GRI Institute

GRI InstituteThe Italian GRI Barometer: PBSA and hotel upgrades take centre stage

Discover how real estate decision-makers are leveraging adaptive reuse and mainstream hotel repositionings to capture value amid restricted bank liquidity

June 11, 2026Real Estate

Written by:Henrique Cisman

Executive Summary

The Italian real estate market is currently navigating a pivotal period of transition, establishing itself as a robust geopolitical safe haven with transaction volumes climbing by 20% to reach EUR 12.5 billion.

On one side sits a highly compelling investment case, characterized by mid-cycle expansion, geographical diversification beyond traditional urban hubs, and exceptionally strong occupier demand across logistics and prime commercial offices.

On the other sits a complex execution environment shaped by consolidated post-pandemic construction costs, persistent administrative hurdles, and a clear credit friction as a traditional domestic banking system remains highly restricted.

What emerges is a clear path towards institutional maturity. Capital is aggressively moving into operationally intensive social and digital infrastructure - including PBSA and hotel repositionings - while developers increasingly turn to the adaptive reuse of obsolete commercial assets to help bridge the national housing deficit.

Ahead of Europe GRI 2026 Summer Edition on 8th-10th September in Paris, which will serve as the primary venue to continue the conversation, we take a look at the key data trends, value-creation strategies, and financing realities driving the Italian market forward.

On one side sits a highly compelling investment case, characterized by mid-cycle expansion, geographical diversification beyond traditional urban hubs, and exceptionally strong occupier demand across logistics and prime commercial offices.

On the other sits a complex execution environment shaped by consolidated post-pandemic construction costs, persistent administrative hurdles, and a clear credit friction as a traditional domestic banking system remains highly restricted.

What emerges is a clear path towards institutional maturity. Capital is aggressively moving into operationally intensive social and digital infrastructure - including PBSA and hotel repositionings - while developers increasingly turn to the adaptive reuse of obsolete commercial assets to help bridge the national housing deficit.

Ahead of Europe GRI 2026 Summer Edition on 8th-10th September in Paris, which will serve as the primary venue to continue the conversation, we take a look at the key data trends, value-creation strategies, and financing realities driving the Italian market forward.

