be critical in navigating an environment where macro-political risk now shapes the boundaries of opportunity.

GRI Barometer results for H2 2026 will be revealed at Europe GRI 2026 - Summer Edition in Paris on September 9-10.