Credit: GRI Institute

Credit: GRI InstituteEuropean Hospitality's Value Revolution: Why investors are betting on repositioning and operational gains

Insights from GRI Hospitality Europe reveal that value-add reigns, luxury leads RevPAR, and labour costs pressure GOP

December 16, 2025Real Estate

Written by:Helen Richards

Executive Summary

This report presents critical market insights and expert consensus derived directly from the discussions and a dedicated survey conducted at the GRI Hospitality Europe 2025 conference in Rome. The findings reflect the near-to-medium-term outlook, focusing on capital allocation, performance expectations, key risks, and the changing financial structure of the hospitality sector. A clear theme is the rise of value-add strategies, as investors move away from purely core acquisitions to focus on creating value through operational enhancements and strategic capital investment. This shift is closely linked to the necessity of mastering operational levers beyond simple real estate transactions.

Key Takeaways

- The dominant investment strategy for European hospitality is shifting from core acquisitions to value-add, specifically buying older assets for heavy CapEx and repositioning to meet modern standards.

- Labour shortages and wage inflation are the overwhelming factors exerting the greatest downward pressure on Gross Operating Profit (GOP) margins in the European hospitality sector.

- Institutional private credit/debt funds have become the primary and largest source of new debt capital for complex value-add deals, filling the funding gap left by constrained traditional European banks.

Download the PDF of this 'GRI Hospitality Europe Spotlight' report here.

European Hospitality Outlook

Investor Profile and Asset Class Maturity

The hospitality real estate sector is moving beyond the traditional investment base of private equity and family offices to attract a greater number and variety of investors, including more traditional core investors who are now looking outside the conventional lease model.This influx of institutional money indicates that hotels are moving out of their former niche status and are becoming a targeted asset class for international investors, marking a positive, long-term structural change for the market.

Southern European Markets Outperforming Northern Europe

Southern European markets, particularly Spain and Italy, are currently outperforming Northern and Central European countries, a trend underpinned by strong macroeconomic health, surprisingly low unemployment rates in some countries including Italy, and manageable inflation rates.This regional advantage is partly due to Southern Europe’s leisure-driven market, benefiting from the robust long-term demographic trend of increased spending on leisure, alongside Northern and Central Europe’s struggle with higher operational costs, such as labour and energy, slowing their post-COVID recovery.

Divergent Investment Strategies and Focus Cities

Investors are focusing heavily on major gateway cities and the luxury hotel segment, with Rome, London, Paris, and Madrid highlighted as the most compelling cities for investment in this sub-sector over the next three years.While private equity investors are targeting large, integrated, and often freehold resort businesses across the Mediterranean for value-add renovation and rebranding, core investors like German institutions are constrained to long-term lease agreements and are predominantly focused on resilient, branded economy and full-service three- or four-star hotels in key cities such as Rome and Milan.

Headwinds from Labour Costs and Taxation

Although the availability of labour is showing signs of normalisation, the costs associated with the workforce continue to rise, with staff housing in resorts and smaller cities being a major issue.Furthermore, rising taxation and property-related levies are emerging as a significant new headwind, driven by European governments seeking novel funding sources. In the UK, property taxes for hotels are more than doubling, posing a serious threat to the bottom line.

Underserved Mid-Market Segment

A clear bifurcation in demand is emerging, with investors and guests gravitating towards either the ultra-luxury, five-star hotel segment or the branded economy sector, suggesting a 'U-shaped' preference.However, this trend has exposed a potential market gap, as the mid-market segment (full-service, three- to four-star hotels) is underserved, with ageing existing stock in major cities including Rome, leading to unsustainably high average daily rates without a corresponding rise in quality.

(Credit: GRI Institute)

(Credit: GRI Institute)Hospitality Investments

Cashflow Over Geography

While geographical factors were once key to hospitality investment, the current focus is securing assets with strong cashflow potential, rather than being restricted to specific regions. This strategy involves acquiring assets at a higher yield than traditional institutional investors, financing them effectively, and implementing strong operational management to generate a good cash-on-cash return.Such an approach allows investors to hold assets for a longer duration, mitigating the need for immediate institutional buyer presence and ensuring resilience in various market conditions.

Niche and Alternative Hospitality Sectors

A clear thematic shift in the hospitality market is towards specialist segments, with outdoor hospitality and wellness-inspired assets emerging as particularly attractive due to their resilience and high growth potential.Outdoor hospitality (campsites) proved resilient during the COVID-19 pandemic, is cost-efficient, and offers significant value-add opportunities through operational improvements like dynamic pricing and adding mobile homes to significantly boost revenue per pitch.

Wellness-inspired assets, often acquired at non-institutional single-digit multiples, are benefiting from a significant cultural tailwind driven by consumer demand for health, longevity, and experiences, providing exciting growth equity opportunities.

Operator-Owner Alignment

Regardless of the contractual structure - be it lease, management agreement, or franchise - the key to driving value in operational assets is a true alignment of interests between the operator and the real estate investor.This alignment is achieved by ensuring the operator has “skin in the game”, such as strong performance guarantees or equity participation, to incentivise their full commitment to the business plan and gross operating profit (GOP) growth.

Successful value creation often involves using operational expertise to convert complicated, structured products into nimble, high-yielding assets, ultimately exiting to different types of buyers.

