GRI Institute

GRI InstituteBeyond the Banks: Mastering the Capital Stack in Europe's New Real Estate Debt Reality

GRI Credit Opportunities & RE Debt: Non-bank lending strategies, capital stack evolution, and confronting the refinancing wall

December 5, 2025Real Estate

Written by:Helen Richards

Executive Summary

This Conference Spotlight report offers exclusive, high-level insights from the European real estate credit and debt market, drawing directly from closed-door discussions at the GRI Credit Opportunities & Real Estate Debt 2025 conference in London, as well as an exclusive survey providing a snapshot of prevailing market player sentiment and strategic intent. Insights reveal how private credit and debt funds are becoming mainstream, offering flexible, relationship-focused capital stack strategies, with a strong preference for resilient sectors including "beds, sheds, and meds" (living, logistics, and medical real estate).

Key Takeaways

- The European real estate finance market has structurally evolved, with private credit and debt funds becoming mainstream to fill gaps left by traditional banks due to post-GFC regulation.

- Lenders are shifting from traditional mezzanine debt to the more efficient whole loan structure, often employing back-leverage to boost returns, maintain control, and offer competitive pricing.

- Despite a massive refinancing wall, market default risk is mitigated by high liquidity from banks and diverse non-bank lenders, though the eventual trigger for asset sales is expected to be the equity cycle and fund maturity issues.

Download the PDF of this 'GRI Credit Opportunities & RE Debt Spotlight' report here.

Navigating Real Estate Credit & Debt Cycles - How Are Global Players Positioning Across Markets, Sectors, and the Capital Stack?

The Evolving Real Estate Financing Landscape

The market has structurally evolved, with private credit and debt funds becoming mainstream and filling gaps left by traditional banks, a change largely driven by post-Global Financial Crisis (GFC) regulation intended to reduce risk in the banking system.While bank balance sheets remain significantly larger, banks are becoming more cautious and focusing on capital requirements, creating opportunities for non-bank lenders to provide flexible financing across the capital stack, including stretch loans and transitional loans.

This shift is seen as beneficial for the stability of the financial system because the failure of a highly-leveraged debt fund would typically result in unhappy investors rather than a systemic financial crisis like those caused by banks.

Debt Positioning and Investment Strategies

Lenders are increasingly adopting flexible capital strategies to create longer-term relationships with sponsors, particularly through active financing that evolves as a project matures, such as funding construction, lease-up, and stabilisation phases.The most successful deals are viewed as those where the underlying real estate is enduring and has a clear exit path to a desirable asset, though some lenders prioritise long-term, durable cash flows and coverage ratios over the final exit valuation due to market cyclicality.

There is a noted trend of leveraged debt funds using back leverage to boost returns, particularly in the whole loan or senior debt space, reflecting a growing complexity in how risk is priced and structured.

Preferred Real Estate Sectors

Debt capital is heavily favouring sectors with strong occupational demand and robust cash flows, often summarised as "beds, sheds, and meds," which includes the entire living sector (residential, student housing, co-living), logistics, and medical-related real estate (life sciences, healthcare, senior living).The residential and logistics sectors are highlighted for their low vacancy rates and strong rental growth, driven by supply constraints and migration into metropolitan areas.

While office development is currently constrained by a lack of equity, prime Grade-A assets in core cities are still seen as investable, and a return to retail lending has been observed where resilient cash flows and high cap rates provide attractive risk-adjusted returns.

Geographical Preferences

Continental Europe is a strong focus for debt deployment, driven by a recent recalibration of interest rates that has kept core underwriting returns at healthy spreads above swap rates and created white space due to reduced bank activity.The UK market is approached more selectively due to a combination of higher interest rates and a transitional macroeconomic backdrop. The most attractive opportunities exist in large metropolitan cities across the continent and the UK where a massive supply-demand gap exists, particularly in the living sector.

The Refinancing Wall and Distress Opportunity

The market is facing a significant wave of loan maturities that will undoubtedly put many borrowers under severe stress, particularly those who were highly levered based on the past low interest rates and now face the current higher rates.However, this cycle is expected to be more benign than the GFC as banks are better capitalised and have been provisioned early due to regulatory changes, allowing them to manage losses over time rather than being forced into a sudden fire sale of non-performing loans (NPLs).

This creates a long-term opportunity for both equity and debt to engage in complex, time-consuming discussions with developers and sponsors to find creative structures for refinancing and providing capital.

(Credit: GRI Institute)

Private Credit Surge - Is Non-Bank Lending the New Normal?

Evolving Role of Non-Bank Lenders Post-GFC

The rise of non-bank lending is seen as a key shift, notably accelerating post-GFC and driven in part by a big push into Europe from US-based debt funds and insurance businesses.

While banks remain significant, there is a historically high flux of capital into non-bank lending and diversification of the marketplace, which has forced banks to partner more frequently with non-bank entities.

The perception of borrowing from non-bank firms has moved from initial wariness to an accepted, even common, practice in the last decade.

The Impact of Back Leverage and Rising LTVs

The use of back leverage is a key element for non-bank lenders to create returns for their investors, often by financing whole loans taken down by the firm. This mechanism allows non-bank lenders to offer more competitive pricing and has contributed to an upward nudge in leverage, with loan-to-value (LTV) ratios increasing from a maximum of 70% to almost 75% as a new standard in some deals.

Despite this, some market players express increasing caution and prudence around risk, resulting in a higher turn-down rate for deals not meeting their leverage asks.

Despite this, some market players express increasing caution and prudence around risk, resulting in a higher turn-down rate for deals not meeting their leverage asks.

Increased Collaboration and Partnerships

There is an increasing trend of collaboration between non-bank lenders and traditional banks, as well as between different non-bank firms, to address the evolving needs of the market.

Partnerships such as those between large funds and mid-market lenders, or high street banks and non-bank capital providers, are becoming more common in order to access specific segments, such as the middle market, or manage the size of large transactions.

This collaboration is often facilitated by the increasing availability of long-term "core-capped" capital, which has a risk profile more aligned with traditional lending.

Partnerships such as those between large funds and mid-market lenders, or high street banks and non-bank capital providers, are becoming more common in order to access specific segments, such as the middle market, or manage the size of large transactions.

This collaboration is often facilitated by the increasing availability of long-term "core-capped" capital, which has a risk profile more aligned with traditional lending.