Key Takeaways

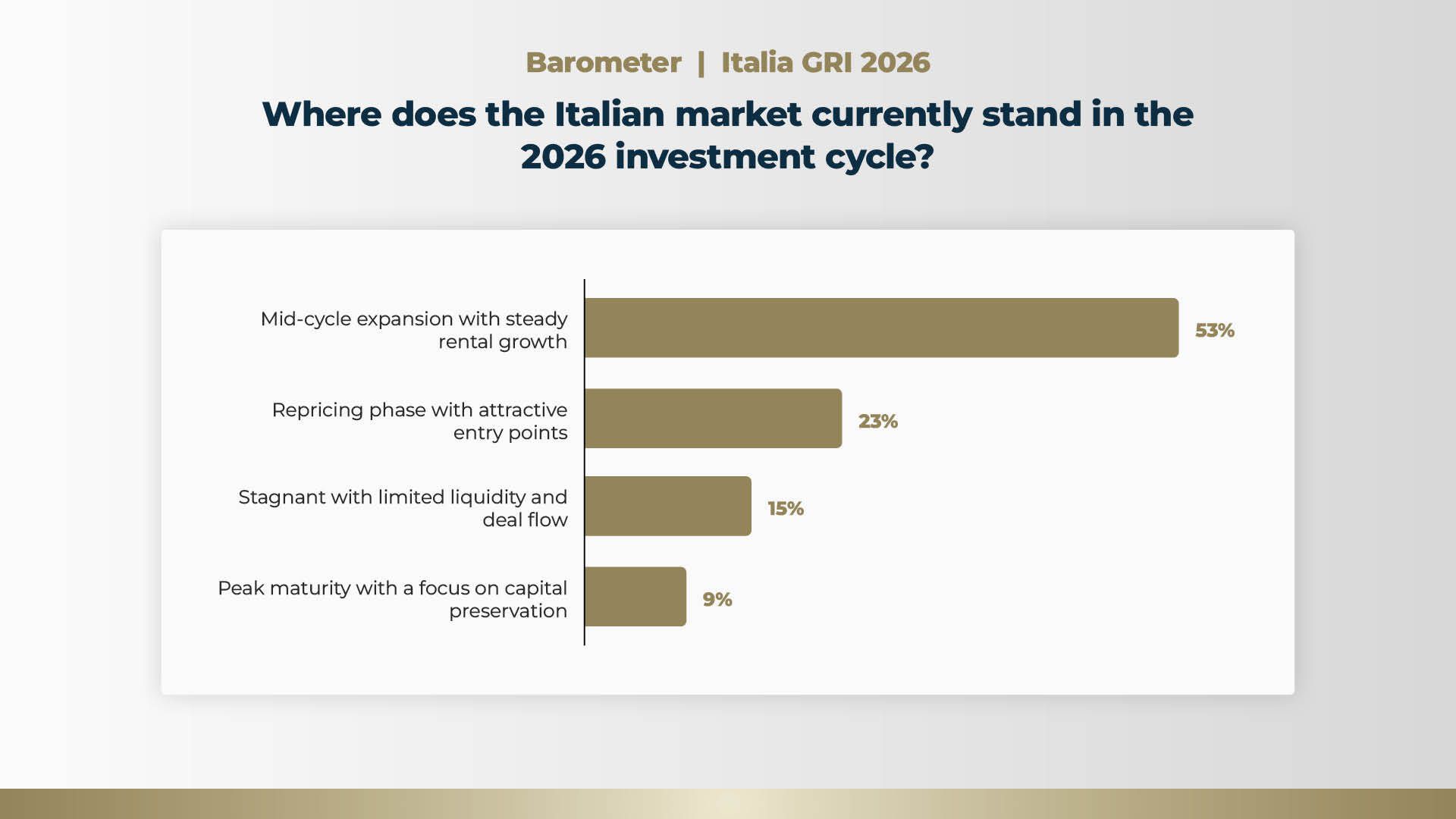

- More than three quarters of senior real estate leaders view the Italian market favourably, with 53% placing it in a mid-cycle expansion defined by steady rental growth and 23% identifying attractive entry points within a repricing phase.

