GRI Institute

GRI InstituteThe Data Centre Super-Cycle: Why the global future of AI is being built in India

Capital scale and strategic consolidation are positioning the subcontinent as the definitive APAC hub for sovereign cloud and high density AI infrastructure

February 24, 2026Real Estate

Written by:Jorge Aguinaga

Executive Summary

The Indian data centre sector has reached a structural inflection point, transitioning from a domestic service model to a global strategic hub within the Asia-Pacific corridor. Driven by an infrastructure super-cycle and unprecedented AI demand, the market is scaling from 1.3 GW of operational capacity toward 1.7 GW well before 2027.

The GRI Data Centre India 2026 conference convened industry authorities to interrogate these dynamics, highlighting how new safe harbour provisions and tax holidays have mitigated investor uncertainty. With 75% of pipelines shifting to liquid cooling to support densities potentially reaching 1 MW per rack, this report synthesises critical insights on power resiliency, modular delivery, and the mandate for Sovereign AI.

The GRI Data Centre India 2026 conference convened industry authorities to interrogate these dynamics, highlighting how new safe harbour provisions and tax holidays have mitigated investor uncertainty. With 75% of pipelines shifting to liquid cooling to support densities potentially reaching 1 MW per rack, this report synthesises critical insights on power resiliency, modular delivery, and the mandate for Sovereign AI.

Key Takeaways

- India’s expansion necessitates approximately USD 5 billion in annual investment to support a one-gigawatt-per-year growth target, attracting significant global financial sponsors.

- To support AI workloads, the industry is shifting from legacy 3-6 kW densities toward high-performance environments utilising liquid cooling and 800 VDC power architectures.

- A multi-parameter strategy has emerged where power-intensive AI training migrates to resource-rich regions like Rajasthan, while latency-sensitive inference remains in metropolitan hubs.

Capital, Scale & Consolidation: The new economics of digital infrastructure growth

India Digital Infrastructure Strategic Blueprint

The Indian data centre sector is currently defined by an aggressive expansion phase, evolving from a local service provider into a globally significant strategic hub. This evolution is marked by a record delivery of nearly 450 MW in 2026, driven by an infrastructure super-cycle fuelled by global AI demand.With operational capacity scaling from 1.3 GW toward a projected 1.7 GW well before 2027, the market is successfully positioning itself to capture the broader Asia-Pacific (APAC) demand traditionally held by established hubs such as Singapore.

The AI Infrastructure Imperative

A radical redesign of data centre specifications is underway to accommodate the unprecedented requirements of artificial intelligence.Legacy 3-6 kW racks are being replaced by high-density environments exceeding 30-40 kW for current GPU clusters, with projections for late 2027 suggesting densities may reach 1 MW per rack for advanced processors such as Nvidia’s Rubin Ultra Plus.

Consequently, 75% of new asset pipelines have transitioned to liquid cooling formats to manage these extreme thermal loads. This technical evolution is driving a future-proofing mandate, ensuring that infrastructure built today remains relevant for the next 15-20 years despite chip technology cycles shrinking to as little as six months.

Economic Fundamentals and Global Positioning

India’s competitiveness is underpinned by a robust regulatory framework and favourable financial metrics. New safe harbour provisions, which assume a flat 15% margin on costs for related-party transactions, have mitigated the tax uncertainty that previously deterred multinational investment.Furthermore, a 20-year tax holiday until 2047 for foreign cloud operators serving offshore demand through dollar-denominated billing - recently introduced in the Union Budget 2026 - are successfully attracting global workloads to Indian soil.

Investment returns remain attractive, with industry standards suggesting an unlevered IRR of 14-15% for speculative builds and 17-18% for built-to-suit projects.

Operational Realities: Power and Execution

Despite the abundance of capital and demand, the sector still faces structural bottlenecks that require urgent strategic intervention. Power has replaced land as the primary global constraint, with the transition to 1 GW single-site campuses demanding a fundamental rethink of energy procurement.- Location Strategy Bifurcation: AI training workloads, which are power-intensive but latency-insensitive, are migrating toward remote, resource-rich regions such as Rajasthan, while inference workloads remain close to metro hubs to satisfy low-latency requirements for real-time applications.

- Energy Resilience: Current solar implementations effectively provide only 7-8 hours of daily power, highlighting the critical need for Battery Energy Storage Systems (BESS) and Data Centre Parks co-located with renewable hubs to ensure 24/7 operational continuity.

- Execution Roadblocks: Acute shortages of skilled labour and long lead times for critical equipment remain significant hurdles, with transformer lead times currently standing at approximately 24 months.

Strategic Outlook

As the market consolidates into a core group of approximately 12-13 dominant players, success will be determined by the ability to master technical complexity while securing long-term renewable baseload power.The future of the sector lies in becoming strategic infrastructure partners, providing integrated energy and compute solutions that support the rising mandate for Sovereign AI.