Optimistic Outlook for Market Volume and Product Diversification

Despite the current competitive and challenging environment for raising equity, market players are showing optimism for the coming year, expecting an increase in investment volumes, particularly acquisition activity, which has been lagging.

The market anticipates a recycling of capital, with refunds from older, high-leverage loans potentially being reinvested into new acquisitions.

Furthermore, there is a strong expectation for continued growth in structured products like CRE-CLOs (Commercial Real Estate Collateralised Loan Obligations) and synthetic securitisation in Europe, as a necessary means of capital markets activity and back leverage as the private credit space continues its expansion.

The market anticipates a recycling of capital, with refunds from older, high-leverage loans potentially being reinvested into new acquisitions.

Furthermore, there is a strong expectation for continued growth in structured products like CRE-CLOs (Commercial Real Estate Collateralised Loan Obligations) and synthetic securitisation in Europe, as a necessary means of capital markets activity and back leverage as the private credit space continues its expansion.

(Credit: GRI Institute)

(Credit: GRI Institute)Mid-Market - Hidden Gems or Hidden Risks?

Pricing Pressure and Differentiation

The increase in base rates made alternative credit competitive with banks, but banks are now re-entering the senior debt space with lower margins (below 220 basis points) and increasing their risk appetite, which is creating pricing pressure for alternative lenders.

To offset this, alternative lenders are differentiating themselves by focusing on superior service, speed of execution, and flexibility in structuring deals for SME or mid-market developers, rather than simply competing on the highest leverage.

To offset this, alternative lenders are differentiating themselves by focusing on superior service, speed of execution, and flexibility in structuring deals for SME or mid-market developers, rather than simply competing on the highest leverage.

Sectoral Opportunities and Risk Approach

Lenders have been known to be sector agnostic, but the consensus suggests opportunities lie where liquidity is constrained and where an asset’s strong fundamentals offer attractive risk-adjusted returns.

Residential development, logistics, convenience retail, and niche living spaces are generally favoured. Meanwhile, high street retail and regional offices are seen as challenging, though some believe prime offices are oversold and present opportunities.

Some firms, particularly in Central and Eastern Europe (CEE), proactively adopt a junior lender position, such as mezzanine debt, to capitalise on market dynamics by de-risking the deal through careful timing, for example, stepping in only after a residential project has permits and significant pre-sales.

Residential development, logistics, convenience retail, and niche living spaces are generally favoured. Meanwhile, high street retail and regional offices are seen as challenging, though some believe prime offices are oversold and present opportunities.

Some firms, particularly in Central and Eastern Europe (CEE), proactively adopt a junior lender position, such as mezzanine debt, to capitalise on market dynamics by de-risking the deal through careful timing, for example, stepping in only after a residential project has permits and significant pre-sales.

Challenges to Scalability and Technology

A significant barrier to growth and scalability is sourcing deals in a market with increasing liquidity and a limited number of transactions. To manage growth, especially with limited personnel, there is a strong focus on technology and AI to improve throughput and capacity.

Firms are investing heavily in bespoke in-house systems to automate the front-end process, from ingesting borrower information for credit underwriting to managing risk and quarterly reporting, as off-the-shelf solutions are often deemed insufficient or pose a risk of sharing proprietary business strategy.

Firms are investing heavily in bespoke in-house systems to automate the front-end process, from ingesting borrower information for credit underwriting to managing risk and quarterly reporting, as off-the-shelf solutions are often deemed insufficient or pose a risk of sharing proprietary business strategy.

Macroeconomic Risks and Market Uncertainty

Macroeconomic and political uncertainty are significant factors in underwriting, making long-term predictions challenging. Specific concerns include the impact of AI on demand for regional office real estate, the effect of driverless cars on commuting patterns and housing demand outside London, and the political instability in the UK.

Despite these risks, the demand for capital is high, and the consensus among market players is to remain prudent and cautious in underwriting deals to ensure they can withstand future market stress.

Despite these risks, the demand for capital is high, and the consensus among market players is to remain prudent and cautious in underwriting deals to ensure they can withstand future market stress.

Future Focus and Outlook

The market is anticipated to be extremely busy in 2026, comparably more so than 2025, due to the large number of debt maturities requiring refinancing.

Given the challenges in development and construction costs, there is a strong belief that rental growth will become a main factor in property value, as a lack of future supply may drive up rents.

The mid-market is poised for continued fragmentation and dislocation, providing ongoing opportunities for agile private credit lenders.

Given the challenges in development and construction costs, there is a strong belief that rental growth will become a main factor in property value, as a lack of future supply may drive up rents.

The mid-market is poised for continued fragmentation and dislocation, providing ongoing opportunities for agile private credit lenders.

(Credit: GRI Institute)

Capital Stack Strategies - Senior, Mezz, Pref… What Works Now?

Shift from Mezzanine Debt to Whole Loans with Back-Leverage

The market has seen a decline in the viability of the traditional mezzanine debt structure, primarily due to intense competition from non-bank vendors and the rise of whole loan financing strategies.

Many debt funds are now favouring the whole loan approach, where they provide the entire loan and then finance a portion of it internally using back-leverage facilities, as this structure is more efficient for deploying large amounts of capital and allows the lender to retain full control over the deal and the borrower relationship.

The whole loan model is seen as a way to generate commensurate returns without the complications of negotiating a separate subordinate position or dealing with a disparate group of lenders.

Many debt funds are now favouring the whole loan approach, where they provide the entire loan and then finance a portion of it internally using back-leverage facilities, as this structure is more efficient for deploying large amounts of capital and allows the lender to retain full control over the deal and the borrower relationship.

The whole loan model is seen as a way to generate commensurate returns without the complications of negotiating a separate subordinate position or dealing with a disparate group of lenders.

Importance of Relationships and Execution Certainty

Despite the highly competitive and price-sensitive market, relationships remain paramount for both lenders and borrowers.

For borrowers, the choice of lender is not solely based on price, but also on execution certainty - the assurance that the lender, even one utilising back-leverage, can reliably and promptly deliver the committed funding without internal delays.

Lenders leverage their strong relationships with syndication partners, back-leverage providers, and their underlying sponsors to create a competitive advantage and a seamless, bilateral experience for the borrower.

For borrowers, the choice of lender is not solely based on price, but also on execution certainty - the assurance that the lender, even one utilising back-leverage, can reliably and promptly deliver the committed funding without internal delays.

