Credit: GRI Institute

Credit: GRI InstituteGRI Market Intelligence: How senior real estate leaders are pricing 2026 risks

Global decision-makers signal recovery in 2026 as AI optimism battles recession fears and geopolitical volatility

January 28, 2026Real Estate

Written by:Helen Richards

Key Takeaways

- While a 61% majority of leaders are optimistic about a market recovery, a deep recession remains the top concern keeping 40% up at night.

- Most leaders view AI as a massive productivity tailwind, yet there is significant underlying anxiety regarding its potential to disrupt the traditional employment base.

- Overregulation is identified as the primary reason Europe is losing its competitive edge against other global markets.

As the global real estate market enters 2026, the industry appears to be shedding the paralysis of recent years in favour of cautious, pragmatic optimism. According to GRI Institute's comprehensive poll of the world’s most senior real estate leaders, 61% of respondents now hold a positive outlook for the next 12 months, signalling a widespread belief that the valuation correction cycle has finally hit its floor.

However, this recovery is far from uniform; with 56% viewing artificial intelligence as a transformative tailwind for productivity, and a significant 40% being kept awake at night by the spectre of a deep recession hitting Western economies.

From the "Trump factor" complicating global risk pricing to a sharp bifurcation in office yields, the results herein reveal an industry that is simultaneously emboldened by new capital opportunities and hyper-vigilant of a fragile geopolitical and economic scaffolding.

A clear majority of leaders maintain a positive outlook, with 61% identifying as either optimistic or highly optimistic. This sentiment suggests that the market has largely digested the interest rate shocks of previous years and is looking toward a period of stabilisation. The prevailing optimism also stems from the belief that the valuation correction cycle is nearing its floor, providing more predictable entry points for new capital.

However, the 28% neutral stance indicates that a significant portion of decision makers remains in a "wait and see" mode, perhaps wary of residual volatility in capital markets.

While a small 8% remains pessimistic, the overall weight of opinion suggests that the industry expects a steady, if not substantial, recovery in transaction volumes and liquidity through 2026.

The sentiment regarding Donald J. Trump’s impact on the West is heavily skewed toward concern, with 49% viewing his influence as unpredictable and destabilising. This reflects a broader institutional anxiety regarding trade tariffs, international alliances, and the potential for sudden shifts in American foreign policy that could ripple through global financial markets.

Conversely, 20% of respondents see him as an effective leader capable of restoring confidence after years of perceived drift. This minority view often aligns with the desire for deregulation and pro-growth fiscal policies.

With 31% still viewing the situation as a high-risk gamble, it is evident that the "Trump factor" remains one of the most significant variables in global risk pricing for real estate investors today.

The threat of a deep recession hitting the West is the primary concern, cited by 40% of Retreat participants, followed closely by the fear that AI might destroy jobs rather than create them. This highlights a dual anxiety: a traditional cyclical downturn paired with a structural fear that the next technological revolution could undermine the very employment base that supports office and residential sectors.

Inflation and debt remain persistent worries, with 27% fearing an inflationary return and 24% concerned about hidden debt "detonating" in the credit markets.

Interestingly, only 9% feel that "everything is going well," suggesting that while leaders are optimistic about their own industry's prospects, according to question 1, they remain hyper-vigilant about the fragile global economic scaffolding supporting it.

AI is overwhelmingly viewed as a great force for the industry, with 56% seeing it as a massive tailwind for productivity and growth. This optimism largely centres on the potential for AI to streamline property management, enhance data-driven investment decisions, and power the burgeoning data centre asset class.

Despite the hype, 33% are still in a "wait and see" mode, reflecting the uncertainty about how AI will fundamentally change the demand for physical office space. Only 11% view it as an "office killer," suggesting that while the industry expects disruption, most leaders believe the productivity gains will ultimately support the broader economic ecosystem and, by extension, property values.

Sentiment toward commercial real estate lending is notably positive, with 48% agreeing that risk-adjusted returns are currently attractive. As traditional banks have retrenched due to regulatory pressure, private credit and alternative lenders have found a lucrative gap, benefiting from higher margins and lower loan-to-value ratios that provide a significant safety cushion.

However, 45% remain cautious, noting that while the opportunity is there, traps remain in specific asset classes or geographies. This suggests that while the lending gap offers high rewards, it requires intense due diligence to avoid legacy issues, particularly in secondary office assets or over-leveraged portfolios.

The diagnosis for Europe’s perceived stagnation is blunt: 58% of leaders believe the continent is overregulated and hostile to risk-taking. This reflects a long-standing frustration with the pace of planning, the complexity of ESG compliance, and a general cultural hesitancy toward the kind of aggressive innovation seen in the US or Asia.

Intriguingly, 23% of respondents see a renaissance occurring, perhaps buoyed by Europe’s leadership in the green energy transition and the resilience of its urban cores. However, with 10% pointing to ageing populations and low productivity as the primary drag, it is clear that Europe faces a significant demographic and structural uphill battle to remain competitive on the global stage.

The logistics sector, formerly the "darling" of the pandemic era, is now viewed with measured caution. While 28% see a clear return of momentum, a 53% majority believe the recovery is still fragile and confined to specific pockets. This reflects a market that has moved past the initial e-commerce explosion and is now grappling with higher construction costs and a more discerning occupier base.

The fragility mentioned by the majority concerns issues such as the just-in-case (JIC) inventory levels being re-evaluated and the impact of softening consumer demand in certain European regions. Investors are no longer buying the sector wholesale but are instead focusing on ultra-prime last-mile locations where supply remains strictly constrained by planning and geography.

Residential real estate continues to be a high-conviction sector, with 55% of leaders confirming it should remain a global allocation priority due to winning structural demand.

The chronic undersupply of housing across major European and global cities provides a defensive quality that few other asset classes can match, particularly during periods of economic uncertainty.

That said, 36% of respondents are more selective, arguing that it only works in the right markets. This caution is often driven by the increasing prevalence of rent controls and tighter regulations in cities like Berlin, London, or Paris, which can cap the upside potential despite the undeniable demand for housing.

Opinion on the European data centre market is split almost three ways, indicating a high level of uncertainty. While 26% believe risks are now broadly priced in, another 26% argue that key risks - such as power availability, sovereign data regulations, and cooling requirements - remain mispriced.

The 29% who feel that optimism is currently ahead of reality reflects concerns over the AI bubble and the sheer difficulty of securing the power grid connections necessary to deliver these projects.

As data centres move from a niche infrastructure play to a mainstream real estate asset, the industry is clearly struggling to standardise how risk is assessed in this power-hungry sector.

Confidence in the hospitality sector is high, with 58% agreeing that hotel CapEx is driving real upside and value. Unlike the office sector, where CapEx is often defensive (required just to maintain occupancy), hotel investments in 2026 are frequently offensive, aimed at capturing the robust demand for experiential travel and luxury services.