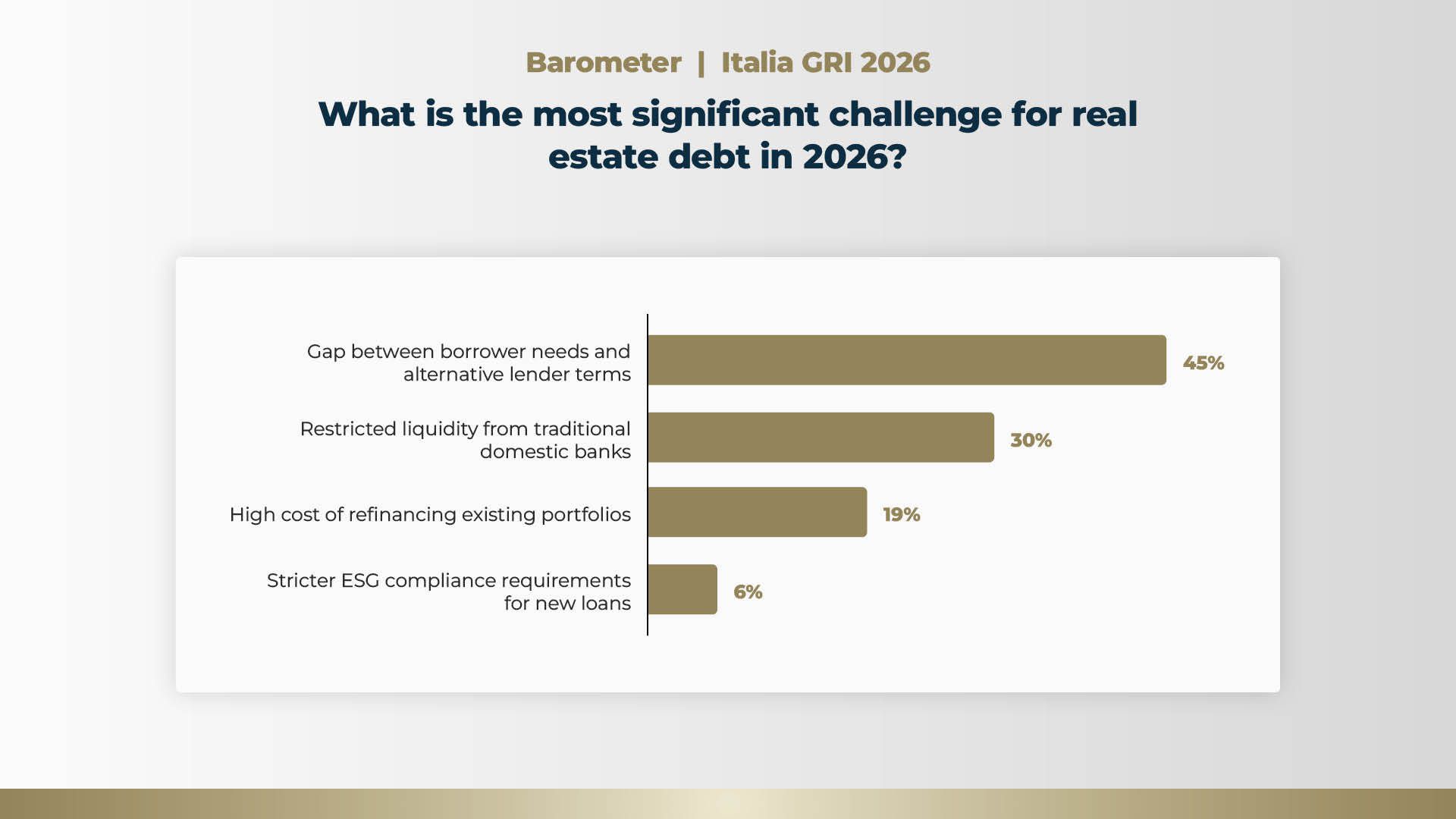

- Credit markets are experiencing severe friction, driven by a prominent gap between borrower needs and alternative lender terms for 45% of executives, alongside restricted liquidity from traditional domestic banks for another 30%.