Lenders leverage their strong relationships with syndication partners, back-leverage providers, and their underlying sponsors to create a competitive advantage and a seamless, bilateral experience for the borrower.

Increased Rigour in Underwriting Standards

The industry has witnessed a pronounced increase in the rigour of underwriting standards, a trend significantly influenced by the lessons learned from past financial crises.

Lenders are moving away from relationship-based lending that sometimes compromised credit quality, focusing instead on a meticulous, asset-driven approach. This involves extensive due diligence by internal experts, including project monitors and sector specialists, to stress-test all possible scenarios and build a high conviction on the underlying asset and business plan to ensure the ultimate return of capital.

Lenders are moving away from relationship-based lending that sometimes compromised credit quality, focusing instead on a meticulous, asset-driven approach. This involves extensive due diligence by internal experts, including project monitors and sector specialists, to stress-test all possible scenarios and build a high conviction on the underlying asset and business plan to ensure the ultimate return of capital.

Demand for Transparency and Control

There is a growing demand from both debt providers and borrowers for greater transparency across the capital stack, particularly regarding the pricing and allocation of returns.

Lenders seek to maintain control over the loan structure, which is a major driver behind the adoption of whole loans with back-leverage, as this allows the debt fund to be the sole point of contact and decision-maker with the borrower.

This is countered by the borrower's desire for transparency on who is ultimately invested in their deal and the terms of the full debt stack.

Lenders seek to maintain control over the loan structure, which is a major driver behind the adoption of whole loans with back-leverage, as this allows the debt fund to be the sole point of contact and decision-maker with the borrower.

This is countered by the borrower's desire for transparency on who is ultimately invested in their deal and the terms of the full debt stack.

(Credit: GRI Institute)

Southern Europe - Is Southern Resilience Paying Off?

Southern Europe's Sustainable Resilience

The resilience of the Southern European market is transitioning from a purely opportunistic phase to a more institutional and structural one, supported by strong demand and increasing capital allocation to private credit strategies.

While the market remains cyclical, the growing acceptance of alternative lenders and the deployment of capital into markets like Spain, Portugal, and Italy suggest a sustained, positive outlook for the next few years.

While the market remains cyclical, the growing acceptance of alternative lenders and the deployment of capital into markets like Spain, Portugal, and Italy suggest a sustained, positive outlook for the next few years.

Alternative Lenders: Filling the Banking Gap

The growing and structural role of alternative lenders is being cemented as they fill the financing gaps left by traditional commercial banks, which are becoming more selective and less aggressive in their lending due to regulatory pressure and a focus on safer assets.

Alternative lenders offer speed, flexibility, and the ability to finance higher-leverage and special situations - a necessity for sponsors, even if it means a higher cost.

This has led to a perceived “parallel road” where alternative lenders are not directly competing with banks for the same deals, but rather replacing the function of private equity by offering debt financing in exchange for a smaller piece of a project's final return.

Alternative lenders offer speed, flexibility, and the ability to finance higher-leverage and special situations - a necessity for sponsors, even if it means a higher cost.

This has led to a perceived “parallel road” where alternative lenders are not directly competing with banks for the same deals, but rather replacing the function of private equity by offering debt financing in exchange for a smaller piece of a project's final return.

Italy: The International Capital Proposition

Italy's investment market is seen as a relative value proposition, heavily reliant on international capital for equity and alternative lending, especially as the banking industry consolidates and local banks focus on a narrow range of lower-risk transactions.

The market is considered less crowded than Spain, with good opportunities due to its size and relatively strong economy, offering appealing risk-adjusted returns for investors willing to manage the inherent complexities.

There is a noted trend towards high-yield strategies, particularly in residential development in areas like Milan, rather than pure opportunism.

The market is considered less crowded than Spain, with good opportunities due to its size and relatively strong economy, offering appealing risk-adjusted returns for investors willing to manage the inherent complexities.

There is a noted trend towards high-yield strategies, particularly in residential development in areas like Milan, rather than pure opportunism.

Portugal's Institutional Hurdles and Scale Issues

Portugal presents significant challenges on its path to becoming a fully institutional market, primarily due to a lack of domestic liquidity and an ineffective banking system that had been over-leveraging projects with zero equity.

While the slowdown of bank activity is creating more space for alternative lenders to step in, the country is currently viewed as a small market that lacks the necessary scale and critical mass to attract major international institutional investors, such as large US fund managers. Furthermore, investors in Portugal are also frustrated by long licensing processes that prevent capital deployment.

While the slowdown of bank activity is creating more space for alternative lenders to step in, the country is currently viewed as a small market that lacks the necessary scale and critical mass to attract major international institutional investors, such as large US fund managers. Furthermore, investors in Portugal are also frustrated by long licensing processes that prevent capital deployment.

Market Maturation and Tightening Returns

The tightening competition and returns for alternative lenders across Europe mean that more capital is looking towards less crowded markets like Italy as a relative value proposition.

The influx of newcomers is putting pressure on returns, with the expected double-digit returns seen before the summer now shifting to the single-digit space, indicating a maturing and more competitive lending environment.

The influx of newcomers is putting pressure on returns, with the expected double-digit returns seen before the summer now shifting to the single-digit space, indicating a maturing and more competitive lending environment.

(Credit: GRI Institute)

Germany - Recovery, Repricing, or Retreat?

Disconnection Between Valuations and Transaction Prices

A major hurdle for increasing German real estate market activity is the significant disconnect between current asset valuations and the price level at which transactions could realistically occur.

Buyers, including those looking for value-add or core-plus opportunities, couldn't act previously because of interest rates and uncertainty, and sellers are now reluctant to transact at the necessary 50% to 60% discounts seen in some smaller or distressed development deals.

This is compounded by the lagging German long-term valuation process, which makes it hard for open-ended funds to justify selling without first bringing their book valuation down.

Buyers, including those looking for value-add or core-plus opportunities, couldn't act previously because of interest rates and uncertainty, and sellers are now reluctant to transact at the necessary 50% to 60% discounts seen in some smaller or distressed development deals.

This is compounded by the lagging German long-term valuation process, which makes it hard for open-ended funds to justify selling without first bringing their book valuation down.

Bank Reluctance and Workout Scenarios

German mortgage banks, despite seeing their workout departments double or triple in size, are generally avoiding putting a lot of NPLs or enforcement-related assets onto the market.