Only 9% see CapEx as mostly defensive, which suggests that the hospitality sector is successfully pivoting its business models to meet post-pandemic consumer preferences. While selective value remains a theme for 30%, the overall sentiment is that the sector has the magic formula for passing on costs to consumers while enhancing asset value through active management.

The debate over office yields reveals a growing bifurcation, with 68% stating that current yields only reflect fundamentals in prime assets. This suggests that the Class A market is stabilising, but a significant portion of the secondary market is still masking structural weakness, a sentiment shared by 18% of the group.

This divide is the defining characteristic of the 2026 office market. While top-tier, ESG-compliant buildings in central business districts are finding a new price equilibrium, older assets are increasingly viewed as stranded, requiring massive capital expenditure to remain viable or being slated for conversion to other uses.

Thank you to our esteemed GRI members and real estate leaders who participated in this survey during the GRI Chairmen’s Retreat Europe 2026.

However, this recovery is far from uniform; with 56% viewing artificial intelligence as a transformative tailwind for productivity, and a significant 40% being kept awake at night by the spectre of a deep recession hitting Western economies.

From the "Trump factor" complicating global risk pricing to a sharp bifurcation in office yields, the results herein reveal an industry that is simultaneously emboldened by new capital opportunities and hyper-vigilant of a fragile geopolitical and economic scaffolding.

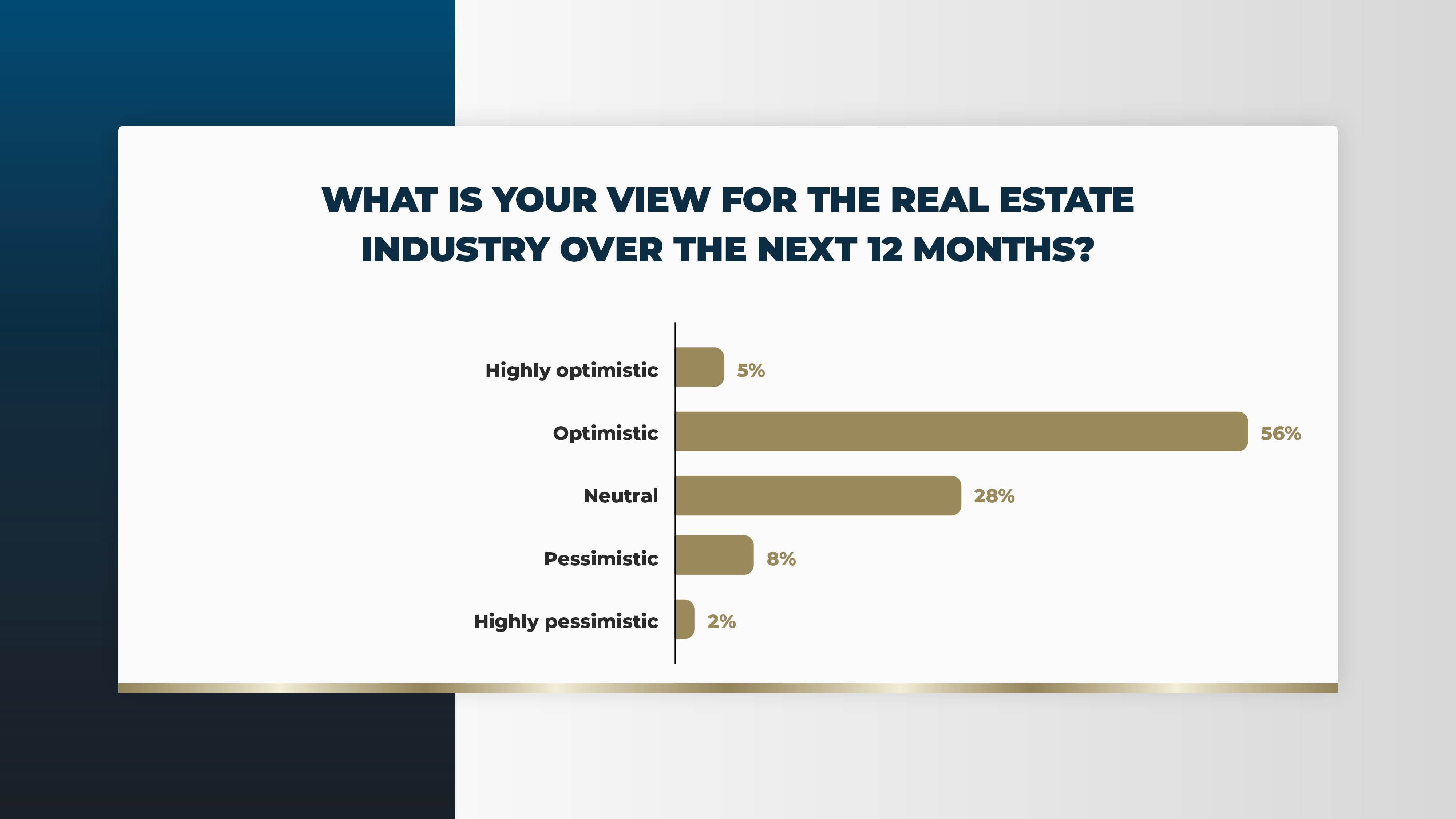

What is your view for the real estate industry over the next 12 months?

A clear majority of leaders maintain a positive outlook, with 61% identifying as either optimistic or highly optimistic. This sentiment suggests that the market has largely digested the interest rate shocks of previous years and is looking toward a period of stabilisation. The prevailing optimism also stems from the belief that the valuation correction cycle is nearing its floor, providing more predictable entry points for new capital.

However, the 28% neutral stance indicates that a significant portion of decision makers remains in a "wait and see" mode, perhaps wary of residual volatility in capital markets.

While a small 8% remains pessimistic, the overall weight of opinion suggests that the industry expects a steady, if not substantial, recovery in transaction volumes and liquidity through 2026.

