Unsplash

UnsplashSpain, Portugal, Italy, or France? Navigating the Southern European residential landscape

Exclusive GRI Barometer insights into how industry leaders are addressing radical shifts in investment playbooks, market sentiment, and sector resilience

May 21, 2026Real Estate

Written by:Rory Hickman

Executive Summary

The landscape for Southern European living assets is at a critical inflection point. As the industry grapples with extreme construction costs, fragmented regulations, and a pervasive housing affordability crisis, senior real estate leaders are radically rethinking their investment playbooks.

This exclusive survey from GRI Living Assets Southern Europe 2026 reveals a surprising shift in capital flows and strategic priorities, including which markets offer the most attractive risk-adjusted returns, why long-standing residential models are facing unprecedented friction, and how operators are repositioning their portfolios to secure resilience and growth through 2027.

► Read the full GRI Living Assets Southern Europe 2026 Spotlight report here

This exclusive survey from GRI Living Assets Southern Europe 2026 reveals a surprising shift in capital flows and strategic priorities, including which markets offer the most attractive risk-adjusted returns, why long-standing residential models are facing unprecedented friction, and how operators are repositioning their portfolios to secure resilience and growth through 2027.

► Read the full GRI Living Assets Southern Europe 2026 Spotlight report here

Key Takeaways

- Investors are increasingly favouring specific Southern European markets that offer stronger risk-adjusted returns and more resilient growth prospects.

- Real estate strategies are shifting towards sales-led models and refurbishments to navigate high construction costs and complex regulatory landscapes.

- Future success depends on adopting industrialised construction methods and technology-driven management to improve efficiency and address the housing affordability crisis.