They often prefer to sit on difficult positions and grant loan extensions - sometimes even into a fifth extension for development deals - rather than take the large write-downs that would be necessary. The pressure to take these write-downs is only slowly beginning to increase.

They often prefer to sit on difficult positions and grant loan extensions - sometimes even into a fifth extension for development deals - rather than take the large write-downs that would be necessary. The pressure to take these write-downs is only slowly beginning to increase.

Shift to Alternative Asset Classes and Operations

Investor interest is moving away from the historically dominant office market towards alternative asset classes, which are seen as providing better risk-adjusted returns. These new focus areas include residential, data centres, self-storage, and senior living.

A common theme in these classes is the importance of operational leverage, where active, intelligent management is used to secure extremely high rents per square metre compared to traditional industrial or residential spaces.

A common theme in these classes is the importance of operational leverage, where active, intelligent management is used to secure extremely high rents per square metre compared to traditional industrial or residential spaces.

Financing Competition and Margins

In the high-liquidity, high-quality end of the market, competition between banks has returned, with margins for core office deals once again becoming extremely tight.

To compete, private debt funds must employ back leverage as a financing strategy, allowing them to offer whole loans at very low margins on high-leverage transactions while still meeting the high return expectations of their capital providers.

However, this low-cost financing is not readily available for value-add projects or those with complex structures, leaving a gap in the market.

To compete, private debt funds must employ back leverage as a financing strategy, allowing them to offer whole loans at very low margins on high-leverage transactions while still meeting the high return expectations of their capital providers.

However, this low-cost financing is not readily available for value-add projects or those with complex structures, leaving a gap in the market.

The German Capital and Regulatory Hurdle

The flow of German domestic capital is severely constrained, as many traditional local investors, such as professional pension schemes, have already over-allocated to real estate and lending, with their capital being effectively "spent".

Furthermore, German lenders are not currently playing in the back leverage space due to regulatory requirements that prevent them from receiving the necessary beneficial capital treatment.

This regulatory difference means that international capital is often the driving force in supporting new, riskier, or alternative finance structures.

Furthermore, German lenders are not currently playing in the back leverage space due to regulatory requirements that prevent them from receiving the necessary beneficial capital treatment.

This regulatory difference means that international capital is often the driving force in supporting new, riskier, or alternative finance structures.

(Credit: GRI Institute)

Cross-Border Lending - Where Is Financing Flowing Most Actively and How Are Lenders Using Diverse Capital Stack Layers Across Regions?

European Geographic Hotspots and Investment Sectors

Spain is currently considered a very attractive market, particularly for hospitality assets such as hotels, with significant interest and capital - mostly American - driving up prices and creating a beneficial climate for international investors.

Other actively targeted markets include Italy and the UK, with the latter offering a sophisticated environment despite its challenges. There is also growing activity in Ireland, where government policy changes are making the living sector more attractive.

Lenders are increasingly sector-agnostic but find good opportunities in non-traditional real estate assets like cold storage and data centres, especially where there is less competition and high barriers to entry.

Other actively targeted markets include Italy and the UK, with the latter offering a sophisticated environment despite its challenges. There is also growing activity in Ireland, where government policy changes are making the living sector more attractive.

Lenders are increasingly sector-agnostic but find good opportunities in non-traditional real estate assets like cold storage and data centres, especially where there is less competition and high barriers to entry.

The Criticality of Local Knowledge and Deal Size

When lending abroad, local knowledge is paramount for navigating differing legal and administrative processes. For instance, Italy presents structural complexities related to syndication, securitisation rules, and setting up the deal, requiring extra time and effort.

To make the effort of cross-border lending worthwhile, especially with the increased complexity, lenders often require a larger transaction size than they may accept domestically.

The UK remains a preferred destination due to the high level of comfort international capital has with its property laws and ease of business.

To make the effort of cross-border lending worthwhile, especially with the increased complexity, lenders often require a larger transaction size than they may accept domestically.

The UK remains a preferred destination due to the high level of comfort international capital has with its property laws and ease of business.

Enforcement Realities and Challenges

While the UK's property laws are lauded for providing a quick and secure route to enforcement, the practical reality of enforcement in Europe often involves a cooperative approach from borrowers, particularly in the post-COVID environment, where sponsors often willingly hand over the asset to the lender as a last resort.

The legal route to enforcement is highly variable across Europe. For lenders, it is essential to understand what this route would be, even if it is unlikely to be used.

The legal route to enforcement is highly variable across Europe. For lenders, it is essential to understand what this route would be, even if it is unlikely to be used.

Exploring Frontiers Beyond Europe

While Europe remains the primary focus, there is increasing pressure and discussion around lending in markets beyond Europe, with the Gulf Cooperation Council (GCC) nations being a notable point of interest due to their booming economies and large-scale projects.

The biggest deterrent for many institutional lenders in nations like Saudi Arabia is the uncertainty of enforcement, which is seen as a material risk due to potential political interference or lack of established legal precedent for international capital.

Other markets, including Japan, India, and Eastern Europe are also on the radar, but these present different challenges, such as tight cap rates in Japan or significant complexity in India.

The biggest deterrent for many institutional lenders in nations like Saudi Arabia is the uncertainty of enforcement, which is seen as a material risk due to potential political interference or lack of established legal precedent for international capital.

Other markets, including Japan, India, and Eastern Europe are also on the radar, but these present different challenges, such as tight cap rates in Japan or significant complexity in India.

(Credit: GRI Institute)

Value-Add & Opportunistic Deals - Where Are the Real Opportunities?

Defining Value-Add and Opportunistic Deals

The traditional definitions of value-add and opportunistic returns have shifted, primarily in response to the current high-cost and high-interest rate environment.

While opportunistic strategies historically targeted in excess of 20% internal rates of return (IRRs), developers are now taking on full development risk for much lower mid-teens or even 11% to 12% IRRs in the UK, focusing instead on fundamental metrics like a satisfactory long-term development yield.

The focus has moved from broad macro bets to more granular, bottom-up approaches centered on the fundamentals of the real estate, such as quality of location and confidence in future leasing.

While opportunistic strategies historically targeted in excess of 20% internal rates of return (IRRs), developers are now taking on full development risk for much lower mid-teens or even 11% to 12% IRRs in the UK, focusing instead on fundamental metrics like a satisfactory long-term development yield.