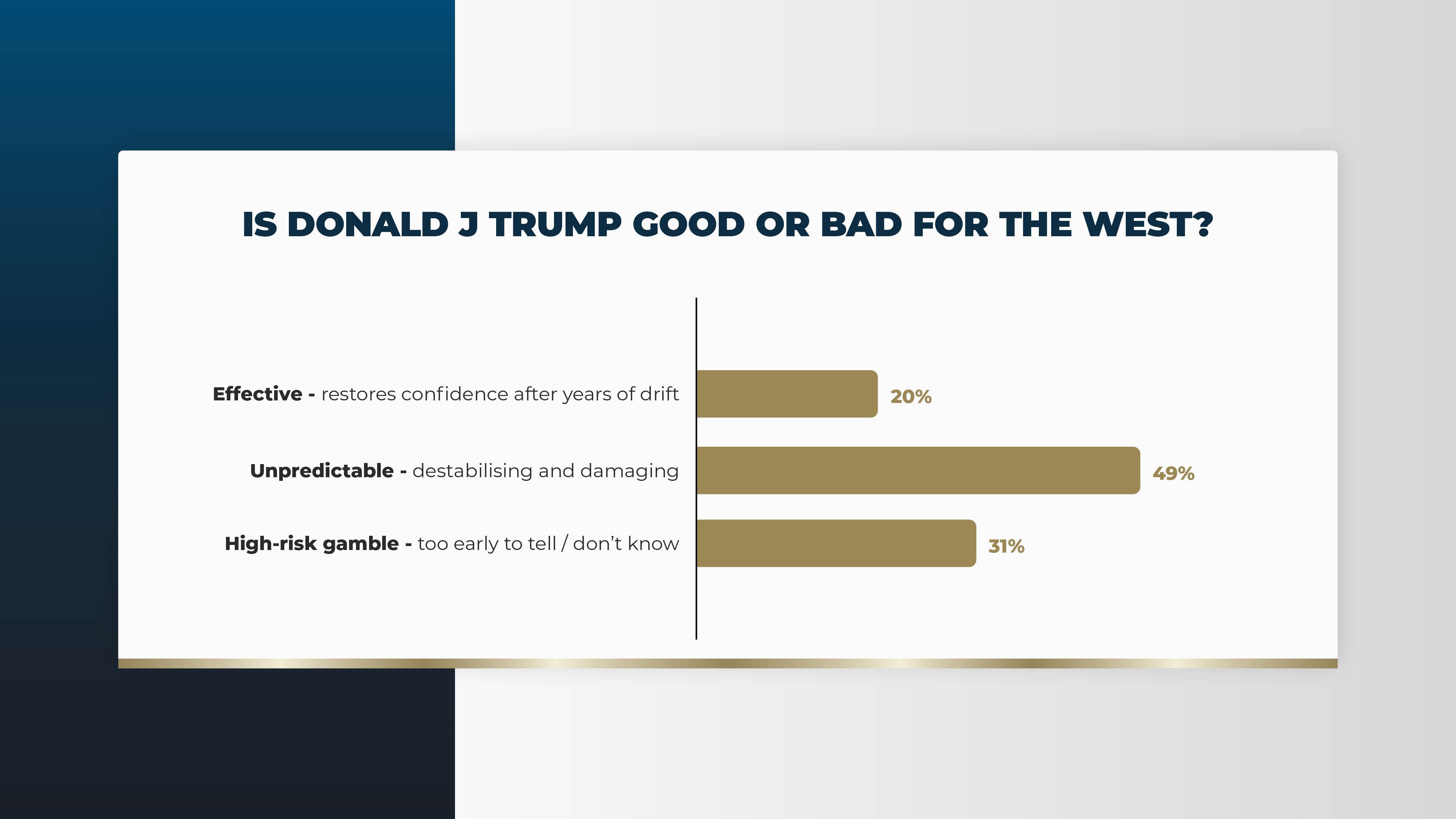

Is Donald J Trump good or bad for the West?

The sentiment regarding Donald J. Trump’s impact on the West is heavily skewed toward concern, with 49% viewing his influence as unpredictable and destabilising. This reflects a broader institutional anxiety regarding trade tariffs, international alliances, and the potential for sudden shifts in American foreign policy that could ripple through global financial markets.

Conversely, 20% of respondents see him as an effective leader capable of restoring confidence after years of perceived drift. This minority view often aligns with the desire for deregulation and pro-growth fiscal policies.

With 31% still viewing the situation as a high-risk gamble, it is evident that the "Trump factor" remains one of the most significant variables in global risk pricing for real estate investors today.

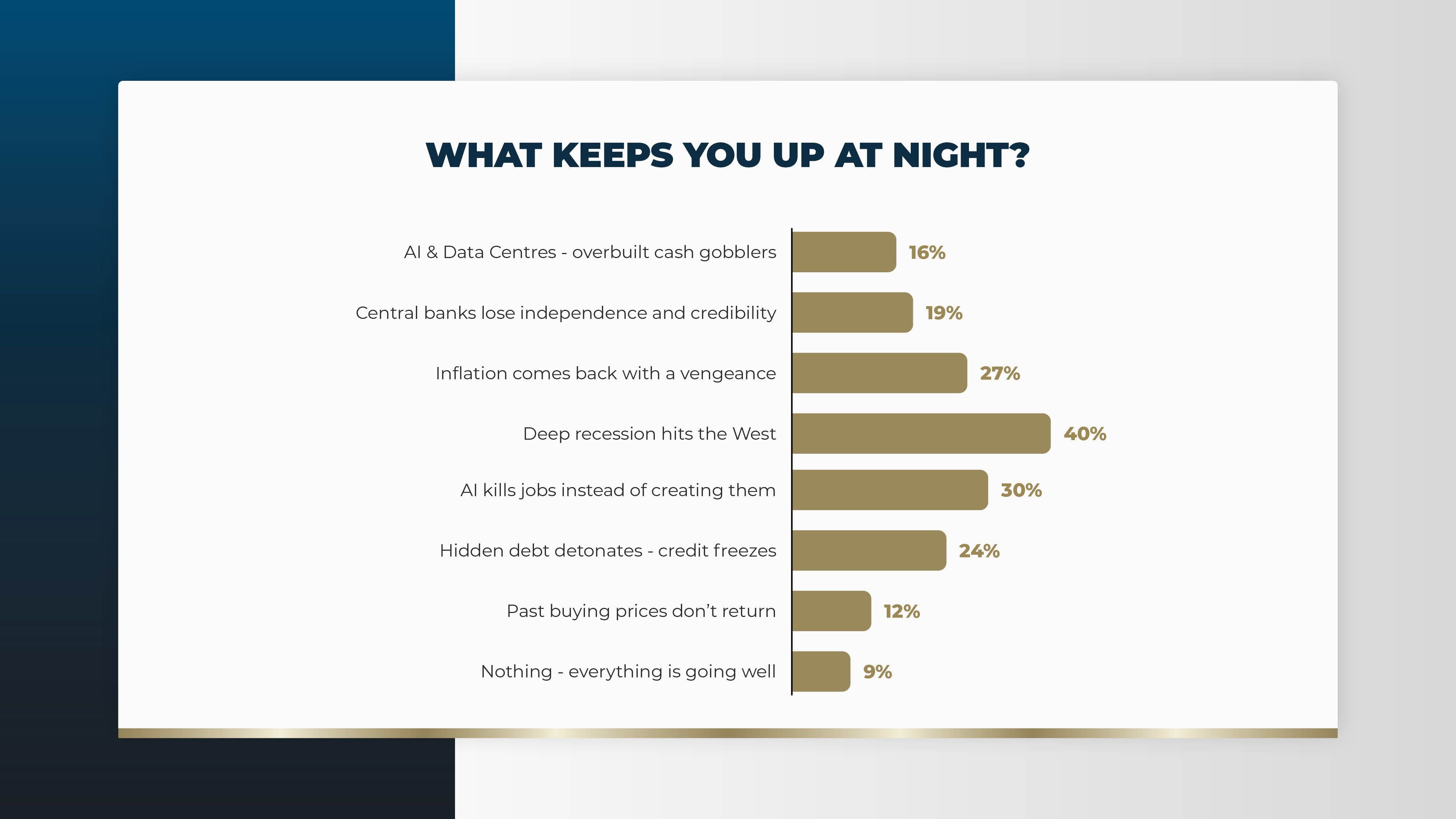

What keeps you up at night?