Preeminent leaders gathered at the Grand Hyatt Mumbai for GRI Data Centre India 2026 to interrogate the infrastructure super-cycle driving India’s transition into a global strategic hub. (GRI Institute)

Digital Demand & Enterprise Shifts: Mapping the next wave of occupier needs

Market Maturation and Resilience

While there is significant momentum surrounding the rise of artificial intelligence and hyperscale requirements, this is tempered by the technical and operational complexities of new technologies.Industry veterans are currently managing a steep learning curve regarding both developments in liquid cooling and the potential implications of integrating quantum computing.

Despite these pressures, there is strong underlying confidence in the long-term demand profile, particularly within the Indian market, which is evolving into a diverse ecosystem capable of sustaining both global giants and agile domestic players.

Escalating Capacity Requirements

A primary shift in the landscape is the dramatic scaling of enterprise requirements. Over the last 36 months, typical enterprise deal sizes have surged from small kilowatt allocations to substantial blocks ranging between 2 megawatts and 25 megawatts.This growth is largely propelled by rigorous regulatory pressure in India, where authorities are mandating higher resiliency and Tier IV standards for national infrastructure, such as banking and exchanges. Simultaneously, the nature of AI demand is pivoting from foundational model training toward production-side inferencing.

Inferencing is projected to eventually account for half of all compute requirements, a shift that benefits markets like India due to the necessity for low latency and adherence to data sovereignty norms.

Furthermore, the emergence of neocloud providers is creating a new customer category, allowing AI labs to enter the market without the overhead of direct infrastructure management.

Evolving Site Selection

The physical architecture of the sector is undergoing a fundamental transformation as power availability becomes the primary global bottleneck. Site selection is no longer a binary choice based on proximity to cable landing stations.Instead, a multi-parameter reality has emerged where land, infrastructure, and reliable electricity are weighted according to specific use cases, leading to the rise of power-led compute hubs in non-traditional or solar-rich regions.

Operational and Grid Constraints

The most significant hurdle is the widening gap between ambitious capacity announcements and practical on-the-ground delivery.Securing permits, ensuring last-mile power connectivity, and managing the vast investment required for transmission infrastructure remain formidable obstacles. The grid itself could become a choking point unless there is a proactive approach to producing and transmitting power more intelligently.

Technological obsolescence also presents a constant risk. While the industry is currently maturing its understanding of liquid cooling, it must already prepare for the different infrastructure needs of quantum chips, which may require cryogenic environments within just a few years.

This rapid pace of change creates a risk that facilities designed today might be misaligned with the hardware they must host by the time they are commissioned. Additionally, the market is currently overcrowded with players driven by short-term private equity horizons rather than long-term delivery, leading to concerns about future consolidation and ROI pressure.

Strategic Infrastructure Partnerships

To navigate this volatility, operators must transition from being simple landlords to acting as strategic infrastructure partners. This involves developing deep engineering, procurement, and construction capabilities to manage power and water resources while effectively engaging with local communities to ensure the long-term acceptance of large-scale projects.There is also a clear mandate for geographical and technological diversification. While hyperscale demand in major metros remains dominant, edge data centres will eventually become essential for delivering data logistics to Tier 2 and Tier 3 cities, particularly as AI inferencing requires processing capacity to sit closer to the end-user.

Furthermore, there is a strategic focus on future-ready solutions - such as two-phase immersion cooling and sovereign cloud architectures - to protect against shifting geopolitical and regulatory frameworks.

The industry’s most influential voices agreed that the mandate for Sovereign AI and the adoption of high-density liquid cooling are now the primary catalysts for the next decade of digital growth. (GRI Institute)

Design, Technology & Operational Evolution: Reimagining Efficiency, Density & Performance

Engineering for AI and High Density Loads

The data centre landscape is currently transitioning from legacy densities of 3-6 kW per rack toward configurations of 12-15 kW, with immediate requirements scaling to 25-30 kW.Future projections indicate the arrival of chips consuming up to 600 kW per rack by 2027, eventually reaching 1 MW per rack for specialised applications.

Meeting these demands requires a transition toward liquid cooling and 800 VDC power architectures, where power is drawn directly from the grid to rectifiers to eliminate the inefficiencies of traditional AC to DC conversion cycles.

This evolution has already influenced density per acre, with current designs targeting over 20 MW per acre compared to the previous standards of 8-10 MW.

Accelerating Speed to Market through Modularity

Annual capacity delivery in India has scaled from roughly 50 MW in 2019 to an anticipated 450 MW by 2026, positioning the market as a global hub capable of delivering 400-500 MW per year.To adhere to 15-month delivery timelines within constrained urban markets like Mumbai, there is an increasing shift toward modularity and Design for Manufacture and Assembly (DfMA).

These methodologies allow for factory-fabricated structures where 90% of Mechanical, Electrical, and Plumbing (MEP) work is completed off-site before being installed as pre-assembled skids.

Furthermore, localised manufacturing for Original Equipment Manufacturers (OEMs) has matured, allowing high-end cooling and power equipment to be manufactured domestically for export to the Middle East and APAC regions.

Sovereign AI and Infrastructure Mandates

The government’s INR 10,000 crore AI Mission is designed to subsidise the usage of AI infrastructure by 15% to 40%, fostering a market potential of approximately INR 40,000 crore over the next four years.This initiative drives the requirement for sovereign AI infrastructure, ensuring that data remains localised and that domestic models have access to necessary compute power.