The focus has moved from broad macro bets to more granular, bottom-up approaches centered on the fundamentals of the real estate, such as quality of location and confidence in future leasing.

Focus on Fundamentals and Sponsor Quality

In today's environment, there is a strong emphasis on real estate fundamentals and the quality of the sponsor as a way to de-risk investments. Lenders are highly selective and are increasingly focused on the borrower's capitalisation and business plan quality, especially when considering stress cases.

A deal is most likely to secure funding if it has at least two of the three key components: a strong location, a reliable sponsor, and an attractive asset class.

A deal is most likely to secure funding if it has at least two of the three key components: a strong location, a reliable sponsor, and an attractive asset class.

Market Bifurcation and Geographic Selectivity

The market is experiencing significant bifurcation between the UK and continental Europe, primarily due to the impact of base rates on leverage. The UK struggles to achieve positive leverage, whereas many continental European markets currently offer slightly higher levels.

Lenders are highly selective within asset classes rather than excluding entire sectors, with current geographical focus areas for lending including France, Spain, Portugal, and Eastern Europe, but with different product focuses in each.

Lenders are highly selective within asset classes rather than excluding entire sectors, with current geographical focus areas for lending including France, Spain, Portugal, and Eastern Europe, but with different product focuses in each.

London Office Market: Demand vs. Cost

The central London office market presents a dichotomy of strong occupational demand and extremely high, "nonsensical" construction costs.

While prime sub-markets like the City and Mayfair have seen staggering rent growth, driven by low historical delivery projections and a strong occupational demand, the costs for development or redevelopment make achieving desired returns very difficult.

Furthermore, the UK's peculiar rent review structures can impair an office landlord's ability to capture rental growth compared to the simpler CPI-based cash flows often seen in continental Europe.

While prime sub-markets like the City and Mayfair have seen staggering rent growth, driven by low historical delivery projections and a strong occupational demand, the costs for development or redevelopment make achieving desired returns very difficult.

Furthermore, the UK's peculiar rent review structures can impair an office landlord's ability to capture rental growth compared to the simpler CPI-based cash flows often seen in continental Europe.

(Credit: GRI Institute)

The Refinancing Crunch - Deal or Default?

Ample Lending Liquidity is Mitigating Default Risk

The prevailing sentiment concurs that the wall of refinancing does not pose a systematic risk of default due to the high amount of liquidity available in the market.

This liquidity is coming not only from traditional banks - which are currently super-liquid, capital-efficient, and driven by relationship lending - but also from a significant number of alternative lenders, the bond market, and the return of the CMBS market.

This diversification and depth of the lending pool makes the refinancing issue relatively manageable, even for deals from the 2021-2022 vintages that face repricing.

This liquidity is coming not only from traditional banks - which are currently super-liquid, capital-efficient, and driven by relationship lending - but also from a significant number of alternative lenders, the bond market, and the return of the CMBS market.

This diversification and depth of the lending pool makes the refinancing issue relatively manageable, even for deals from the 2021-2022 vintages that face repricing.

Shift in Leverage and Asset Valuation

There has been a notable shift in lending metrics, with LTV ratios increasing to the point where "80% is the new 70%". This higher leverage is primarily being applied to refinancing existing loans to support the assets and sponsors, rather than financing new acquisitions.

The regulator's past policy of maintaining low LTV ratios on senior debt has served to protect the equity held by sponsors. A potential issue is that a number of current refinancing transactions involve the sponsor extracting capital, or are structured in a way that suggests they are halfway to selling the asset.

These particular deals are concerning as the high LTV ratios - sometimes reaching 90% - mean the underlying asset value is difficult to determine, leading to uncertainty over the true level of risk.

The regulator's past policy of maintaining low LTV ratios on senior debt has served to protect the equity held by sponsors. A potential issue is that a number of current refinancing transactions involve the sponsor extracting capital, or are structured in a way that suggests they are halfway to selling the asset.

These particular deals are concerning as the high LTV ratios - sometimes reaching 90% - mean the underlying asset value is difficult to determine, leading to uncertainty over the true level of risk.

Bifurcation and Concern for Office Assets

The office sector is experiencing a significant bifurcation. Prime offices are performing well and attracting liquidity, with credit markets returning for good assets. However, secondary offices, including those that are non-ESG compliant or in less desirable locations, are expected to struggle.

The lack of capital for necessary reforms or improvements means lenders could be "stuck" with assets that may become worthless. Furthermore, the higher cost to carry a deal post-GFC means equity must often fund interest costs if the asset isn't producing enough, compounding the difficulty for these secondary assets.

The lack of capital for necessary reforms or improvements means lenders could be "stuck" with assets that may become worthless. Furthermore, the higher cost to carry a deal post-GFC means equity must often fund interest costs if the asset isn't producing enough, compounding the difficulty for these secondary assets.

The Equity Cycle is the True Market Trigger

The general belief is that the real constraint and eventual trigger for asset sales and new acquisition financing will not be the debt market, but the equity cycle. This is linked to fund vintages, LPAC (Limited Partner Advisory Committee) decisions on extensions, and the need for funds to return money to LPs (Limited Partners) to raise new funds. This is expected to eventually force asset sales at potentially lower values to new buyers.

Core equity is now seen as a long-term IRR play rather than a cash substitute, with a potential target of 10% on a moderately levered basis.