Creative Debt Financing

The current market is characterised by a scarcity of equity but a high availability of financing, which has created a substantial arbitrage opportunity for investors with access to capital.While traditional banks remain an option for core assets, alternative lenders and credit funds are filling a crucial gap by offering more flexible and increasingly competitive platform-level financing for non-traditional or esoteric hospitality products like wellness and outdoor assets.

The increasing supply and competition in the debt market, particularly from credit funds, is driving margin compression and offering advantageous financing solutions that accelerate the equity market's recovery.

Exit Strategies

An effective exit strategy in the current uncertain climate requires acquiring quality assets and simultaneously building time through robust cashflow generation.The ultimate target is the institutional core capital buyer, but since they are currently scarce, generating strong cashflow allows investors to wait for their inevitable return without negatively affecting returns.

Furthermore, for development or value-add projects, the optimum time to exit may be immediately after opening or just before a CapEx phase, allowing the seller to realise maximum value and leaving tangible value-add opportunities for the next buyer.

(Credit: GRI Institute)

Value-Add Strategies in Hospitality

Redefinition of Value-Add Investment

The expected wave of deeply discounted distressed assets following industry shifts, has largely failed to materialise in a meaningful way. Consequently, value-add is less about securing a low entry price and more about creating a cheap basis through robust operational enhancements, strategic capital investment, and leveraging opportunities to generate returns.True opportunity is often found in complex situations, such as buying non-performing loans (NPLs) related to hospitality assets, where few investors are willing to play.

Geographic Diversification

The market is experiencing diversification of investment away from traditional hotspots. Spain is presenting a strong resort platform, with similar potential emerging in Italy, however the challenges of scaling is limiting this potential, largely due to a lack of international branding.Greece has emerged as an easier market for growth, while countries like Croatia, Montenegro, and Albania are increasingly viewed as sensible, non-traditional countries for future entry, particularly benefiting from a growing number of visitors from Central and Eastern Europe (CEE) who seek decent, affordable family hotels.

Industrial Specialisation and Strategic Differentiation

Successful value creation is increasingly dependent on becoming industry specialists, moving beyond simple real estate transactions to mastering the operational levers of the business. This expertise involves the meticulous analysis and transformation of assets across revenue management, cost control, distribution, and rebranding, where the value-add is rooted in the industrial knowledge to identify and unlock upsides that are not obvious to non-specialist financial buyers.This capability is critical for tackling challenges in the mid-market segment, which is highly exposed to cost pressures like wage and energy increases.

Value creation also extends beyond mere CapEx to crafting a distinctive and unique guest experience that differentiates the product from competitors, often involving partnerships with fashion brands, art galleries, or third-party food and beverage (F&B) operators.

Specifically for F&B, in-house concepts rarely succeed without attracting external commercial traffic, necessitating either leasing out the space to high-calibre external partners or a strategic focus on very high-quality offerings to integrate the hotel with the local community.

(Credit: GRI Institute)

Hospitality Operations

Regulatory Ambiguity

A significant operational pressure for innovative operators, particularly those employing hybrid models such as co-living and serviced apartments, stems from the lack of clear and adaptable normative and regulatory frameworks.The current implant of laws and public administration often fails to keep pace with the evolution of these new hospitality models, creating confusion and difficulty in fitting into existing governmental "boxes".

For businesses operating across multiple international markets, managing this regulatory complexity alongside international scaling and maintaining consistent standards across different jurisdictions presents a primary challenge.

Technology in Operational Efficiency

Technology is central to the success and scalability of new hospitality operators, enabling them to achieve GOP margins of 55-60%, significantly higher than traditional models.The highest return on investment comes from building an entire in-house, fully automated tech ecosystem, rather than relying solely on external, third-party solutions.

Key innovations include developing proprietary revenue management algorithms that cater to hybrid models with mixed-stay lengths, and automation tools like AI-driven chatbots and in-house cleaning checker applications, which substantially reduce labour and operational costs

Differentiation Through Guest Experience

The market for hospitality is becoming increasingly polarised, with different models catering to distinct customer demands and use cases. Tech-enabled, lean-service apartment models thrive in urban, central locations by offering an efficient, seamless digital experience - likened to a car-sharing app - where guests prioritise independence and experiencing the local city environment.In these cases, effective expectation management, clearly communicating the digital nature of the check-in process, is crucial to ensuring a positive guest experience and avoiding negative reviews.

By contrast, “destination” concepts rely on creating a community and offering a full-service environment with common areas, events, and personal support, appealing to a different, often membership-based, clientele willing to pay a premium for the complete package.

In-House Technology

Developing proprietary technology is viewed not just as a cost-saving measure but as a strategic defence of margins and a crucial element for business continuity and flexibility.Operators are concerned that becoming overly reliant on third-party Software as a Service (SaaS) providers could lead to dependency, increased prices, and the erosion of their competitive edge, similar to the leverage wielded by Online Travel Agents (OTAs).

The 'born-without-legacy' approach of newer brands allows them to build fully open, API-driven systems that are highly flexible, easily adaptable for new acquisitions, and specifically tailor-made for operational efficiency, unlike the closed, age-restricted legacy systems of traditional operators.

Competition in Real Estate Acquisition

The current scarcity of new greenfield developments means growth for these tech-enabled operators relies heavily on converting existing buildings, notably tired hotels and structural offices, which their lean models are uniquely positioned to manage profitably.However, dynamic expansion and competition among operators are leading to an acquisition-side challenge where developers and real estate brokers, seeking to maximise asset value, are driving up rents.

