GRI Institute

GRI InstituteThe Iberian Safe Haven: Why global institutional capital is pivoting to Spanish real estate

Collected insights from industry decision-makers on why the peninsula's BTR, PBSA, and luxury hospitality sectors outperform core Northern European markets

June 10, 2026Real Estate

Written by:Henrique Cisman

Executive Summary

Spain's real estate market has firmly established itself as a premier defensive safe haven for global institutional capital, presenting a compelling investment case that stands out against broader European stagnation.

Driven by resilient tourism, a growing population, and acute housing shortages, the Iberian Peninsula continues to command strong conviction from international investors looking for scalable opportunities and reliable risk-adjusted returns.

This momentum and the shifting dynamics of the market were central to the insights shared at the España GRI 2026 gathering in Madrid, where top real estate leaders deconstructed the local landscape.

What emerges from the discussion is a sector undergoing structural evolution, characterised by the rapid professionalisation of alternative debt funds, a definitive flight to quality, and an overwhelming preference for Spanish living assets over traditional continental markets.

Ahead of the GRI Living Assets Europe 2026 conference in London, which will serve as a vital venue to continue the conversation, we take a look at the data, capital shifts, and financing trends defining the Spanish real estate ecosystem today.

Driven by resilient tourism, a growing population, and acute housing shortages, the Iberian Peninsula continues to command strong conviction from international investors looking for scalable opportunities and reliable risk-adjusted returns.

This momentum and the shifting dynamics of the market were central to the insights shared at the España GRI 2026 gathering in Madrid, where top real estate leaders deconstructed the local landscape.

What emerges from the discussion is a sector undergoing structural evolution, characterised by the rapid professionalisation of alternative debt funds, a definitive flight to quality, and an overwhelming preference for Spanish living assets over traditional continental markets.

Ahead of the GRI Living Assets Europe 2026 conference in London, which will serve as a vital venue to continue the conversation, we take a look at the data, capital shifts, and financing trends defining the Spanish real estate ecosystem today.

Key Takeaways

- Spain has firmly transitioned from a cyclical recovery market into a mature, permanent cornerstone for pan-European capital strategies, offering global institutional investors a highly resilient, defensive safe haven backed by robust demographic tailwinds and strong GDP growth.

- The rapid professionalisation and expanding dominance of alternative lenders are structurally shifting the capital stack, providing critical debt liquidity for value-creation and greenfield projects while traditional banks slowly return to higher LTV lending.

- High conviction in Southern Europe is concentrated heavily in Spain and Portugal, where immense scalability across BTR and PBSA platforms, combined with resilient tourism performance, continues to outperform core Northern European markets.