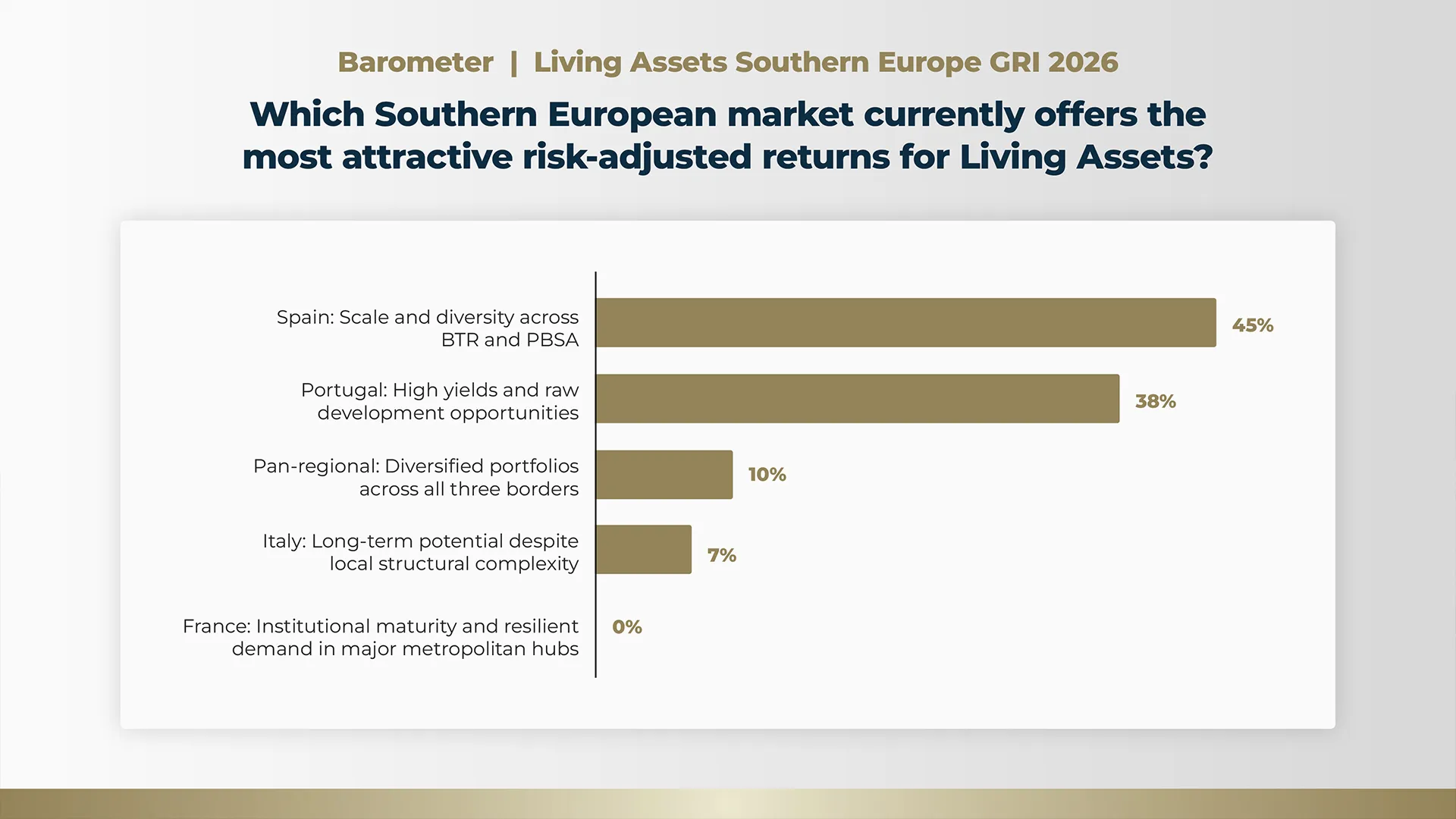

Top Southern European Markets

Spain clearly dominates investor sentiment within the region, securing 45% of the vote as the Southern European market that offers the most attractive risk-adjusted returns.

Spain's appeal is underpinned by strong market fundamentals, positive immigration, and healthy household formation, with the country offering significant scale and diversity across critical sub-sectors - including build-to-rent (BTR) and purpose-built student accommodation (PBSA).

This strong demand continues to attract capital despite ongoing challenges with regional regulatory inconsistencies and rising construction costs.

Portugal follows closely at 38%, positioned as an attractive safe haven for capital seeking high yields and raw development opportunities. Investors are drawn to the market by incoming structural shifts, such as the expected reduction of VAT on construction hard costs from 23% to 6% - which could significantly unlock mid-market developments on the outskirts of major cities.

Conversely, Italy captured only 7% of the vote. While it holds substantial long-term potential, the market remains less institutionalised and presents high execution hurdles due to local structural complexities.

A notable 10% of respondents favour a pan-regional approach, seeking to mitigate individual market risks by establishing diversified portfolios across multiple borders.

Interestingly, France received no votes for offering the most attractive risk-adjusted returns. Although the French market benefits from institutional maturity and resilient demand in major metropolitan hubs, it is currently navigating political and interest-rate pressures that make the peripheric advantages of Spain and Portugal more appealing for opportunistic capital.

Ultimately, while Southern Europe is increasingly viewed as the real estate engine of the continent, successfully capitalising on these returns requires deep local expertise and cross-border partnerships to overcome fragmented rules, language barriers, and lengthy licensing processes.

Residential Strategies

Given the challenging regulatory landscape and extreme construction costs across Southern Europe, 55% of investors favour a build-to-sell (BTS) strategy to capture immediate liquidity and high demand.

As highlighted during the panels, this preference is heavily driven by the current difficulties facing the BTR model, which received a mere 3% of the vote for building long-term institutional platforms.

In markets such as Spain, large BTR portfolios are increasingly pivoting toward "privatisation" - selling units individually as tenants depart - to maximise gains in a supply-constrained environment.

Similarly, BTR in Portugal remains nearly non-existent due to frozen rent legacies and a lack of regulatory incentives, prompting a reliance on domestic buyers purchasing off-plan as a form of capital preservation.

Value-add refurbishments of existing stock in urban centres emerged as the second most attractive strategy, securing 28% of the consensus. With lengthy permitting processes often taking up to five years for small projects, repurposing existing buildings provides a more agile and predictable route to market.

The conversion of underperforming or obsolete office stock into residential units is proving to be a critical strategy for core funds seeking stabilised income, allowing developers to bypass some of the zoning delays and high land prices associated with ground-up construction in prime metropolitan areas.