This practice is creating an unsustainable environment, with some operators prepared to sign fixed lease agreements at highly inflated rents that do not align with realistic operational back-up, a scenario that poses a significant threat to long-term market sustainability.

(Credit: GRI Institute)

Luxury Hotels & High-End Experiences

Redefinition of Luxury

The concept of luxury in hospitality has shifted significantly, moving beyond mere ostentatious design and brand recognition to encompass personalised, consistent, and experiential offerings.True luxury is now increasingly defined by the ability to deliver unique, memorable experiences, such as extreme isolation or highly customised services, which can command ultra-high average daily rates (ADR) even in minimalist or simple settings, underscoring that operational execution and the emotional connection created with the guest are often more critical than brand standard or hardware alone.

Advantages and Challenges in Branding

From an investor's perspective, a strong luxury brand remains fundamental to asset value, as the brand provides a crucial marketing tool and significant power placement, particularly important for investors with limited experience in the complex hotel sector.Established luxury brands offer clients a recognised standard of quality and consistency globally, fostering strong customer loyalty - as exemplified by Four Seasons and Mandarin - which directly translates into a more comfortable investment strategy and a higher likelihood of achieving sustainable growth in ADR and occupancy.

However, significant tension exists between developers and luxury brands, as top-tier luxury brands generally operate exclusively through management agreements to maintain absolute control over all operations and brand standards, making a franchise model impossible.

This insistence on control can pose a problem for owners/developers who have a specific, pre-built concept or vision - such as in emerging segments like wellness and longevity - which may not align completely with the brand's rigid requirements, forcing the investor to consider developing their own independent brand.

High Development Costs and Time-to-Market

The development of new luxury and high-end concepts faces a substantial challenge from increasing costs, particularly involving high demand greenfield sites, making such projects increasingly less viable.Furthermore, the long time-to-market is deterring closed-end private equity funds seeking quick returns to engage with these projects, suggesting that luxury hotel development is becoming more of a domain for high-net-worth individuals or long-term private investors.

Branded Residences and Service Apartments

Branded residences are emerging as a major focus area, providing high-net-worth individuals (HNWIs) with international luxury homes that offer full hotel services and the ability to rent out the unit through the hotel manager when not in use.This model commands a significant premium, typically selling for around 30% higher than the normal real estate market, as the brand's services and consistency maintain the asset's long-term value and attract a dedicated clientele seeking a sense of community and proven management.

(Credit: GRI Institute)

Urban Hotels

Bifurcation of Urban Hotel Product Design

The urban hotel product is evolving along two distinct lines: the ultra-luxury, high-margin asset, and the lean, digitally-operated, new-generation hotel, with the traditional three-to-four-star mid-market facing increasing margin compression.This bifurcation is driven by both supply-side necessity - including high hard costs and limited building stock requiring either highly efficient or high-margin products - and an unsaturated demand for both extremes of the market.

The lean, tech-enabled model, such as serviced apartment brands, is capitalising on a new generation of independent, smartphone-savvy travellers who prefer a digital-friendly, efficient experience with more space and local engagement over traditional full-service offerings, resulting in a predictable and low-volatility profit and loss (P&L) statement.

Data-Driven Operational Models and Asset Resilience

Operators are leveraging technology and extensive data to inform underwriting, predict performance, and adapt product design, moving beyond reliance on traditional property data to incorporate platform-scraped data, internal asset performance, and even insights from competitor networks.This data-driven approach, combined with asset-light and lean operational models, enables them to offer a superior product at a better price while also providing investors with a more resilient business model that is less exposed to cost volatility from F&B and personnel, unlike traditional full-service hotels.

The success of these models, even in secondary locations, is rooted in the proven demand for efficient, flexible, and locally-integrated accommodation, suggesting that demand remains the primary filter for investment decisions.

Geographical Performance

There is clear divergence in market performance across Europe, with Southern European destinations like Spain, Italy, and France demonstrating remarkable strength, largely driven by resilient leisure travel and growing demand.Conversely, while Germany's market benefits from inner-German travel, it faces macro-economic headwinds and significant dependency on the struggling corporate travel sector, leading operators to seek expansion in more stable and leisure-focused markets, such as the Nordics, Italy, and Portugal.

The long-term outlook for cooler, more stable markets like the Nordics is considered positive due to attractive macro trends and political stability, despite higher barriers to entry.

Evolving Investor Profiles and Capital Allocation Strategies

A significant shift in the investor landscape has been observed, with a move away from traditional institutional capital, like pension funds and insurance companies, which sought super-stabilised, fixed-rent lease agreements, towards private investors.This transition was accelerated by the COVID-19 pandemic, which exposed the vulnerability of long-term fixed leases, leading to a focus on variable rents or Hotel Management Agreements (HMAs).

Contemporary investors are predominantly private equity, family offices, and those seeking to hedge alternative portfolios, with a greater appetite for value-add opportunities and projects in secondary Italian cities like Bologna, Torino, and Naples, though this presents a challenge in justifying non-prime locations to foreign investment committees.