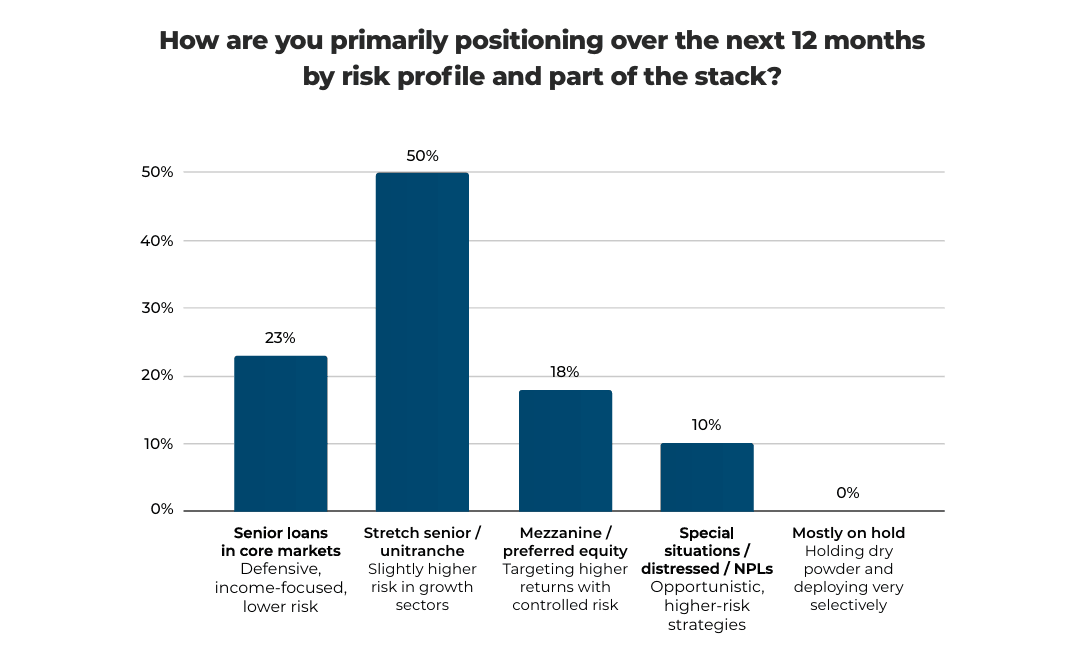

The survey provides a timely snapshot of prevailing sentiment and strategic intent across the European real estate credit and debt landscape. The results indicate a generally optimistic and active market, with participants demonstrating a clear preference for slightly higher-risk strategies focused on growth sectors, though stability in core markets remains a strong focus.

Key takeaways include a noticeable shift toward non-bank and hybrid lending models in real estate finance, the critical importance of strong sponsor track records and the cost of capital in mid-market transactions, and a concentration of the most attractive investment opportunities in Southern Europe and the UK.

The survey results reflect a predominantly optimistic outlook among investors, asset owners, and real estate developers in Europe, with a clear preference for positioning in slightly higher-risk strategies targeting growth sectors.

The majority of participants are leaning towards opportunities that offer potential for higher returns, even if they involve some risk. This suggests confidence in certain growth areas, despite broader economic uncertainties.

At the same time, there is a strong focus on more defensive, income-generating strategies, particularly in core markets, indicating that a significant portion of the market still values stability and predictable returns.

However, the low interest in distressed assets and the complete lack of preference for a "hold" strategy suggests that participants are generally active and searching for opportunities, rather than holding capital in reserve.

Overall, the results demonstrate a balanced yet slightly risk-tolerant approach, with a clear focus on growth and stability in equal measure.

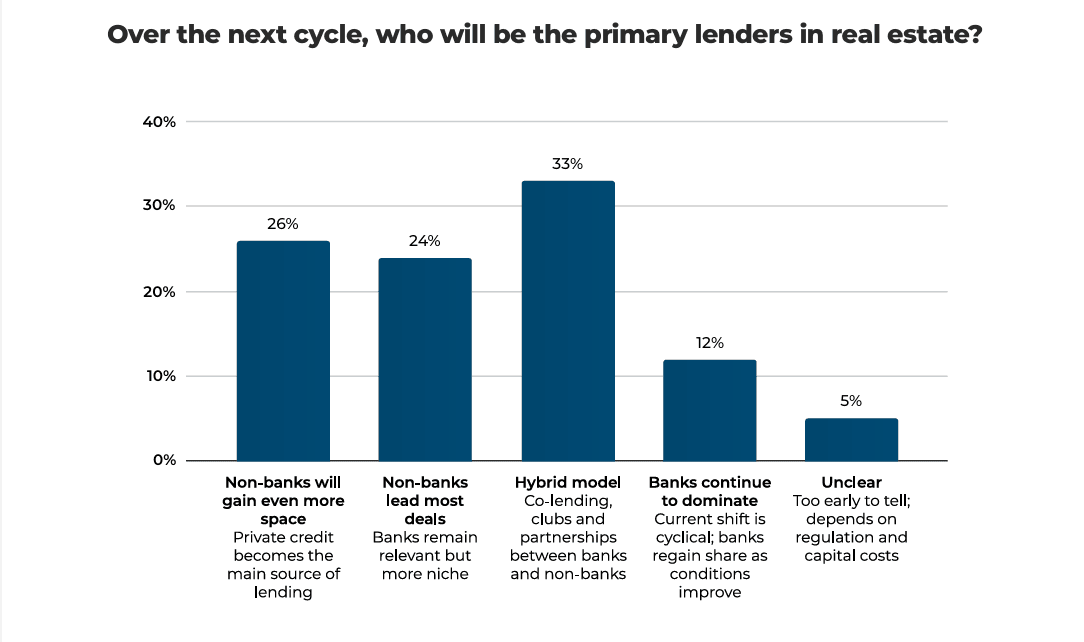

The survey results indicate a clear shift in the real estate lending landscape, with a notable presence of non-banks taking a leading role. A big part of respondents anticipate that private credit will become the primary source of lending or will gain even more space, reflecting growing confidence in non-bank lending as an alternative to traditional banks.

Many participants believe there will also be significant growth of the hybrid model, where co-lending and partnerships between banks and non-banks become more common. This suggests a collaborative approach that leverages the strengths of both sectors.

A smaller group of participants still sees banks as maintaining their dominance, though in a more niche capacity, pointing to a cyclical nature of the banking sector. It signs a shift away from traditional banking models in favour of more flexible, private credit-driven solutions.

Overall, the results suggest that non-banks and hybrid models will increasingly dominate the lending landscape in real estate, reflecting a broader trend towards diversification in capital sources.