The threat of a deep recession hitting the West is the primary concern, cited by 40% of Retreat participants, followed closely by the fear that AI might destroy jobs rather than create them. This highlights a dual anxiety: a traditional cyclical downturn paired with a structural fear that the next technological revolution could undermine the very employment base that supports office and residential sectors.

Inflation and debt remain persistent worries, with 27% fearing an inflationary return and 24% concerned about hidden debt "detonating" in the credit markets.

Interestingly, only 9% feel that "everything is going well," suggesting that while leaders are optimistic about their own industry's prospects, according to question 1, they remain hyper-vigilant about the fragile global economic scaffolding supporting it.

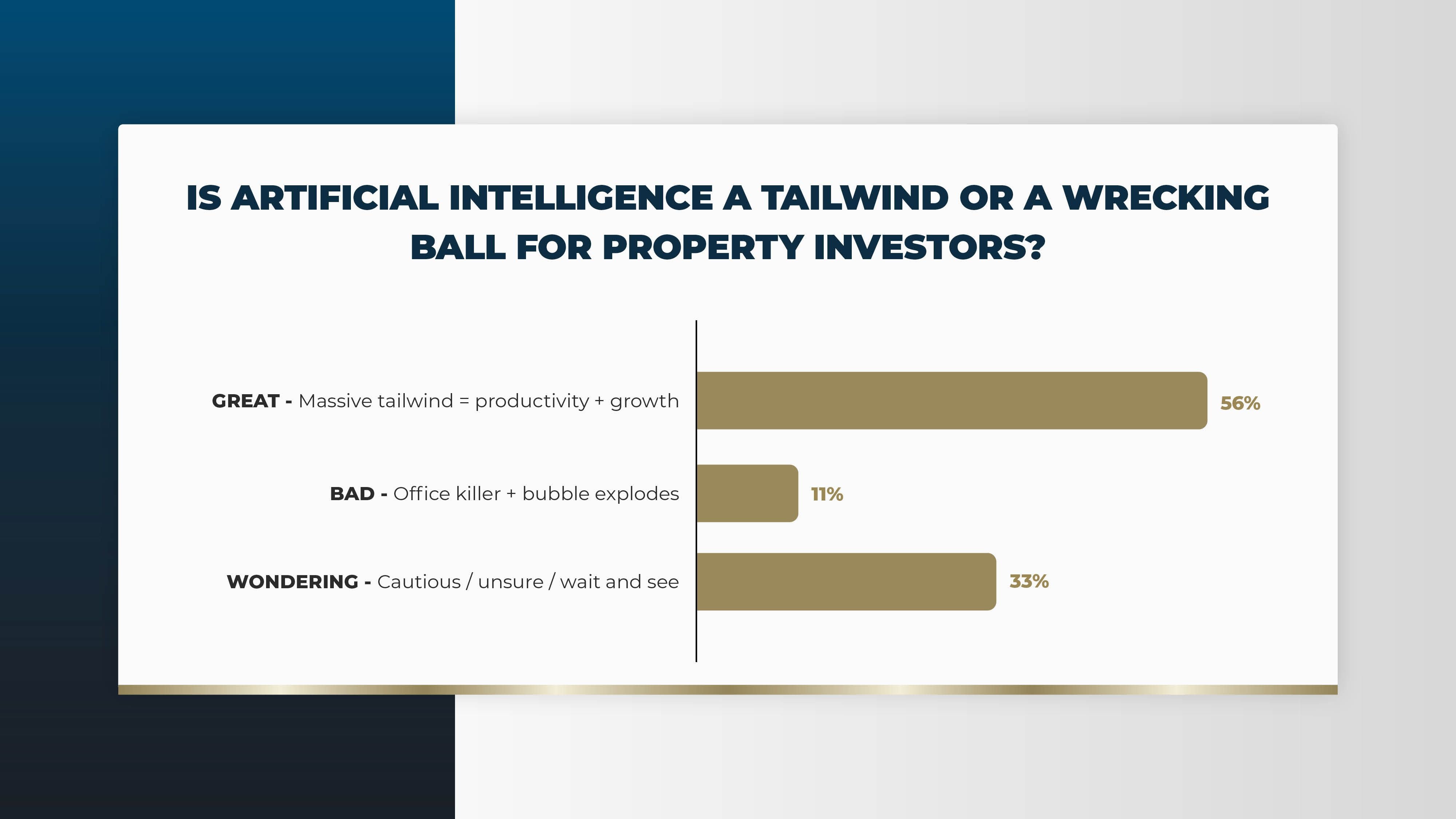

Is artificial intelligence a tailwind or a wrecking ball for property investors?

AI is overwhelmingly viewed as a great force for the industry, with 56% seeing it as a massive tailwind for productivity and growth. This optimism largely centres on the potential for AI to streamline property management, enhance data-driven investment decisions, and power the burgeoning data centre asset class.

Despite the hype, 33% are still in a "wait and see" mode, reflecting the uncertainty about how AI will fundamentally change the demand for physical office space. Only 11% view it as an "office killer," suggesting that while the industry expects disruption, most leaders believe the productivity gains will ultimately support the broader economic ecosystem and, by extension, property values.