Alternative and Development Financing

Traditional bank lending for hospitality projects is constrained, primarily due to banks' aversion to development, planning, and regulatory risks, particularly in Southern Europe. As a result, alternative lenders and debt funds have become increasingly vital, offering greater flexibility and higher loan-to-cost (LTC) ratios - often between 65% and 80% - to finance complex construction and conversion projects.While alternative financing is generally more expensive, with rates ranging from 7-8% to potentially higher, its willingness to underwrite risks such as archaeological or permitting delays makes it the practical solution for development, a space where local banks are often perceived as too costly for the risk profile.

(Credit: GRI Institute)

Resorts & Leisure

Importance of Local Identity

The leisure resort product is currently an attractive area for investment, with operators emphasising that a successful resort must be rooted in the place where it is located. This belief drives the necessity for a strong connection to the local community, which may require more flexible standards for global brands operating resorts in the Mediterranean.This is often in contrast to city-centre hotels where brand standards are critical, as leisure guests are typically seeking a very different, immersive local experience.

Global Brand vs. Local Operator

A key challenge is the tension between leveraging a global brand for financing and maintaining a unique product identity. While investors often prefer the perceived lower risk and distribution power of an international brand, a specialised, local or niche brand can often deliver greater revenue and a better customer experience, especially in the complex resorts segment.Some brands are now attempting to create a resort-like atmosphere even in city locations by developing extensive service-led experience programmes.

Technology in Driving Revenue

For continued success in this sector, revenue growth must come from driving overall revenue rather than relying solely on further increases in ADR. This is achieved through upselling and technology.Specifically, resort operators are investing in custom-built reservation systems capable of creating complex, personalised packages that traditional hotel systems cannot offer, and implementing AI and CRM tools to enable hyper-personalisation and better meet customer demand.

Addressing the Long-Term Labour Challenge

Labour shortages and rising operational costs are significant, long-term challenges to industry profitability, particularly in the high-service leisure segment where human touch is critical.Operators are exploring digitalisation, automation, and robotics for non-guest facing tasks, such as the cleaning of public areas, to mitigate the impact of labour costs. However, there is a strong commitment to preserving the human element in high-touch guest interactions, such as with concierges and restaurant attendants, which are considered essential to the resort experience.

(Credit: GRI Institute)

Flexible Hospitality Models

Risk of Unsustainable Rent Offers

A major concern is the prevalent lack of market discipline among operators, particularly the tendency to overplay and push rents to unsustainable levels to secure assets. Driven by VC funding and growth targets, many operators are signing deals with rent coverages that are not viable, creating a risk of future failures.There is a need for operators to maintain discipline, walk away from unsustainable offers, and perform solid underwriting based on common sense and realistic market projections, especially considering the current economic slowdown in major European economies.

Subscription-Based Lifestyle

The market is experiencing a generational shift towards a "subscription lifestyle," where consumers prioritise flexibility, convenience, and a one-bill solution over long-term commitments and traditional homeownership.This trend is fuelling demand for flexible hospitality models, which offer a high level of customer satisfaction by addressing the limitations of the traditional residential market, such as tedious contracts and a lack of flexibility.

Operators are successfully commanding a premium - around 20% above average rental rate - as guests are willing to pay for this convenience, service, and the elimination of associated moving costs and contractual worries.

Regulatory Challenges and Supply Constraints

Regulatory pressure, particularly in Spain and Portugal, is significantly impacting the available supply in major European cities. Municipalities are making licenses harder to obtain, primarily to combat short-term rentals and create more control around rents, which in turn benefits longer-term operators by removing competition.While these regulations create delays and challenges for development pipelines, some progressive city planning, such as the City of London's push for office-to-hotel conversions, demonstrates how a forward-thinking approach can positively address the housing crisis and stimulate growth in the hybrid hospitality sector.

Optimising Asset Layout for Long-Term Viability

There is debate around the optimal unit mix and layout necessary to ensure positive financial performance and high occupancy rates. Operators generally favour a majority of smaller units, with studios and one-bedroom apartments forming the core of the portfolio - for example 75% studios, 25% one-beds.The most inefficient layouts are often mid-sized units (60-100 square metres) which offer a large living room but do not significantly command a higher ADR. Meanwhile, smaller units, full kitchens - as opposed to kitchenettes - and strategically designed common spaces - avoiding overly large, unused amenity space - are key differentiators that drive longer stays, higher occupancy, and a more robust business case.

(Credit: GRI Institute)

Debt & Credit In Hospitality Deals

Alternative Credit in Southern Europe

Alternative credit has become an essential solution, particularly in Southern European markets like Italy and Spain, primarily due to the withdrawal of traditional banks from certain types of financing.While alternative lenders are stepping in to fill this void, smaller-scale, investment opportunities struggle to secure debt financing. Mid-market transactions, typically ranging from EUR 10 million to EUR 100 million, can be deemed too small for the costly and complex administrative and regulatory structures required by alternative lenders.

Working with alternative credit, particularly in challenging regulatory environments such as Italy, involves significant structural and procedural complexity that often surprises sponsors.

The process requires compliance with intricate structures such as mortgage bonds, securitisation vehicles, or money issuance in jurisdictions like Luxembourg, which can result in substantial legal and setup fees, making the process considerably more costly and complex than traditional mortgage loans.

Although this complexity can act as a barrier to entry, enabling alternative lenders to charge higher margins, the trade-off is often a much faster transaction closing time compared to traditional banks.