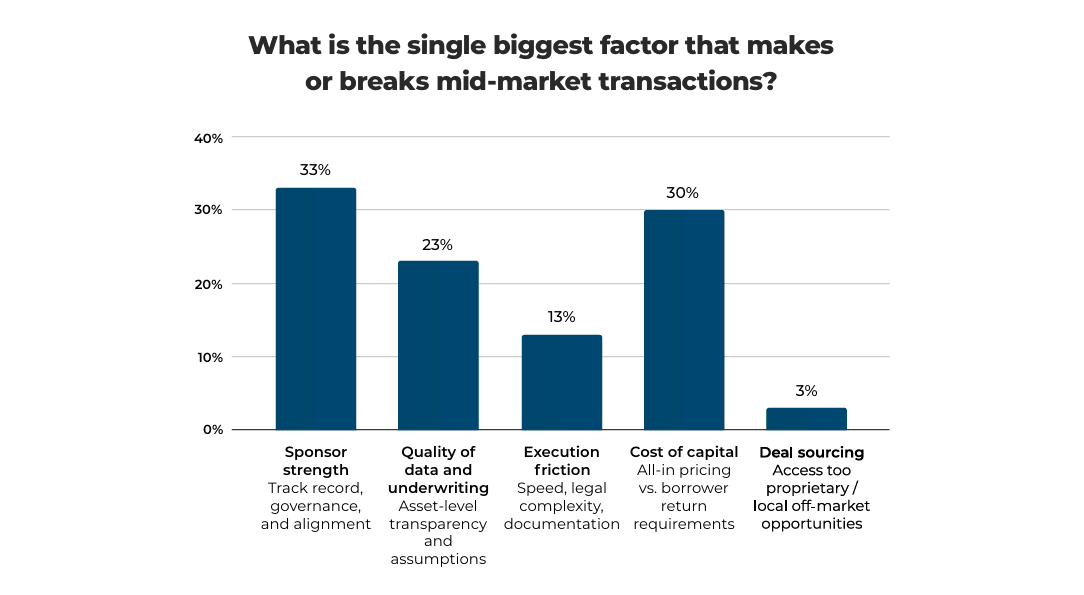

The survey results highlight that sponsor strength is considered the most critical factor in making or breaking mid-market transactions, with 33% of votes. This reflects the importance of a sponsor's track record, governance, and alignment, signalling that investors place significant value on the reputation and reliability of those leading the transaction.

Cost of capital follows closely with 30% of the votes, indicating that the pricing dynamics and how capital costs align with borrower return requirements are crucial in determining the success of mid-market deals.

Quality of data and underwriting also play an important role, with 23% emphasising the need for asset-level transparency and strong assumptions in the due diligence process.

On the other hand, factors such as execution friction (legal complexity, speed, and fees) and deal sourcing (access to proprietary or off-market opportunities) appear to be less significant, with 13% and 3% of the votes, respectively.

Overall, the results point to a market that highly values strong sponsorship, favourable capital structures, and well-supported underwriting processes in ensuring successful transactions.

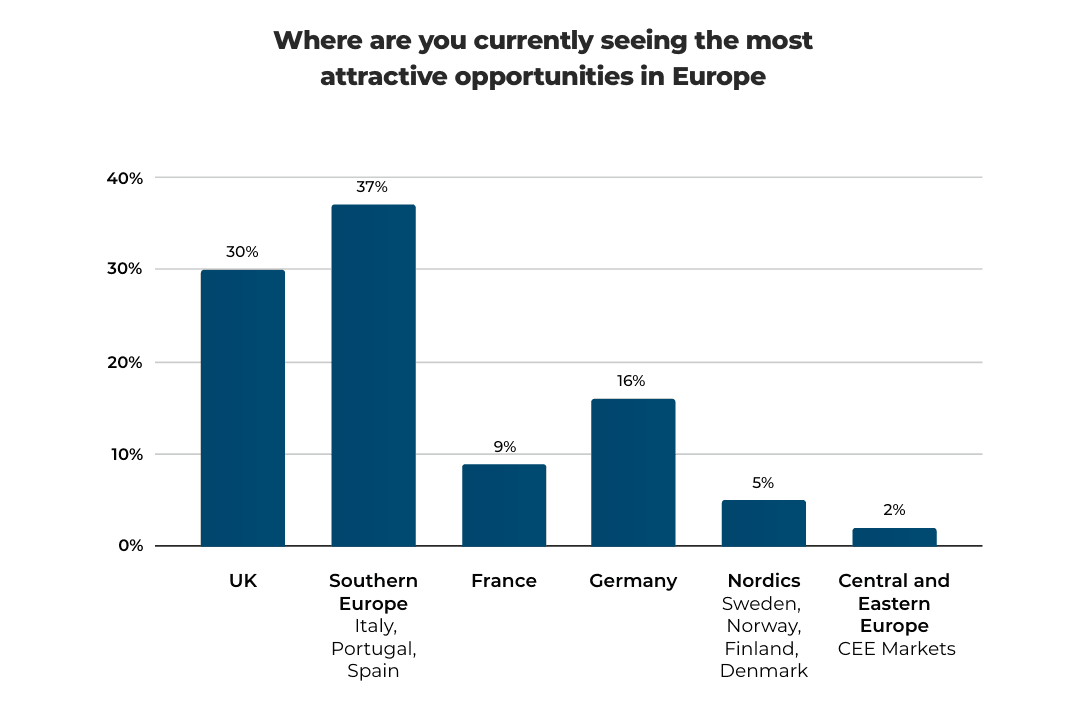

The results clearly show that the most attractive opportunities in Europe are concentrated in Southern Europe and the UK, with significant interest in these regions. Investors seem to be gravitating towards markets that offer potential for growth and favourable conditions, particularly in regions with a strong recovery trajectory and increasing market stability.

In contrast, countries in Northern Europe and Central & Eastern Europe (CEE) appear less appealing at this time, with minimal votes, indicating a weaker financing outlook.

This suggests that, while these regions have their merits, they are currently overshadowed by the more dynamic markets of Southern Europe and the UK, which are perceived as offering more immediate opportunities.

The overall sentiment points to a preference for markets with solid fundamentals and potential for continued growth, rather than regions with less financing opportunities.