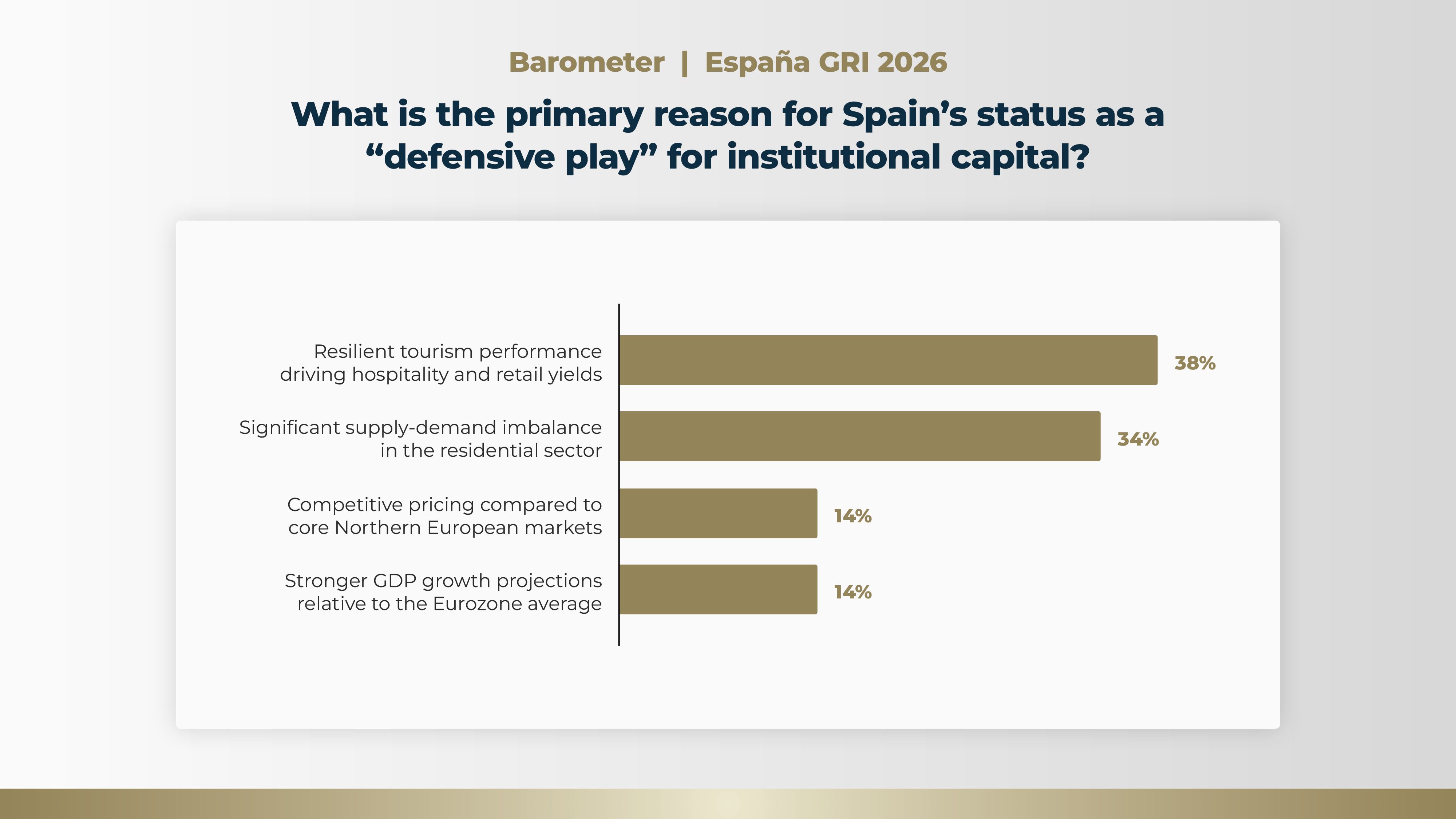

Spain as a "Defensive Play"

The España GRI 2026 survey highlights a strong consensus among senior real estate industry leaders regarding Spain's emerging status as a reliable defensive haven for institutional capital.

According to the executives, the leading factor driving this sentiment is the country's resilient tourism performance, which continues to bolster hospitality and retail yields, capturing 38% of the votes. This is closely followed by the significant supply-demand imbalance in the residential sector, which 34% of respondents identified as the primary catalyst for defensive investment.

The remaining sentiment is equally split between macroeconomic and pricing advantages. Specifically, 14% of surveyed leaders point to Spain's stronger GDP growth projections relative to the Eurozone average as the main driver, while another 14% emphasize its competitive asset pricing when contrasted with core Northern European markets.

This balanced distribution underscores the multi-faceted appeal of the Iberian market, combining macroeconomic resilience with strong sector-specific fundamentals. While traditional European investment hubs grapple with stagnation, Spain's macroeconomy is supported by a growing population and GDP growth exceeding 2%.

The high conviction in hospitality is reflected in the market's pivot toward luxury developments capable of commanding exceptional average daily rates, while the acute housing undersupply ensures long-term institutional interest in residential platforms despite local regulatory hurdles.