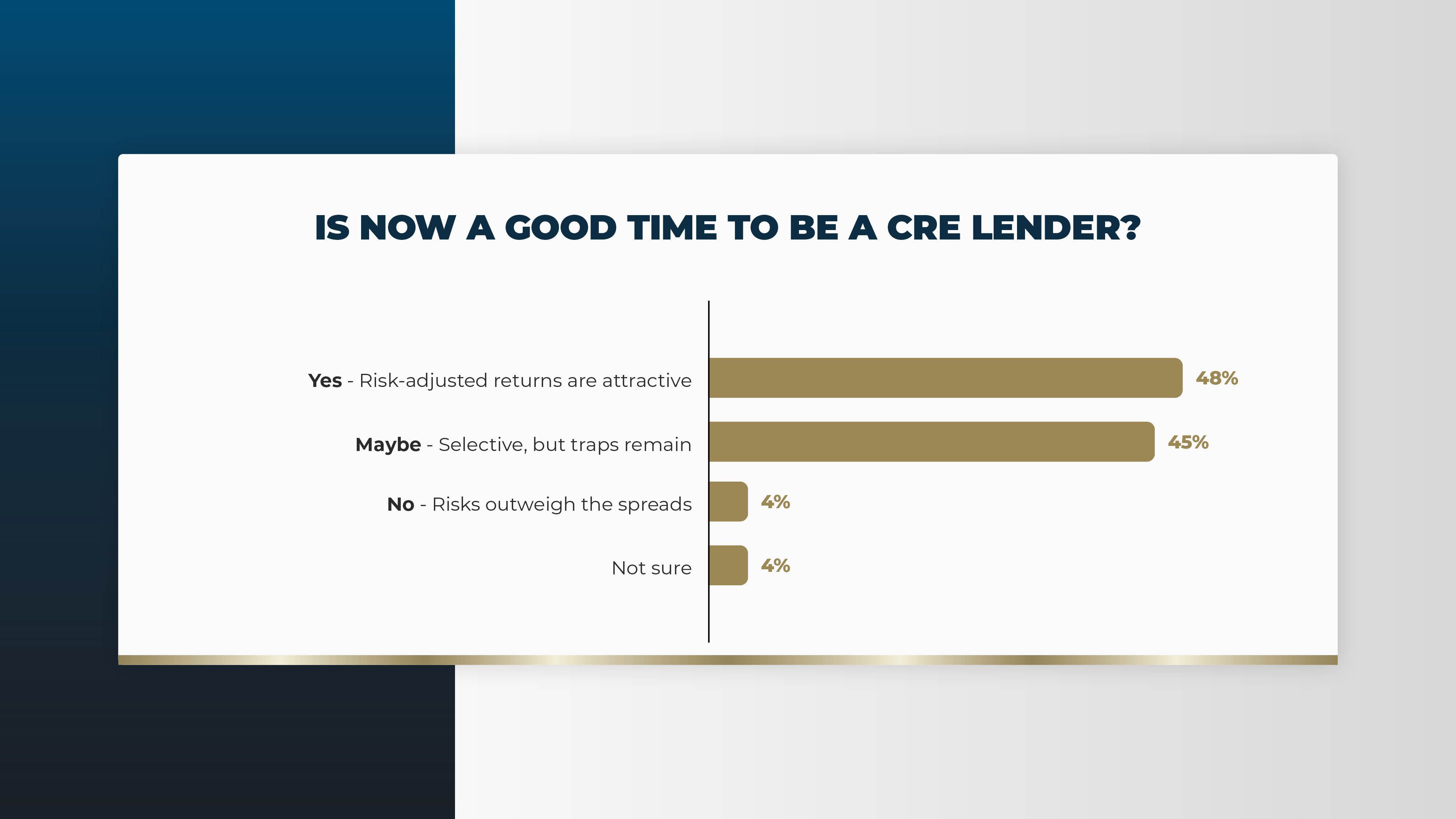

Is now a good time to be a CRE lender?

Sentiment toward commercial real estate lending is notably positive, with 48% agreeing that risk-adjusted returns are currently attractive. As traditional banks have retrenched due to regulatory pressure, private credit and alternative lenders have found a lucrative gap, benefiting from higher margins and lower loan-to-value ratios that provide a significant safety cushion.

However, 45% remain cautious, noting that while the opportunity is there, traps remain in specific asset classes or geographies. This suggests that while the lending gap offers high rewards, it requires intense due diligence to avoid legacy issues, particularly in secondary office assets or over-leveraged portfolios.