Underwriting and Risk Perspective

Alternative lenders employ a rigorous underwriting approach that is often more akin to equity investment, demanding extensive diligence, new securities, and detailed business plans, which contrasts with the reliance banks place on pre-existing customer track records.The perspective of alternative lenders focuses on downside protection, necessitating a strong security position and a clear exit strategy, typically either refinancing or a sale.

Furthermore, the market for alternative lending is seeing an increase in the quality of borrowers, leading to a focus on non-bankable situations like recapitalisation and equity releases, which are more complex but offer better security.

Regulatory Pressure and the Challenge to Commercial Banks

Commercial banks are facing increasing difficulty in real estate lending, primarily due to regulatory reasons, which are set to intensify with the introduction of Basel IV. This regulatory environment is ironically making it easier and less capital-intensive for banks to provide back leverage to private credit funds rather than engaging in direct lending, despite the underlying risk being similar or even structurally higher in a loan-on-loan context.This trend of moving risk from regulated to non-regulated entities is a major concern for financial stability, with the consensus that the commercial banks' reduced capacity to lend poses a systemic problem for the wider economy.

(Credit: GRI Institute)

Survey Results & Analysis

This section presents the results of the survey conducted among a group of Europe’s most prominent real estate market leaders active in the hospitality sector, which took place during the GRI Hospitality Europe 2025 conference in Rome.The survey was designed to capture expert perspectives on the near-to-medium-term outlook by addressing four core areas of concern for investors, operators, and developers. Specifically, respondents were polled on their intended primary investment strategy over the next 24 months, their predictions for the highest RevPAR growth and investment returns across European hospitality segments in the next 12-18 months, the operational factors currently exerting the greatest downward pressure on GOP margins, and the anticipated largest source of new debt capital for value-add deals over the next 12 months.

The findings herein offer a comprehensive benchmark of industry consensus on capital allocation, performance expectations, key risks, and the changing structure of hospitality real estate financing.

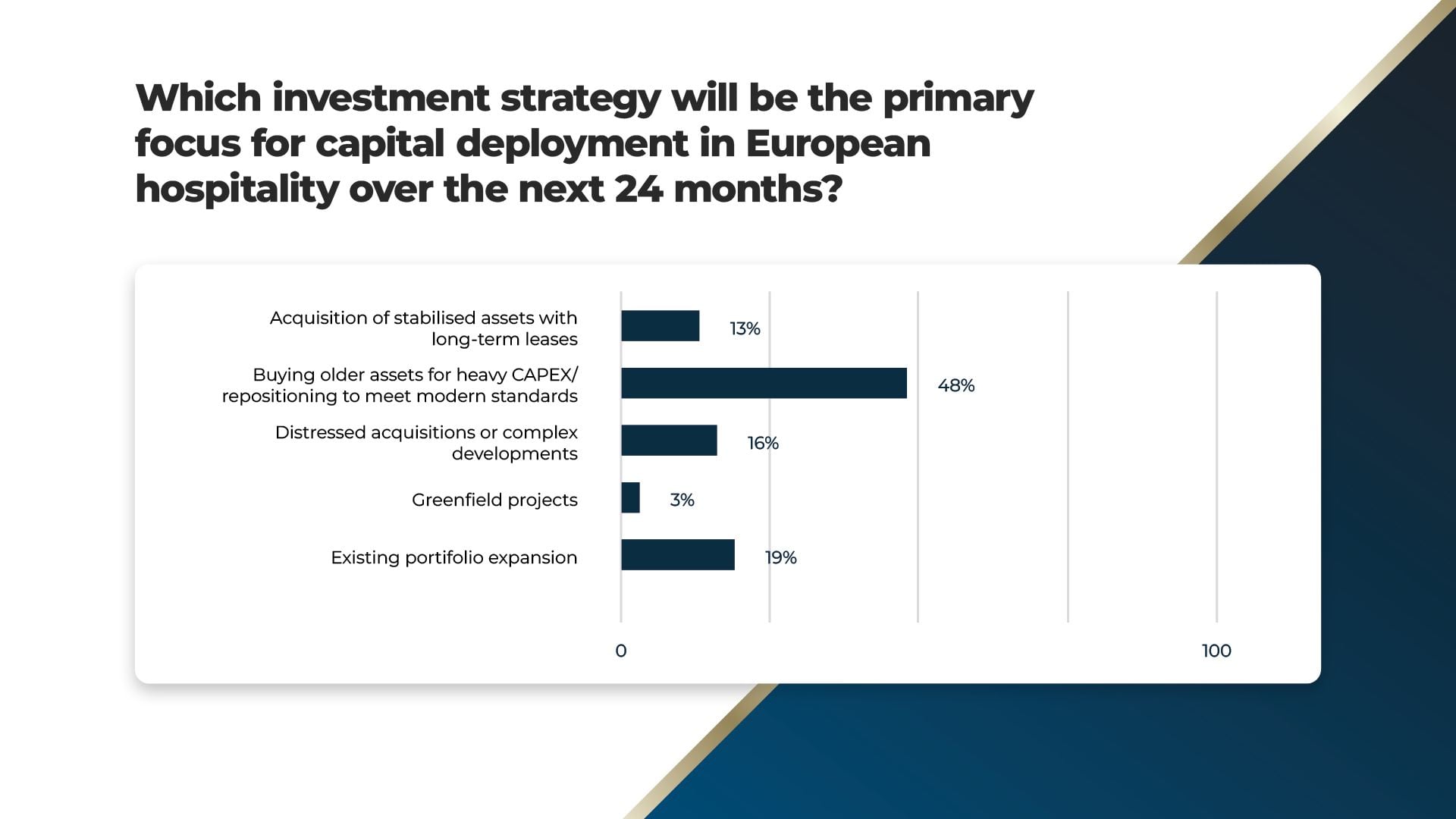

Which investment strategy will be the primary focus for capital deployment in European hospitality over the next 24 months?