Finally, 14% of respondents see the best risk-adjusted outlook in affordable housing delivered through public-private partnerships (PPPs) as unaffordability remains a pervasive crisis across the Mediterranean.

While institutional investment in this space is sometimes hindered by reputational risks and regulatory uncertainty, overcoming the supply-demand imbalance requires patient capital, government subsidies, and collaborative innovation.

Solutions being explored include high-productivity industrialised construction, modular components, and the repurposing of infrastructure land to deliver viable, cost-effective housing near key transport hubs.

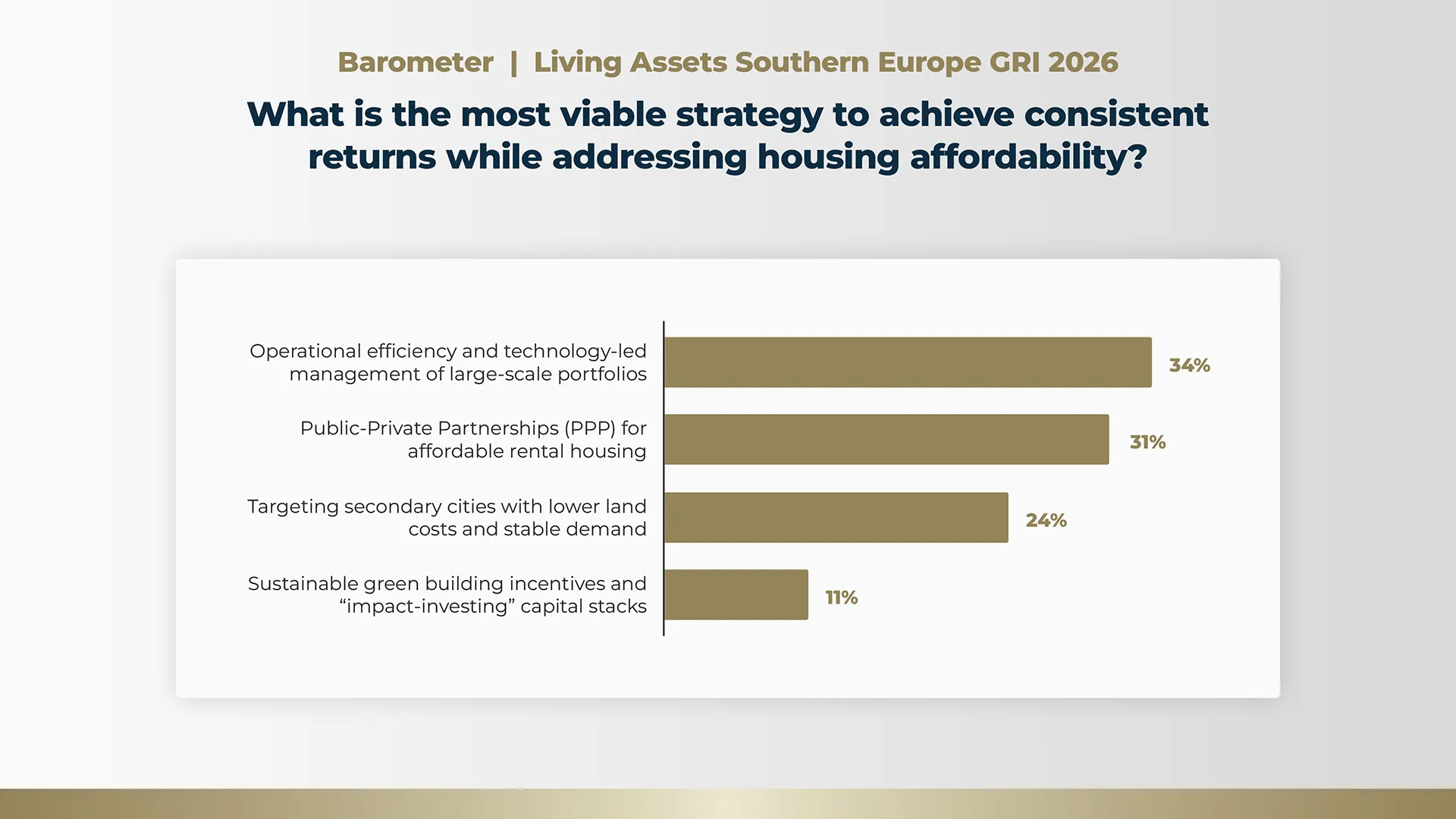

Affordability vs Returns

Addressing the pervasive European housing affordability crisis requires innovative approaches to maintain viable margins, with 34% of survey respondents identifying operational efficiency and technology-led management of large-scale portfolios as the most effective strategy.