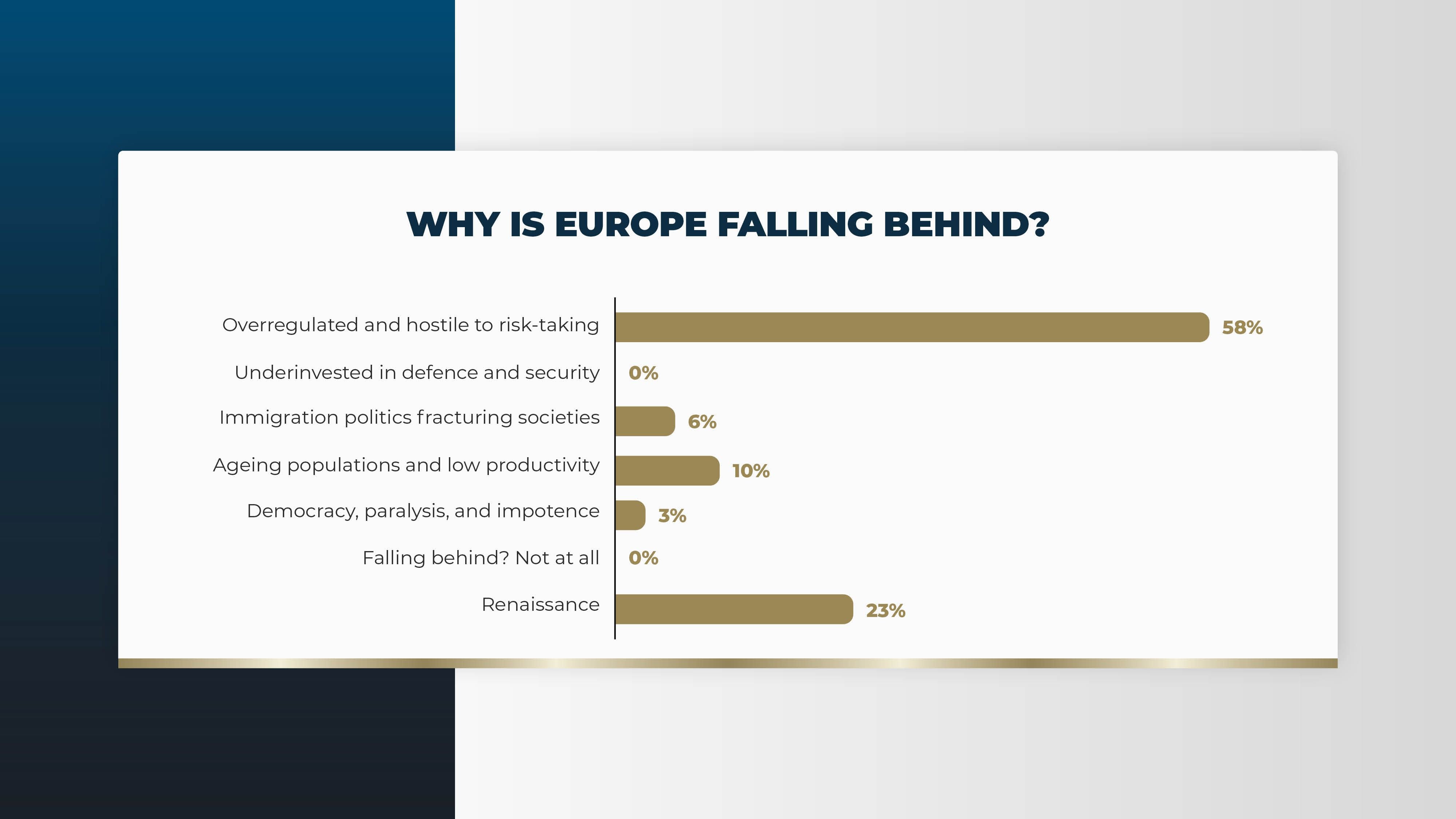

Why is Europe falling behind?

The diagnosis for Europe’s perceived stagnation is blunt: 58% of leaders believe the continent is overregulated and hostile to risk-taking. This reflects a long-standing frustration with the pace of planning, the complexity of ESG compliance, and a general cultural hesitancy toward the kind of aggressive innovation seen in the US or Asia.

Intriguingly, 23% of respondents see a renaissance occurring, perhaps buoyed by Europe’s leadership in the green energy transition and the resilience of its urban cores. However, with 10% pointing to ageing populations and low productivity as the primary drag, it is clear that Europe faces a significant demographic and structural uphill battle to remain competitive on the global stage.

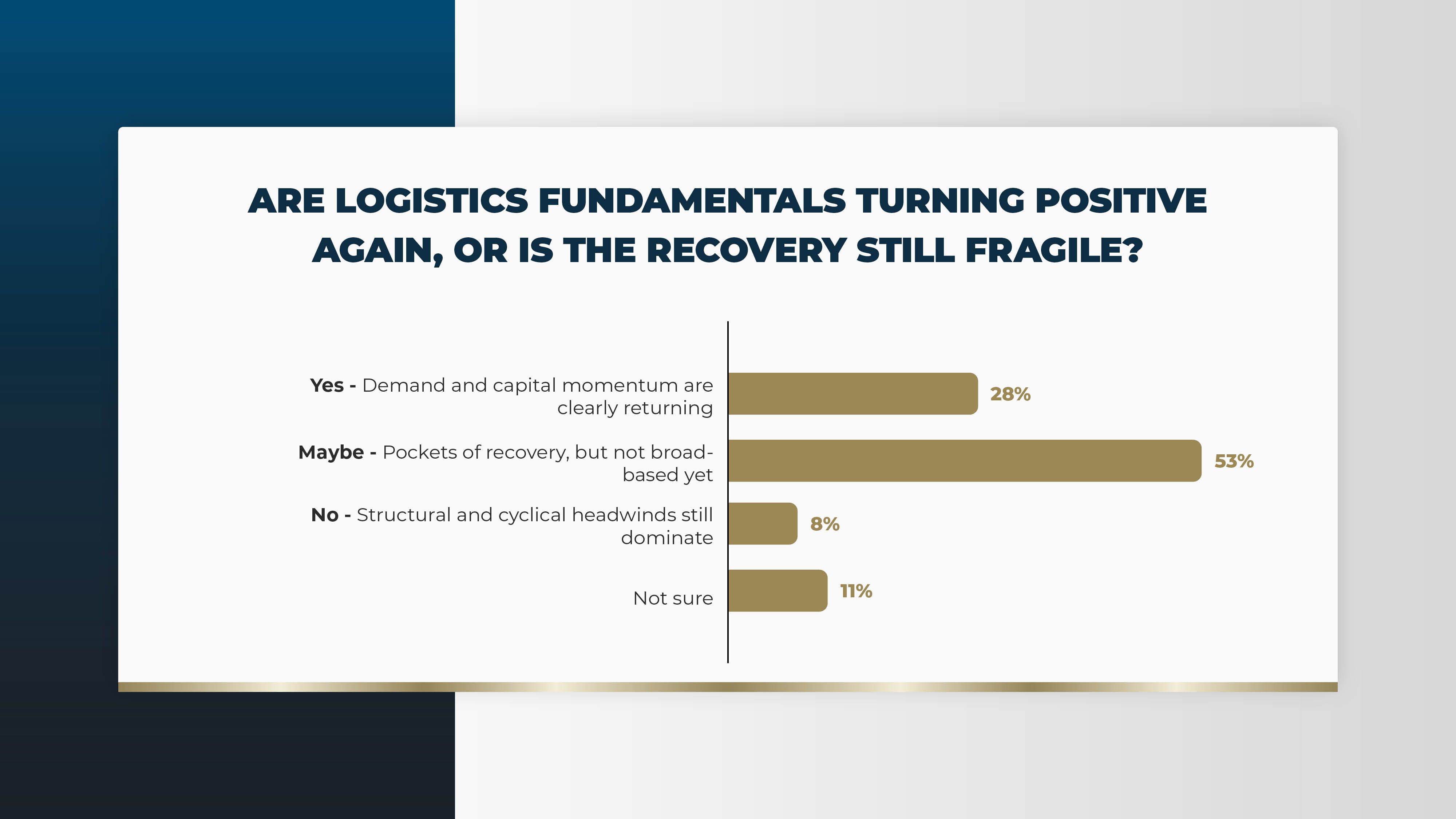

Are logistics fundamentals turning positive again, or is the recovery still fragile?

The logistics sector, formerly the "darling" of the pandemic era, is now viewed with measured caution. While 28% see a clear return of momentum, a 53% majority believe the recovery is still fragile and confined to specific pockets. This reflects a market that has moved past the initial e-commerce explosion and is now grappling with higher construction costs and a more discerning occupier base.

The fragility mentioned by the majority concerns issues such as the just-in-case (JIC) inventory levels being re-evaluated and the impact of softening consumer demand in certain European regions. Investors are no longer buying the sector wholesale but are instead focusing on ultra-prime last-mile locations where supply remains strictly constrained by planning and geography.

Should residential still be a global allocation priority?

Residential real estate continues to be a high-conviction sector, with 55% of leaders confirming it should remain a global allocation priority due to winning structural demand.

The chronic undersupply of housing across major European and global cities provides a defensive quality that few other asset classes can match, particularly during periods of economic uncertainty.

That said, 36% of respondents are more selective, arguing that it only works in the right markets. This caution is often driven by the increasing prevalence of rent controls and tighter regulations in cities like Berlin, London, or Paris, which can cap the upside potential despite the undeniable demand for housing.