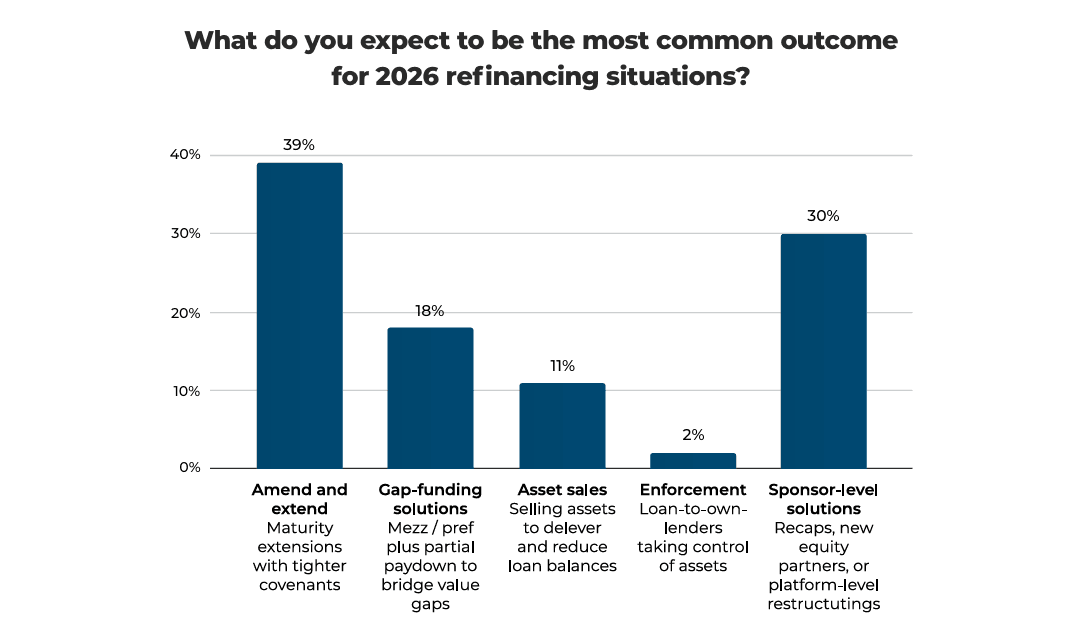

The results indicate a clear outcome for more flexible and negotiated refinancing solutions in 2026. The market is primarily anticipating maturity extensions, with tighter covenants, as a common strategy and outcome to manage refinancing situations. This reflects a cautious approach, with stakeholders looking to secure more time and stability, likely in response to ongoing economic challenges and liquidity concerns.

There is also a significant expectation that sponsor-driven solutions, including recapitalisations and the introduction of new equity partners, will play a significant role in navigating refinancing needs. This highlights the importance of strategic restructuring at the ownership level to maintain asset value and operational stability.

While some participants foresee gap-funding solutions to address value shortfalls, asset sales and lender takeovers are seen as less likely outcomes, suggesting that the market prefers to avoid drastic measures, unless absolutely necessary.

Overall, the results reflect a preference for proactive, flexible strategies that focus on extending terms and bolstering financial structures, rather than relying on liquidation or more severe enforcement actions.

Thank you to our discussion moderators, co-chairs, and all participants for their contributions to the valuable discussions that unfolded at GRI Credit Opportunities & RE Debt 2025.

Core equity is now seen as a long-term IRR play rather than a cash substitute, with a potential target of 10% on a moderately levered basis.

(Credit: GRI Institute)

Survey Results & Analysis

This section presents the key findings and analysis from the survey conducted among some of Europe’s most prominent real estate market stakeholders during the GRI Credit Opportunities & Real Estate Debt 2025 conference.The survey provides a timely snapshot of prevailing sentiment and strategic intent across the European real estate credit and debt landscape. The results indicate a generally optimistic and active market, with participants demonstrating a clear preference for slightly higher-risk strategies focused on growth sectors, though stability in core markets remains a strong focus.

Key takeaways include a noticeable shift toward non-bank and hybrid lending models in real estate finance, the critical importance of strong sponsor track records and the cost of capital in mid-market transactions, and a concentration of the most attractive investment opportunities in Southern Europe and the UK.

The majority of participants are leaning towards opportunities that offer potential for higher returns, even if they involve some risk. This suggests confidence in certain growth areas, despite broader economic uncertainties.

At the same time, there is a strong focus on more defensive, income-generating strategies, particularly in core markets, indicating that a significant portion of the market still values stability and predictable returns.

However, the low interest in distressed assets and the complete lack of preference for a "hold" strategy suggests that participants are generally active and searching for opportunities, rather than holding capital in reserve.

Overall, the results demonstrate a balanced yet slightly risk-tolerant approach, with a clear focus on growth and stability in equal measure.

The survey results indicate a clear shift in the real estate lending landscape, with a notable presence of non-banks taking a leading role. A big part of respondents anticipate that private credit will become the primary source of lending or will gain even more space, reflecting growing confidence in non-bank lending as an alternative to traditional banks.

Many participants believe there will also be significant growth of the hybrid model, where co-lending and partnerships between banks and non-banks become more common. This suggests a collaborative approach that leverages the strengths of both sectors.

A smaller group of participants still sees banks as maintaining their dominance, though in a more niche capacity, pointing to a cyclical nature of the banking sector. It signs a shift away from traditional banking models in favour of more flexible, private credit-driven solutions.

Overall, the results suggest that non-banks and hybrid models will increasingly dominate the lending landscape in real estate, reflecting a broader trend towards diversification in capital sources.

Cost of capital follows closely with 30% of the votes, indicating that the pricing dynamics and how capital costs align with borrower return requirements are crucial in determining the success of mid-market deals.

Quality of data and underwriting also play an important role, with 23% emphasising the need for asset-level transparency and strong assumptions in the due diligence process.

On the other hand, factors such as execution friction (legal complexity, speed, and fees) and deal sourcing (access to proprietary or off-market opportunities) appear to be less significant, with 13% and 3% of the votes, respectively.

Overall, the results point to a market that highly values strong sponsorship, favourable capital structures, and well-supported underwriting processes in ensuring successful transactions.

In contrast, countries in Northern Europe and Central & Eastern Europe (CEE) appear less appealing at this time, with minimal votes, indicating a weaker financing outlook.

This suggests that, while these regions have their merits, they are currently overshadowed by the more dynamic markets of Southern Europe and the UK, which are perceived as offering more immediate opportunities.

The overall sentiment points to a preference for markets with solid fundamentals and potential for continued growth, rather than regions with less financing opportunities.

There is also a significant expectation that sponsor-driven solutions, including recapitalisations and the introduction of new equity partners, will play a significant role in navigating refinancing needs. This highlights the importance of strategic restructuring at the ownership level to maintain asset value and operational stability.

While some participants foresee gap-funding solutions to address value shortfalls, asset sales and lender takeovers are seen as less likely outcomes, suggesting that the market prefers to avoid drastic measures, unless absolutely necessary.

Overall, the results reflect a preference for proactive, flexible strategies that focus on extending terms and bolstering financial structures, rather than relying on liquidation or more severe enforcement actions.

Thank you to our discussion moderators, co-chairs, and all participants for their contributions to the valuable discussions that unfolded at GRI Credit Opportunities & RE Debt 2025.