The industry must shift from traditional construction to a high-productivity "house production" model, mirroring the automotive sector.

To control extreme construction costs and mitigate the risks of volatile global material supplies, developers are increasingly internalising architecture, adopting AI, and utilising industrialised components to keep operations lean.

PPPs for affordable rental housing followed closely at 31% as overcoming massive regional shortages - such as the deficit of 700,000 units in Spain - demands a collaborative framework that combines patient capital, government subsidies, and regulatory stability.

Proposed solutions to unlock supply include European-level risk-weighted asset adjustments for banks, and the repurposing of obsolete infrastructure land for residential use near key transport hubs.

In third place, 24% of leaders see value in targeting secondary cities, leveraging lower land costs to offset the structural hurdles of delivering mid-market housing.

While these areas can occasionally face liquidity concerns from core capital, strategic investments in surface metros and rail links are proving essential to unlocking the outskirts of major metropolitan areas.

Meanwhile, a niche 11% of respondents look to sustainable green building incentives and "impact-investing" capital stacks, relying on the use of sustainable materials, such as timber, to navigate the difficult underwriting of affordable housing.

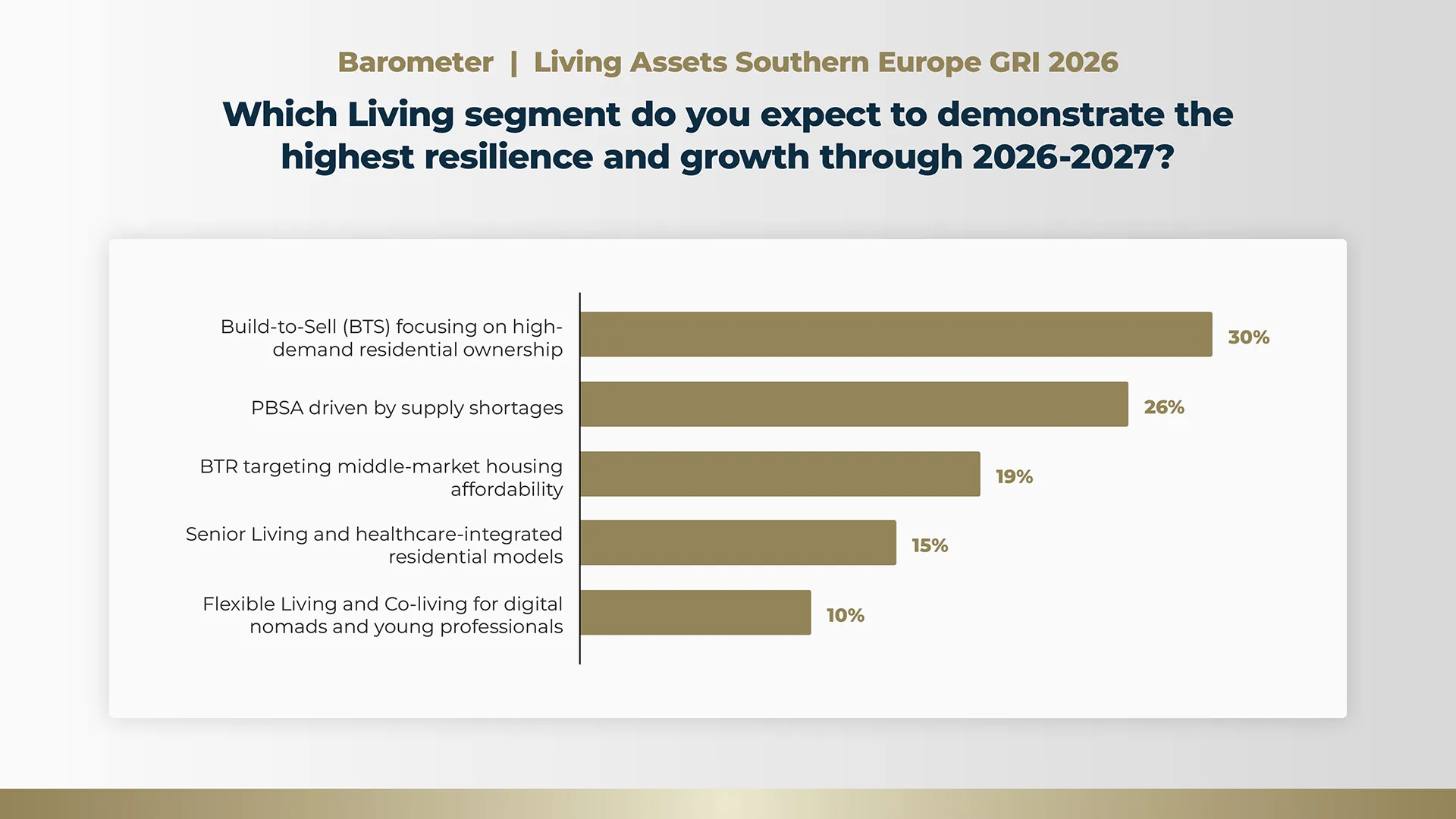

Sector Resilience

Looking ahead to 2027, BTS stands out as the segment expected to demonstrate the highest resilience and growth, securing 30% of the survey responses.

Panel discussions confirmed that developers are increasingly repositioning their pipelines away from strictly premium products toward highly diversified, "value for money" solutions that align with the constrained purchasing power of the middle class.

Closely following is PBSA at 26%, a sector primarily driven by acute supply shortages in key university towns. Iberia remains a core jurisdiction for pan-European strategies, with Spain's modest 9-10% provision rate indicating a significant runway for institutional growth.

Operators in this space are also actively seeking "double licences" to permit high-occupancy hotel use during summer academic gaps, thereby optimising net operating income.