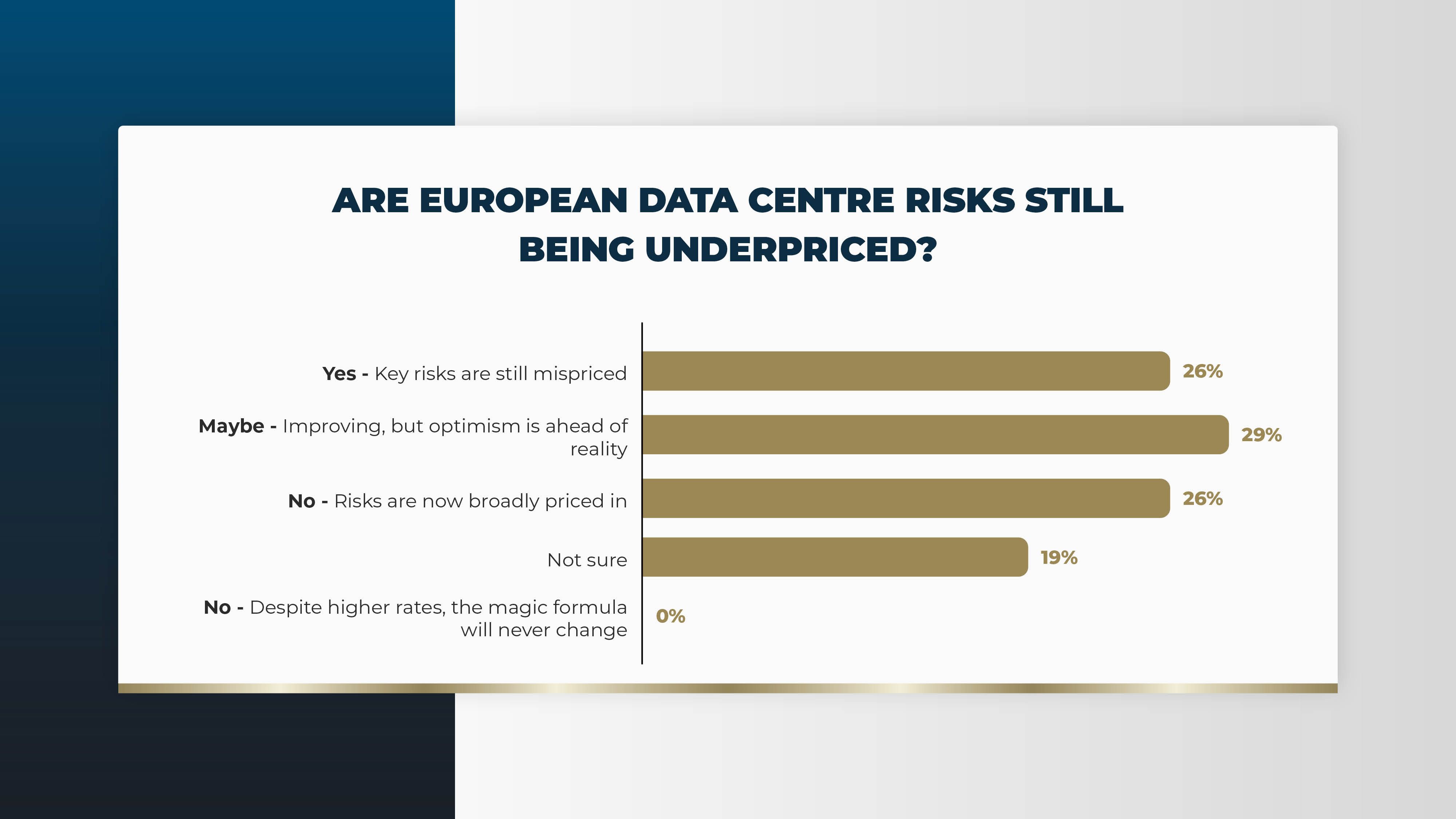

Are European data centre risks still being underpriced?

Opinion on the European data centre market is split almost three ways, indicating a high level of uncertainty. While 26% believe risks are now broadly priced in, another 26% argue that key risks - such as power availability, sovereign data regulations, and cooling requirements - remain mispriced.

The 29% who feel that optimism is currently ahead of reality reflects concerns over the AI bubble and the sheer difficulty of securing the power grid connections necessary to deliver these projects.

As data centres move from a niche infrastructure play to a mainstream real estate asset, the industry is clearly struggling to standardise how risk is assessed in this power-hungry sector.