The poll results clearly indicate a strong preference among European hospitality market leaders for value-add strategies over core or opportunistic investments for the next 24 months.

Buying older assets for heavy CapEx/repositioning to meet modern standards was the overwhelming primary choice, securing 48% of the vote. Existing assets offer a better entry price point and a clearer path to creating value, especially in a market with constrained new supply and increasing demand for properties that meet modern ESG standards.

The remaining votes were dispersed among lower-risk and higher-risk strategies. The low number of votes for greenfield projects, at just 3%, highlights market leaders’ hesitance to commit to the long timelines, elevated construction costs, and regulatory uncertainties associated with building entirely new developments, further reinforcing the dominant strategy of leveraging and enhancing existing real estate stock.

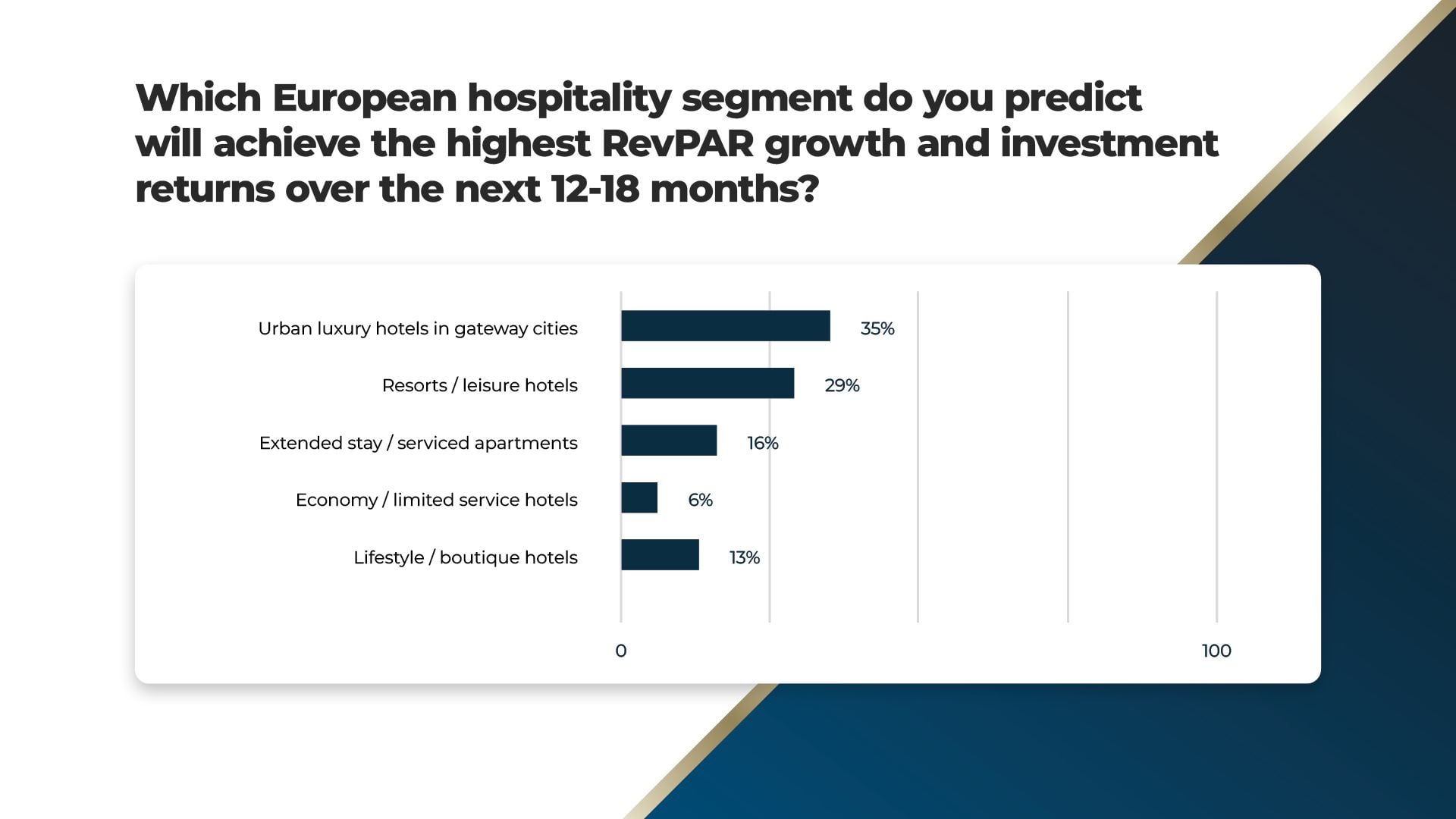

Which European hospitality segment do you predict will achieve the highest RevPAR growth and investment returns over the next 12-18 months?