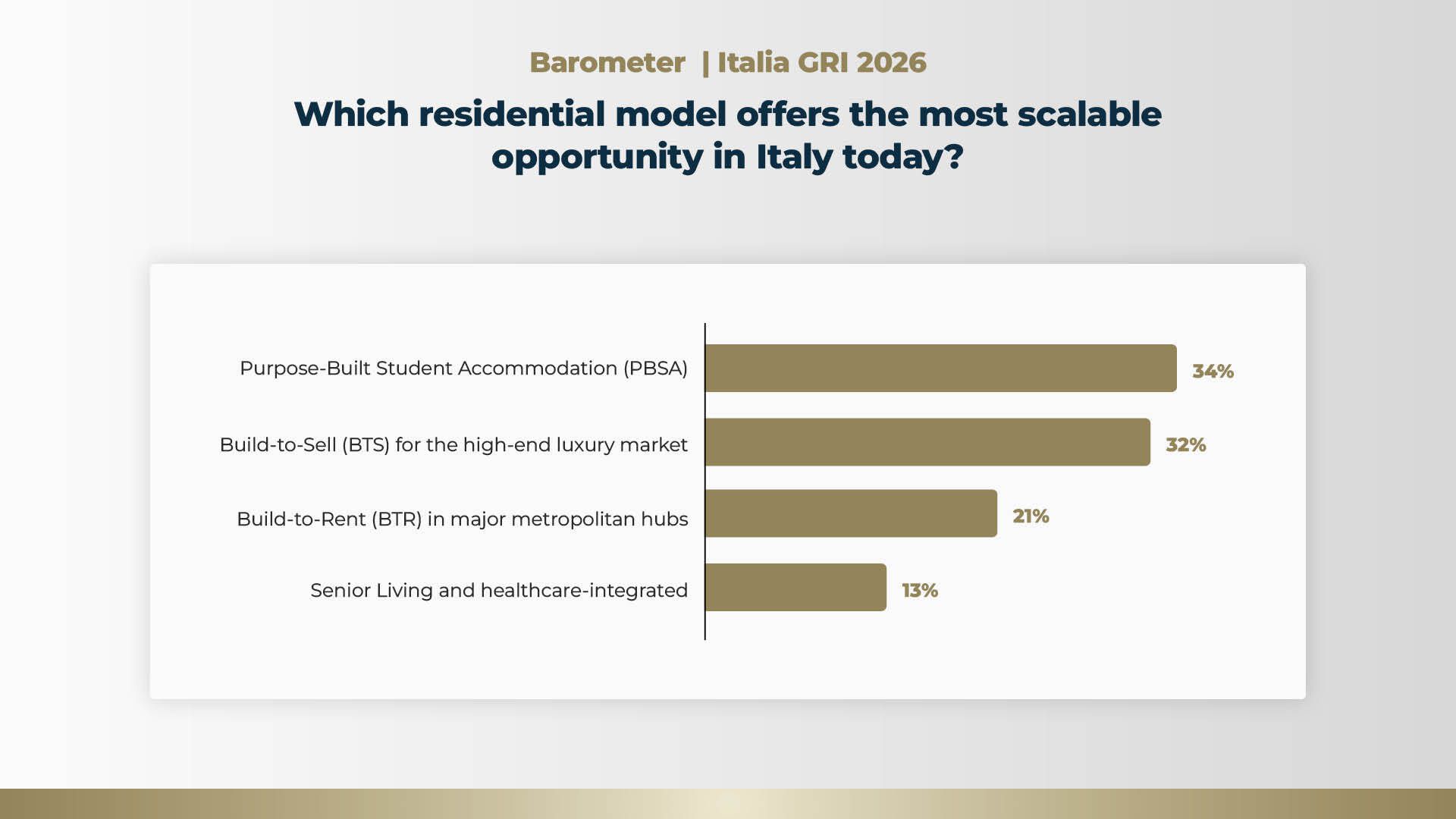

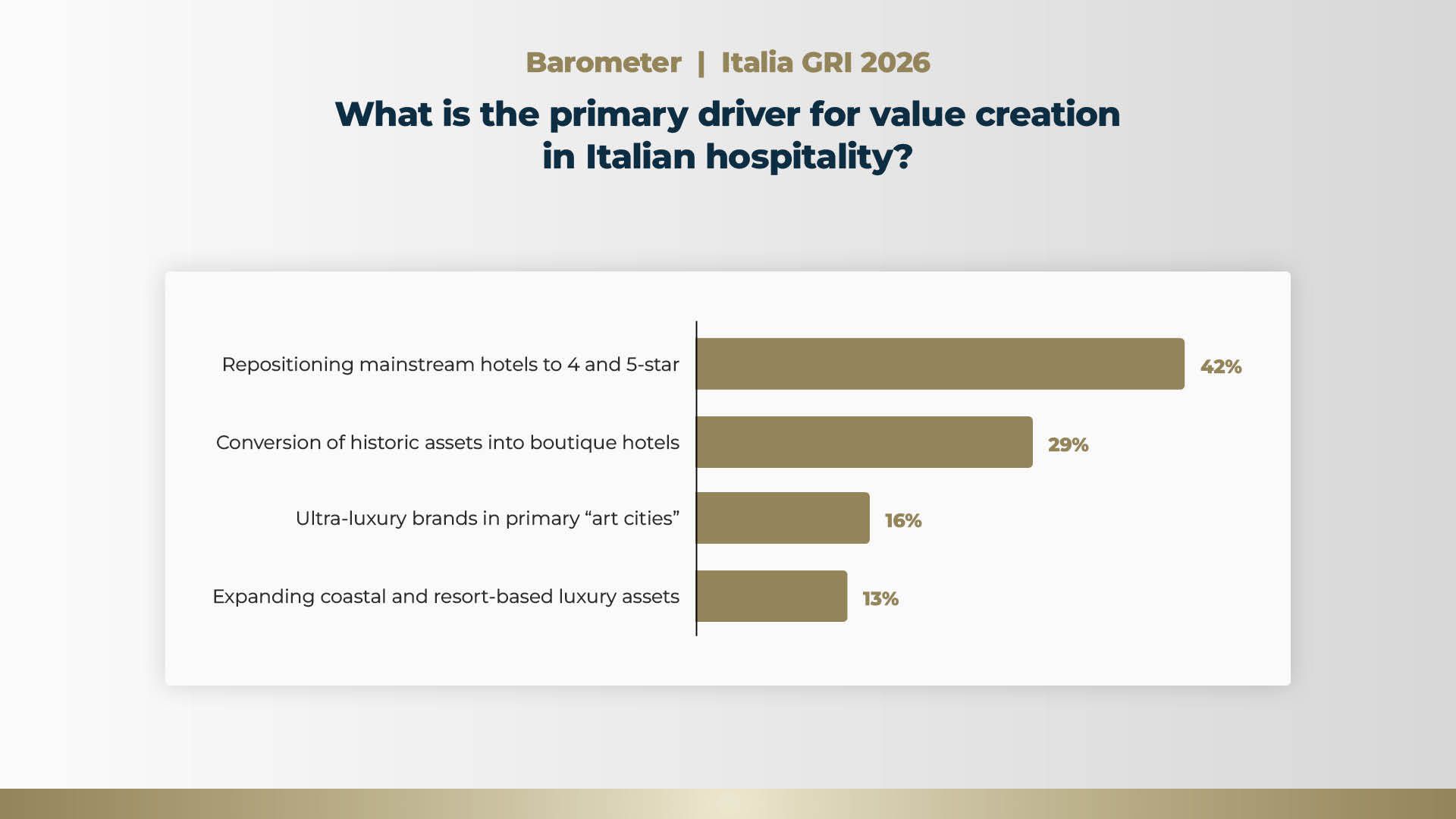

- Scalability and value creation are heavily tied to alternative assets, with 34% prioritizing PBSA, 42% focusing on repositioning mainstream hotels to four- and five-star standards, and 50% identifying commercial-to-residential conversion as the most viable strategy for obsolete stock.

The Italian Market in the 2026 Investment Cycle

The Italia GRI 2026 survey demonstrates a strong wave of optimism among senior real estate executives regarding the current standing of the Italian property market, that has firmly established a bottom and is currently moving through a robust recovery phase.

Backed by a 20% year-on-year surge in transaction volumes to EUR 12.5 billion, Italy is rapidly gaining traction as a stable geopolitical safe haven. This cyclical expansion is further paired with a healthy geographic diversification; capital is successfully moving beyond its traditional concentration in Milan and Rome, spreading structural liquidity across secondary national regions to capture higher yields.

Most Significant Challenges for Real Estate Debt

The financing landscape in Italy is experiencing a distinct structural friction as the market adapts to modern lending standards: 45% of senior real estate leaders point to the widening gap between borrower needs and alternative lender terms as the single most critical challenge facing real estate debt. This friction is exacerbated by traditional funding restrictions, with 30% of surveyed executives highlighting restricted liquidity from traditional domestic banks as a major industry bottleneck.

The remaining hurdles focus heavily on capital management and regulatory compliance. This indicates that while green standards are essential for institutional underwriting, the immediate mechanics of securing and structuring debt remain the more pressing operational issue.

A heavily bank-tethered system has become structurally constrained, opening up vast fields of opportunity for private debt providers to step in with bespoke solutions. However, alternative lenders are mandating highly disciplined underwriting standards, requiring substantial cash equity and pricing mid-market facilities around Euribor plus 600 basis points. This approach clashes culturally with local sponsors who have historically relied on aggressive leverage, creating the prominent market gap identified by the survey participants.

Scalability of Residential Models

As institutional capital increasingly moves toward digital and social infrastructure, the Italian living sector is witnessing a competitive race between varied residential asset classes.