BTR targeting middle-market housing affordability captured 19% of the consensus, reflecting the industry's ongoing efforts to navigate the pervasive European affordability crisis and structural supply shortages through legislative incentives and professionalised management.

Meanwhile, senior living models garnered 15% of expectations. The sector is rapidly evolving from a purely medicalised nursing home model into a lifestyle-driven longevity market, buoyed by deep demographic shifts and an influx of "nomadic" seniors from Northern Europe.

However, despite potentially high revenues, investors remain cautious due to a highly fragmented operator landscape and a lack of established market comparables for financing risk committees.

In last place, flexible living and co-living formats, aimed at digital nomads and young professionals, accounted for 10% of the vote. Proven to be a highly resilient model over the past six years, flex-living crucially fills the gap between permanent housing and temporary labour mobility.

Operators are maintaining lean operations and high margins through the strategic use of internal technology, offering an attractive, amenity-rich lifestyle product that typically caters to stays of nine to twelve months.

By seamlessly pivoting between short-term and mid-term stays, these assets are well-equipped to navigate seasonal demand and broader economic shocks.

Southern Europe's Operational Future

These results signal a profound evolution in the Southern European living sector. The era of passive, yield-chasing capital is giving way to a demand for extreme operational agility.Investors are clearly prioritising pragmatic, liquidity-driven strategies to navigate an environment constrained by regulatory bottlenecks, inflated construction costs, and a mounting affordability crisis.

Going forward, success will no longer be defined merely by acquiring land and building assets, but by operating highly efficient, tech-enabled platforms.

Solving the region's deep supply-demand imbalance dictates that the industry must evolve from a purely private enterprise into an active, industrialised partner with the public sector to deliver genuine value for the middle class.

► Read the full GRI Living Assets Southern Europe 2026 Spotlight report here

This survey was conducted among the senior real estate industry leaders in attendance at GRI Living Assets Southern Europe 2026.

For further insights into the pan-European living sector, don’t miss GRI Living Assets Europe 2026 in London on 24th-25th June.