European hospitality real estate market leaders demonstrated confidence in urban luxury hotels in gateway cities for achieving the highest RevPAR growth and investment returns over the next 12-18 months, securing 35% of the vote.

This preference reflects the expectation of a sustained resurgence in high-end international and corporate travel to Europe's major city hubs, where luxury assets possess strong pricing power and benefit from limited new supply.

Following closely is the resorts / leisure hotels segment with 29% of the vote, indicating confidence in the continued strength of the post-pandemic leisure travel boom, which often prioritises experiential, high-value stays in destination markets.

The low confidence in the economy/limited service segment (6%) is particularly notable, suggesting market leaders anticipate greater pressure on lower-tier assets from factors like cost inflation and price-sensitive customers, which could limit RevPAR growth despite sustained demand.

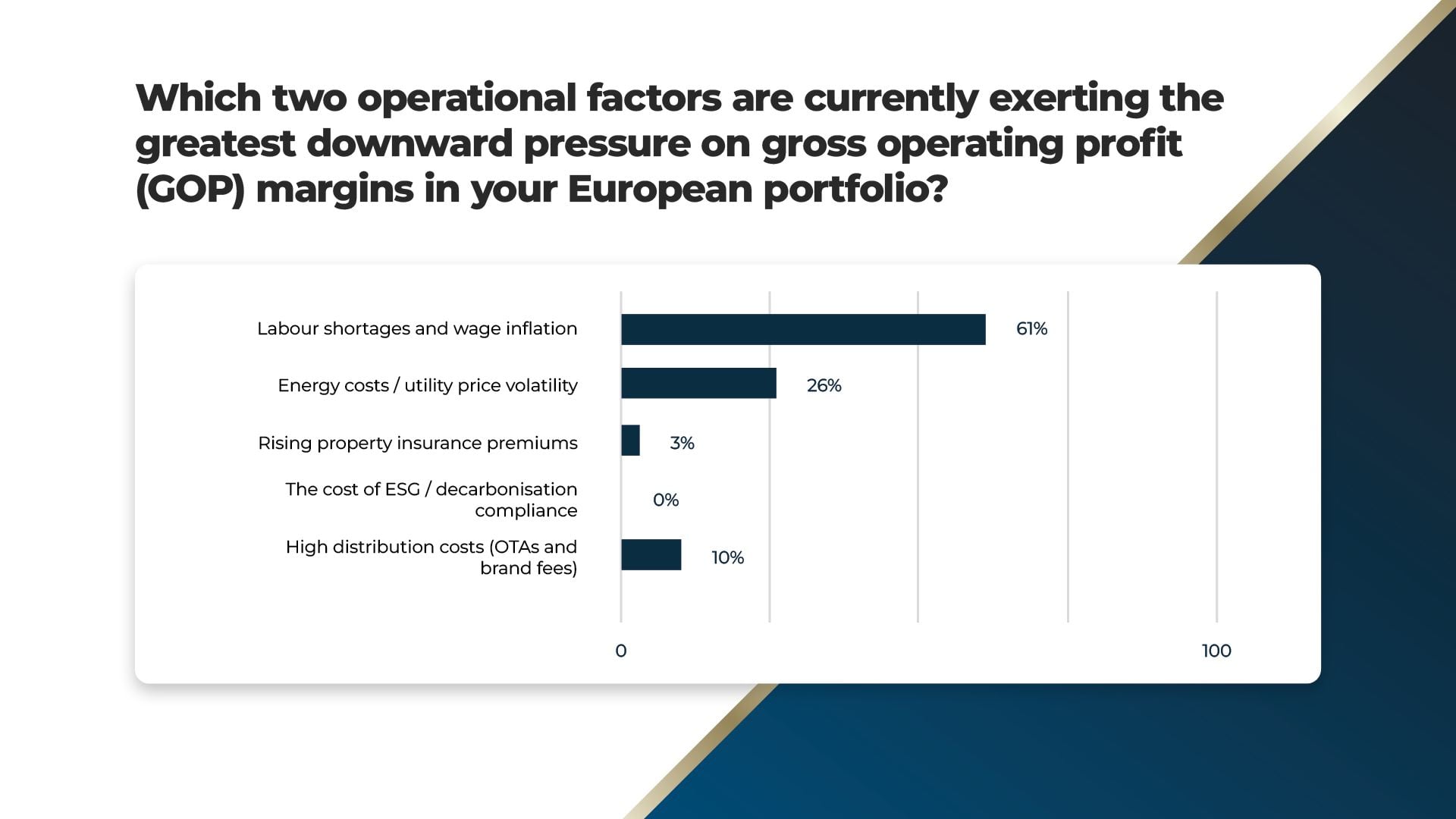

Which two operational factors are currently exerting the greatest downward pressure on gross operating profit (GOP) margins in your European portfolio?

The poll results clearly identify labour shortages and wage inflation as the overwhelming factors exerting the greatest downward pressure on GOP margins in the European hospitality sector. The cost and availability of personnel - a crucial operational component in a service-heavy industry - is the single most acute pain point for European real estate market leaders. The need to offer higher wages to attract and retain staff, compounded by chronic shortages, is directly eroding the profitability of hospitality assets.

Following labour, energy costs / utility price volatility was cited by 26% of participants as the most impactful factor. While a substantial concern, its impact is viewed as less severe than the labor crisis, indicating that despite high prices and market swings, energy management may be more controllable or less structurally challenging than workforce issues.