Purpose-Built Student Accommodation (PBSA) is considered the most scalable model in Italy today, securing 34% of the executive vote. This is followed immediately by Build-to-Sell (BTS) platforms tailored for the high-end luxury market, which captured 32% of responses from the surveyed real estate leaders.

The middle and alternative segments of the residential market reflect a more measured appetite. Build-to-Rent (BTR) models in major metropolitan hubs were selected by 21% of professionals, while Senior Living and healthcare-integrated platforms gathered the remaining 13% of the vote.

PBSA is the primary pioneer for broader institutional living platforms due to its highly visible regulatory framework and predictable, recurring income streams. The high ranking of high-end BTS models further underscores a profound dichotomy currently defining the Italian residential landscape. Wealthy domestic and international buyers continue to fuel a highly resilient luxury segment, making quick-turn capital models highly attractive to developers.

In contrast, a 30% to 35% consolidation in post-pandemic construction costs, combined with a severe 27% deterioration in local price-to-income ratios over the last decade, continues to make mid-market BTR and affordable rental projects exceptionally difficult to pencil out without significant regional scale.

Primary Drivers for Value Creation in Italian Hospitality

The Italian hospitality ecosystem is undergoing a major institutional overhaul, moving rapidly away from its historically fragmented roots toward highly professionalised, international standards.

Senior industry figures view the repositioning of mainstream hotels into four- and five-star establishments as the primary driver for value creation, capturing 42% of the survey results. The conversion of historic assets into boutique hotels is also highlighted as a highly lucrative pathway, securing 29% of executive support.

In contrast, strategies tied directly to premium luxury tiers and resort assets command smaller percentages of the total sentiment. This distribution clearly signals that the greatest financial upside is currently found in upgrading and professionalising the massive, underserved mid-market and upscale segments rather than fighting for ultra-luxury market share.

Hospitality transaction volumes have jumped by 18% year-on-year to hit EUR 2.2 billion. With entry prices in the ultra-luxury tier reaching prohibitively high levels of EUR 1 million to EUR 1.5 million per key, international funds are intentionally bypassing asset saturation by converting offices and industrial stock into turnkey hotel products.

By utilizing forward-purchase structures and expanding geographically into secondary regions like Puglia, Sicily, and the Alps, smart capital is successfully capturing sustainable average daily rate growth.