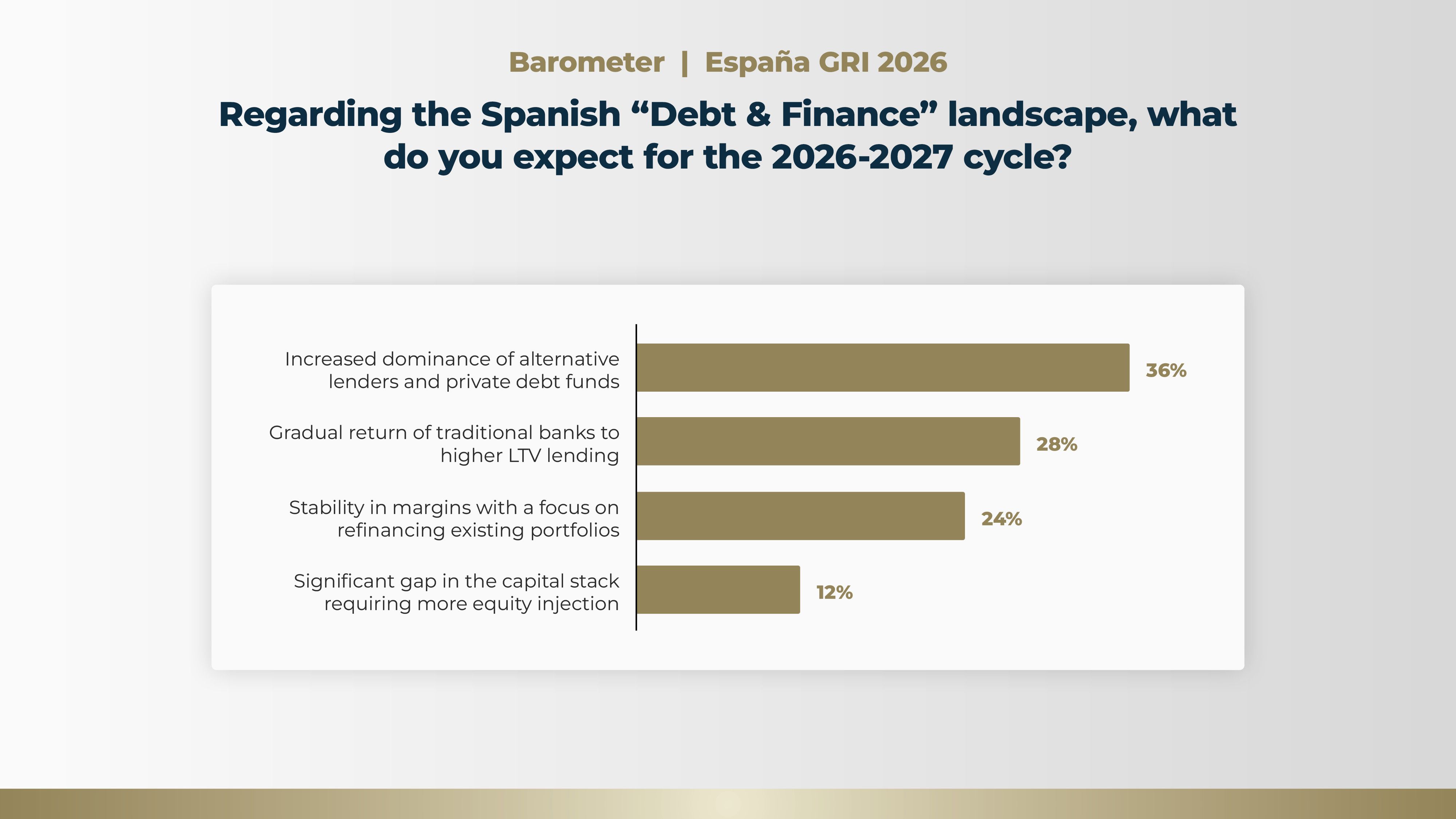

Evolution of the Spanish Debt and Finance Landscape

When surveyed on their expectations for the 2026-2027 financing cycle, real estate executives pointed toward a structurally shifting capital stack. The largest share of respondents (36%) anticipates an increased dominance of alternative lenders and private debt funds. This perspective reflects a market that is rapidly professionalising to meet the demands of sponsors navigating complex asset classes.Meanwhile, 28% of leaders foresee a gradual return of traditional banks to higher loan-to-value (LTV) lending, indicating that conventional credit lines are expected to reopen slowly as market conditions stabilise.

Portfolio management and capital conservation also feature heavily in the near-term outlook. Nearly a quarter of those surveyed (24%) expect stability in margins with a primary focus on refinancing existing portfolios, rather than funding new acquisitions.

Conversely, only 12% of executives believe there will be a significant gap in the capital stack that requires a greater injection of equity, suggesting a general confidence in the availability of debt liquidity, irrespective of its origin.

Traditional banks remain highly selective, forcing non-bank capital to step into value-creation and greenfield development phases. With refinancing emerging as a dominant exit strategy and international debt providers introducing highly competitive back-leverage structures, alternative debt funds are successfully positioning themselves as an indispensable, permanent component of the Iberian real estate ecosystem.

Regional Attractiveness for Living Assets in Spain

The investment appetite for residential and alternative residential sectors shows a clear concentration of capital within specific corners of the Iberian Peninsula. Spain is considered the most attractive Southern European market for risk-adjusted returns in Living Assets, securing 45% of the vote.

Surveyed executives attribute this top ranking to the superior scale and diversity available across the Spanish build-to-rent (BTR) and purpose-built student accommodation (PBSA) segments.

Global capital from North America, the Middle East, and Asia is actively reallocating toward Southern Europe. Driven by shrinking household sizes and strict equity requirements that price out first-time homebuyers, the Spanish BTR market remains highly lucrative.

Even as institutional investors demand higher yields, the sheer scalability of the Iberian living sectors continues to outperform other continental markets.

A Strategic Blueprint for Pan-European Capital

Ultimately, these findings signal a profound maturation of the Iberian market, transitioning it from a cyclical recovery play into a permanent cornerstone of pan-European capital strategies. The strong focus on resilient tourism, non-bank financing, and scalable living assets demonstrates that success no longer hinges on mere yield compression, but on operational excellence and flexible capitalization.By successfully professionalising its private debt ecosystem to counter selective bank lending, Spain has effectively insulated itself from broader continental stagnation.

Moving forward, the region stands as a blueprint for navigating macroeconomic tension-proving that structural supply deficits and robust demographic tailwinds can create a highly predictable, sophisticated safe haven for global capital.