The remaining factors collectively account for only 13% of the votes. This distribution highlights a strategic focus on variable operating costs (labour and utilities) over more fixed or less immediately pressing expenses, suggesting that operational resilience against day-to-day cost inflation is the primary challenge facing the market leaders.

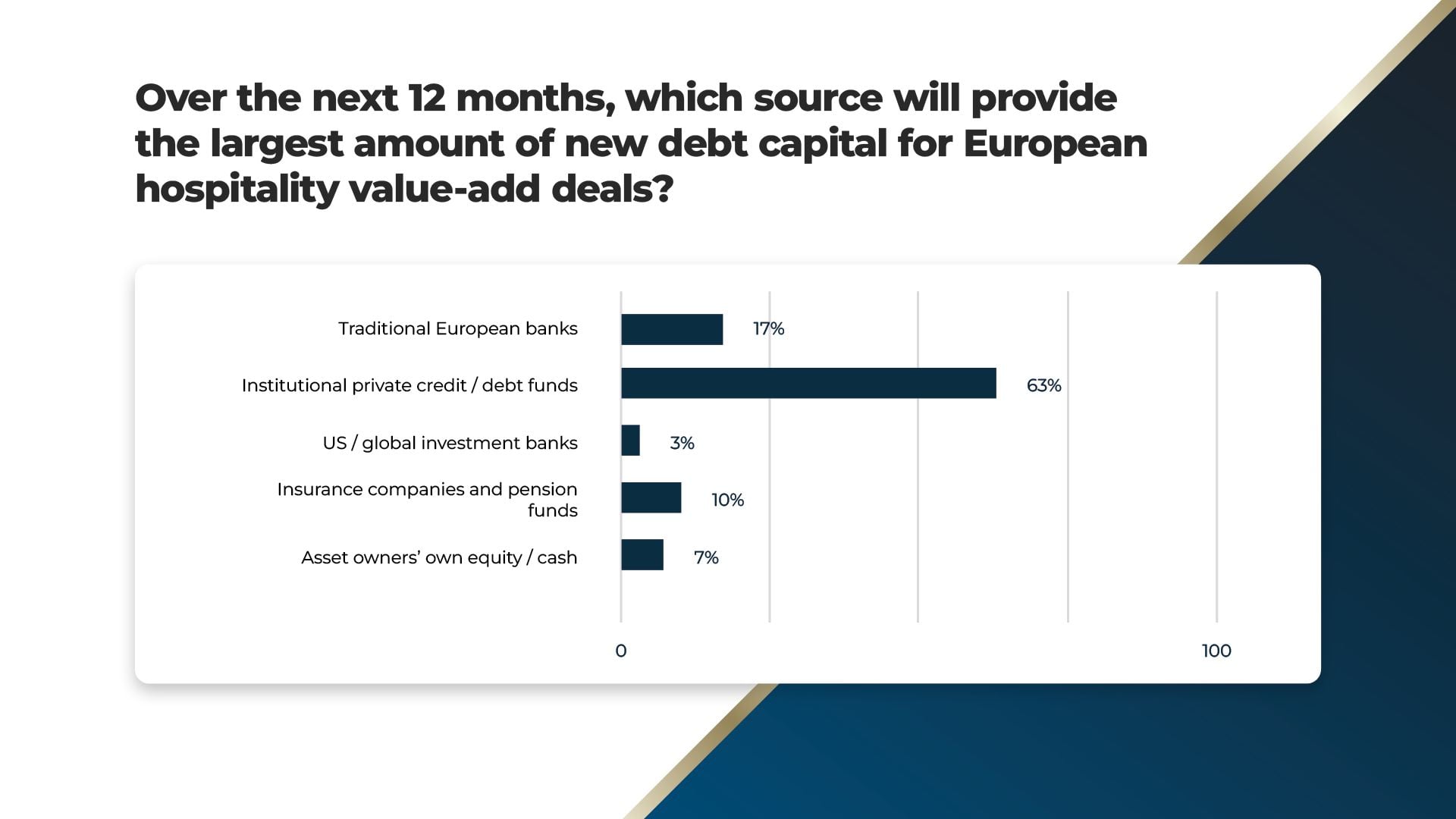

Over the next 12 months, which source will provide the largest amount of new debt capital for European hospitality value-add deals?

The poll results clearly indicate a significant shift in the landscape of debt capital provision for European hospitality value-add deals, moving away from traditional sources. The overwhelming majority of market leaders (63%) believe that institutional private credit / debt funds will be the largest source of new debt capital over the next 12 months.

There is a growing dominance of non-bank lenders in financing riskier, higher-yield real estate strategies, particularly in the value-add space. This trend is consistent with a broader post-Global Financial Crisis environment where increased banking regulation has constrained the ability of traditional European banks (receiving only 17% of the vote) to lend to complex or higher loan-to-value (LTV) transactions, creating a major funding gap that private credit funds are filling.

The remaining sources of capital - insurance companies and pension funds (10%), asset owners' own equity/cash (7%), and US/global investment banks (3%) - lag far behind, suggesting they play a more specialised or supplementary role in this segment of the market.

Thank you to our discussion moderators, co-chairs, and all participants for their contributions to the valuable discussions that unfolded at GRI Hospitality Europe 2025.