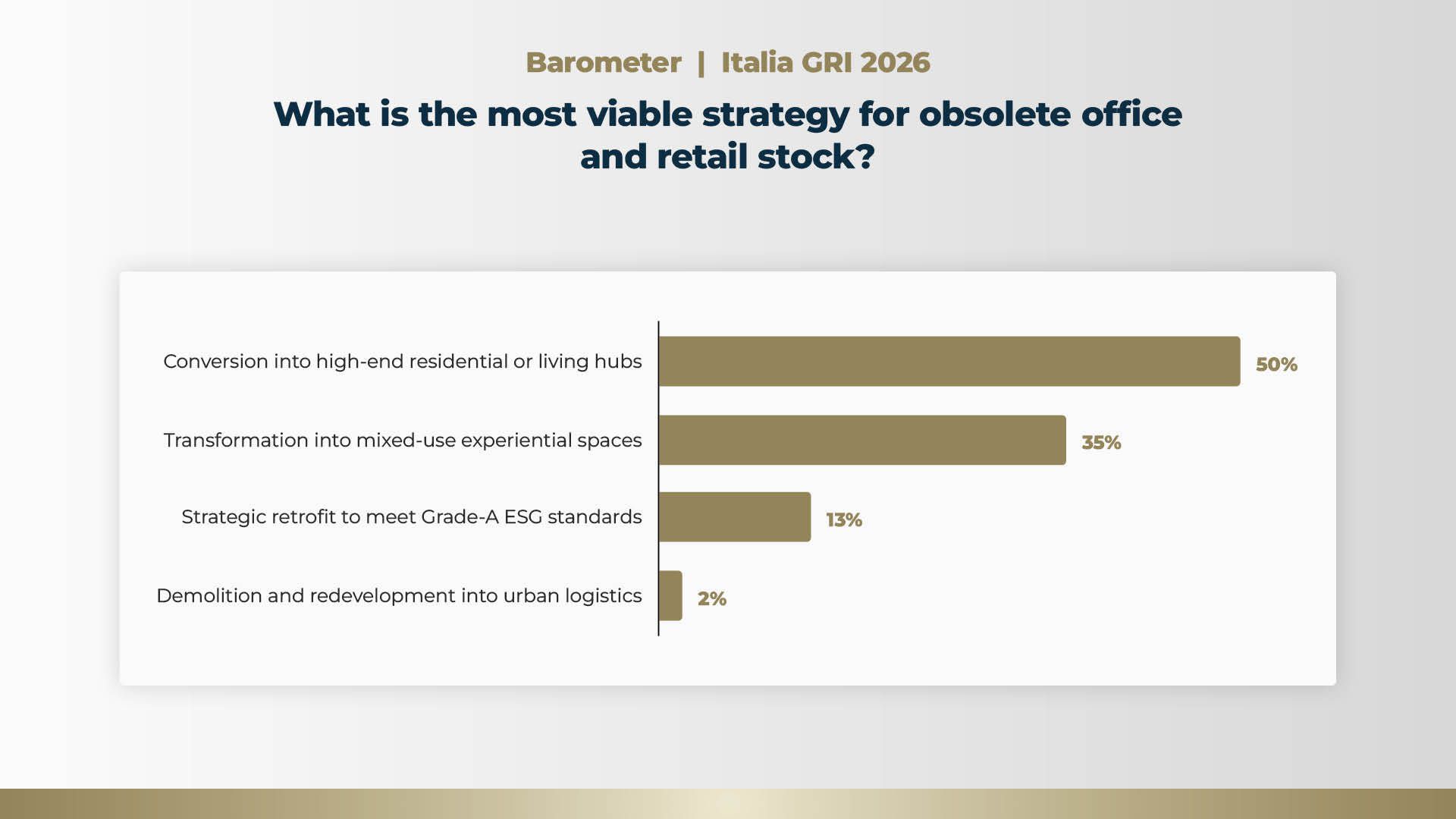

Most Viable Strategies for Obsolete Office and Retail Stock

Changing occupier preferences accelerate the structural obsolescence of legacy commercial buildings. Exactly half of all surveyed industry leaders state that the single most viable strategy for obsolete office and retail stock is full conversion into high-end residential spaces or urban living hubs.

The traditional routes of asset preservation and commercial repositioning show minimal viability according to the survey sample. Strategic retrofitting to meet Grade-A ESG standards garnered only 13% of executive support, while demolition and redevelopment into urban logistics platforms sat at the absolute bottom with a mere 2% of the vote.

This strong preference for adaptive reuse highlights a market-wide consensus that obsolete commercial space must be aggressively repurposed into alternative living structures to help bridge Italy's massive national deficit of 600,000 homes.

While prime Central Business District offices in Milan maintain an exceptionally tight 2% vacancy rate, older commercial assets in peripheral or secondary locations are suffering from a severe lack of institutional liquidity.

To unlock these frozen portfolios, developers are actively leveraging public asset valorisation programmes and turning to technology-driven, staff-light flex-living models. This allows them to bypass urban saturation, generate inflation-linked cash flows, and effectively match real estate functionality with modern corporate and social demand.

A Blueprint for Institutional Modernisation

Ultimately, these results signal a profound structural pivot away from passive, yield-relying real estate models toward highly proactive, operationally intensive investment strategies.The strong consensus on mid-cycle expansion, paired with an aggressive push for commercial-to-residential conversions, demonstrates that forward-looking capital is directly targeting Italy's acute public infrastructure and housing deficits.

Furthermore, the prominent financing gaps highlight that future market winners will be those who can successfully bridge the cultural mismatch between traditional local sponsorship and the disciplined asset-management requirements of modern private debt.

As the peninsula transitions toward institutional maturity, value creation will increasingly belong to sophisticated players capable of deploying technology-driven, staff-light platforms that transform obsolete, fragmented bricks and mortar into liquid, scalable living and hospitality ecosystems.