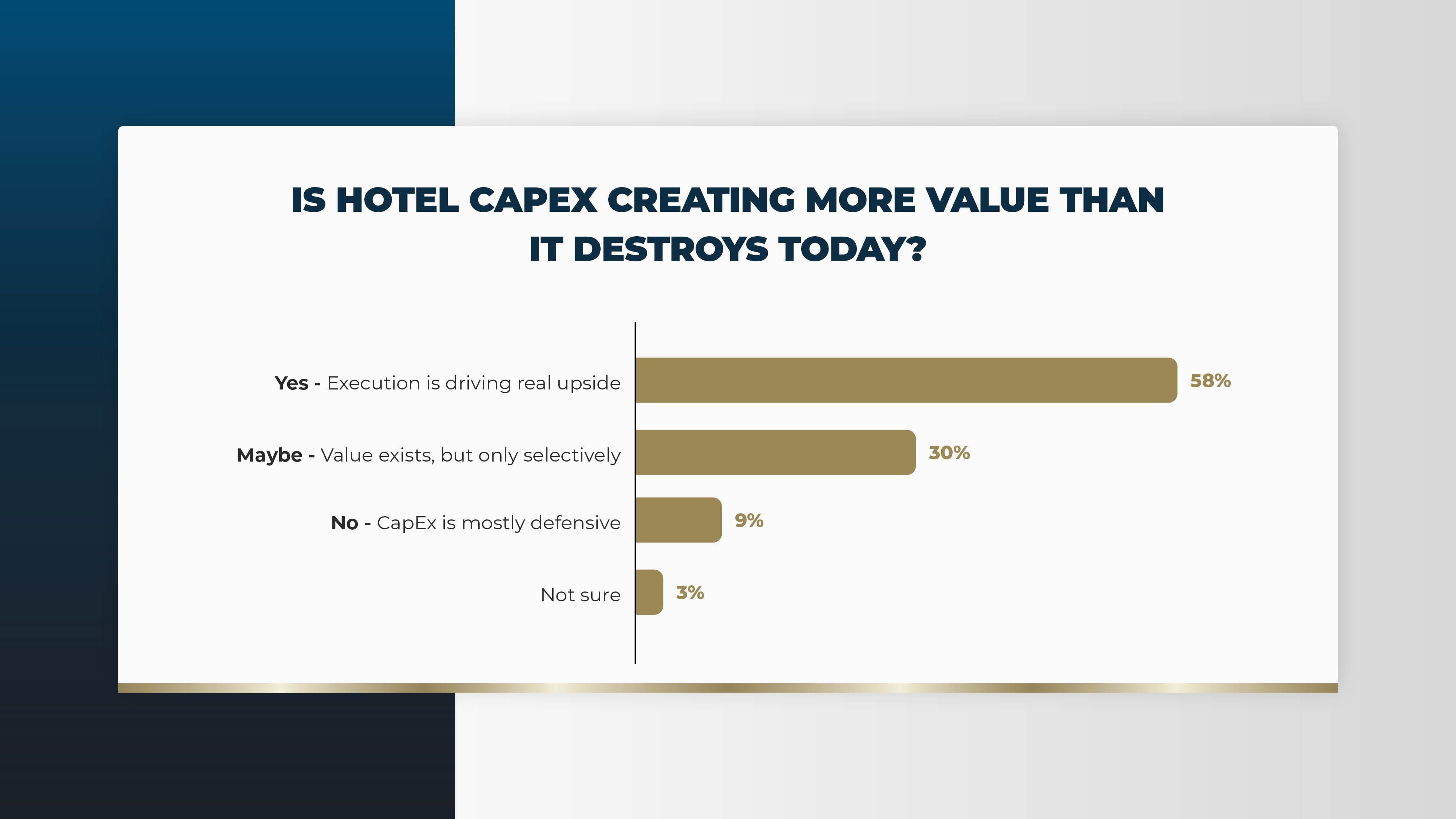

Is hotel CapEx creating more value than it destroys today?

Confidence in the hospitality sector is high, with 58% agreeing that hotel CapEx is driving real upside and value. Unlike the office sector, where CapEx is often defensive (required just to maintain occupancy), hotel investments in 2026 are frequently offensive, aimed at capturing the robust demand for experiential travel and luxury services.

Only 9% see CapEx as mostly defensive, which suggests that the hospitality sector is successfully pivoting its business models to meet post-pandemic consumer preferences. While selective value remains a theme for 30%, the overall sentiment is that the sector has the magic formula for passing on costs to consumers while enhancing asset value through active management.

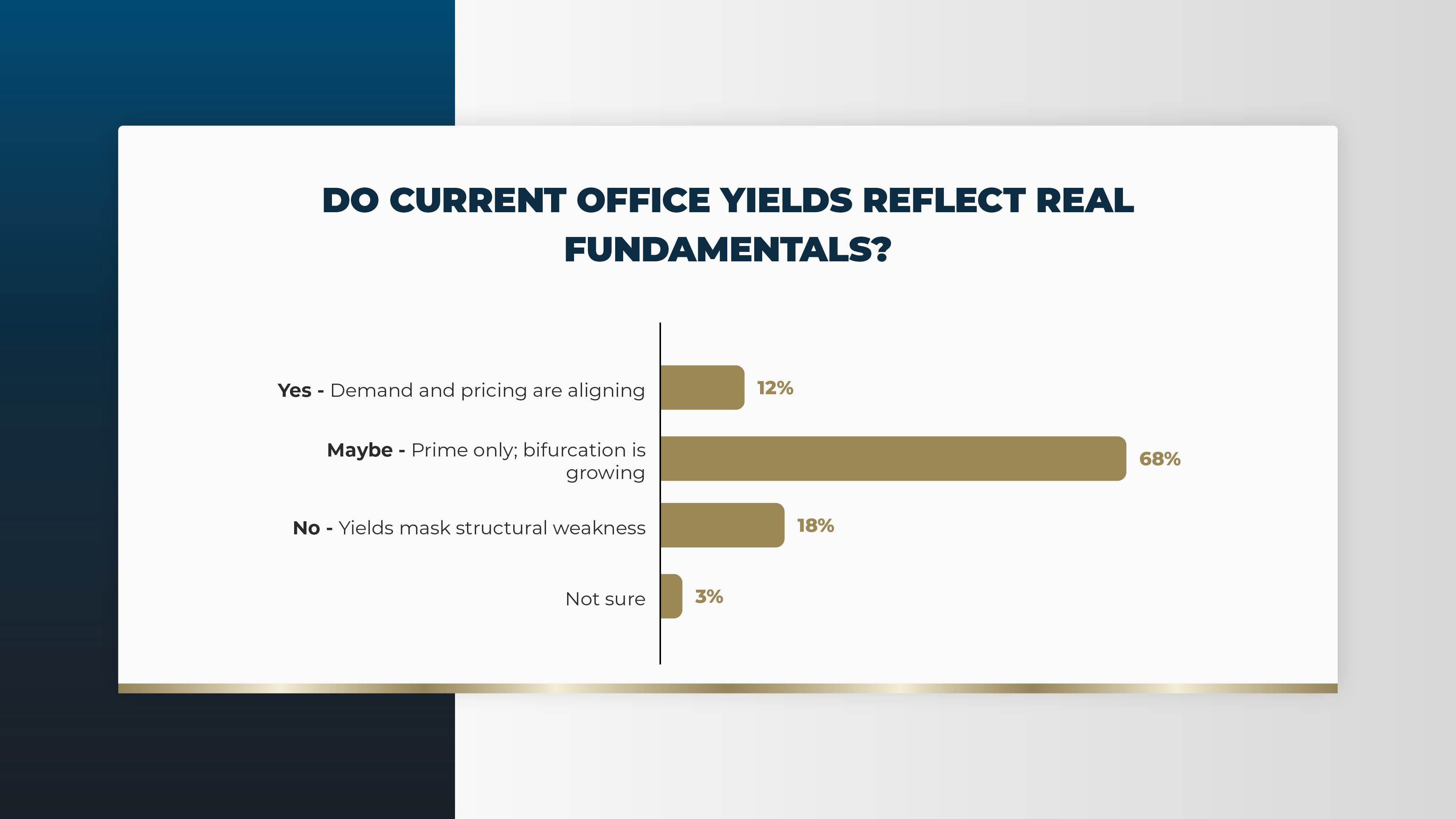

Do current office yields reflect real fundamentals?

The debate over office yields reveals a growing bifurcation, with 68% stating that current yields only reflect fundamentals in prime assets. This suggests that the Class A market is stabilising, but a significant portion of the secondary market is still masking structural weakness, a sentiment shared by 18% of the group.

This divide is the defining characteristic of the 2026 office market. While top-tier, ESG-compliant buildings in central business districts are finding a new price equilibrium, older assets are increasingly viewed as stranded, requiring massive capital expenditure to remain viable or being slated for conversion to other uses.

Thank you to our esteemed GRI members and real estate leaders who participated in this survey during the GRI Chairmen’s Retreat Europe 2026.