While the power and cooling ecosystems are advancing, terrestrial network latency remains a challenge; latency from Chennai to Singapore can be lower than 7 milliseconds, whereas Chennai to Jammu can reach 35 milliseconds. Bridging this gap requires the proliferation of neutral, open-access fiber networks that are independent of specific telecom operators.

Operational Efficiency and Sustainability Benchmarks

Sustainability is now evaluated at a portfolio level, with water usage efficiency (WUE) becoming as critical as power usage effectiveness (PUE). High-density AI deployments necessitate robust management of grey water and wastewater treatment to support cooling operations without depleting local resources.Additionally, the adoption of renewable energy is moving beyond simple solar usage toward integrated battery storage systems to ensure reliability throughout 24-hour cycles.

Efficient waste management, specifically the organisation of e-waste recycling and the reuse of materials like racetracks and cables, is also becoming a standard requirement for institutional-grade facilities.

Human Capital and Delivery Certainty

The technical shift toward liquid cooling and specialised AI power architectures requires the upskilling of the local labour force to manage complex installations with minimal error.Success in this sector is tied to the predictability of the future data centre profile - whether it will be dominated by massive single-transformer racks for training or smaller, distributed chips for agentic AI.

Long-term business sustainability relies on the industry’s ability to meet aggressive contractual timelines despite global supply chain pressures, such as the 24-month lead times for transformers.

Capital remains attracted to the asset class due to its infrastructure-like cash flows, but project success is ultimately determined by delivery certainty and the ability to adapt to rapid hardware refreshes.

Strategic discussions between C-level executives highlighted that mastering the new economics of 1 GW campuses and 800 VDC power architectures will define the market's future leaders. (GRI Institute)

Power, Policy & Preparedness: Building energy-resilient data infrastructure for the next decade

Capital Mobilisation

The Indian data centre ecosystem is targeting a fourfold capacity increase over the next five to seven years, an ambition that requires unprecedented financial backing. To successfully add one gigawatt of operational capacity per year, the market necessitates a radical capital infusion of approximately USD 5 billion annually, laying the groundwork for the next era of digital infrastructure growth.Global financial sponsors, including major entities such as Blackstone, KKR, and Macquarie, are increasingly viewing India as a primary destination for digital infrastructure due to the scarcity of comparable facilities globally.

Strategic investment is no longer confined to the physical real estate of the data centre campus. Forward-thinking investors are now engaging in backward integration, allocating capital across the entire value chain - from GPUs and fibre networks to subsea cables and power generation.

Despite this enthusiasm, a significant speculative risk remains because the market is largely controlled by a few major hyperscalers who are simultaneously competing for self-use land and power resources.

Strategic AI Location

The distinction between AI training and AI inference is beginning to dictate divergent location strategies for future developments.Historically, data centres in India have been built close to demand centres within major metropolitan areas, whereas global trends - particularly in the United States - favour proximity to power resources in remote regions.

As the industry matures and the demand for high-density AI computing intensifies, a shift toward Tier 2 and Tier 3 cities is inevitable, as metropolitan grids will eventually struggle to justify the massive power and space requirements of these facilities.

The transition to decentralised or resource-proximate hubs is further supported by the evolution of workloads. While low-latency applications must remain near urban centres, AI training loads that are less sensitive to latency can be effectively moved closer to grid substations in high-resource states.

This movement mirrors the historical evolution of Global Capability Centres (GCCs), which took two decades to fully realise the cost and operational advantages of the Indian market.

Power Resiliency

The primary bottleneck for the next decade of infrastructure growth is the alignment of power availability with data centre demand. While India is a high-resource country, the current challenge lies in the lack of a streamlined regulatory process for interstate power transmission.Renewable energy generators often face significant delays in obtaining necessary approvals to supply power from remote solar or wind farms to urban data centre clusters.

To achieve world-class status, Indian data centres must move beyond vanilla renewable energy toward round-the-clock (RTC) power solutions.

Since solar and wind are intermittent, the integration of Battery Energy Storage Systems (BESS) or hybrid thermal-renewable packages is essential to ensure high reliability.

Currently, 60% to 70% of a facility’s power can be economically replaced by renewables, but reaching total energy residency requires sophisticated storage or backup to manage peak power demands.

Supply Chain Realities

India remains in a nascent stage regarding the domestic production of specialised data centre technology. A substantial portion of the cooling systems, power generation hardware, and design solutions currently utilised in Indian facilities is imported.There is a critical need for localised innovation in world-class cooling and high-efficiency power architectures to reduce the dependence on global supply chains. Execution remains the most significant roadblock to achieving the targeted development pace.

The industry is currently grappling with a shortage of skilled manpower specifically trained for critical infrastructure, as well as supply chain constraints on essential components like generators.

Furthermore, while state-level policies offer attractive tax breaks and single-window clearances, the practical implementation of these incentives often faces bureaucratic friction.

Market Sentiment and Strategic Forecasts

Quantifying industry consensus on capital structuring technical future-proofing and energy resiliency

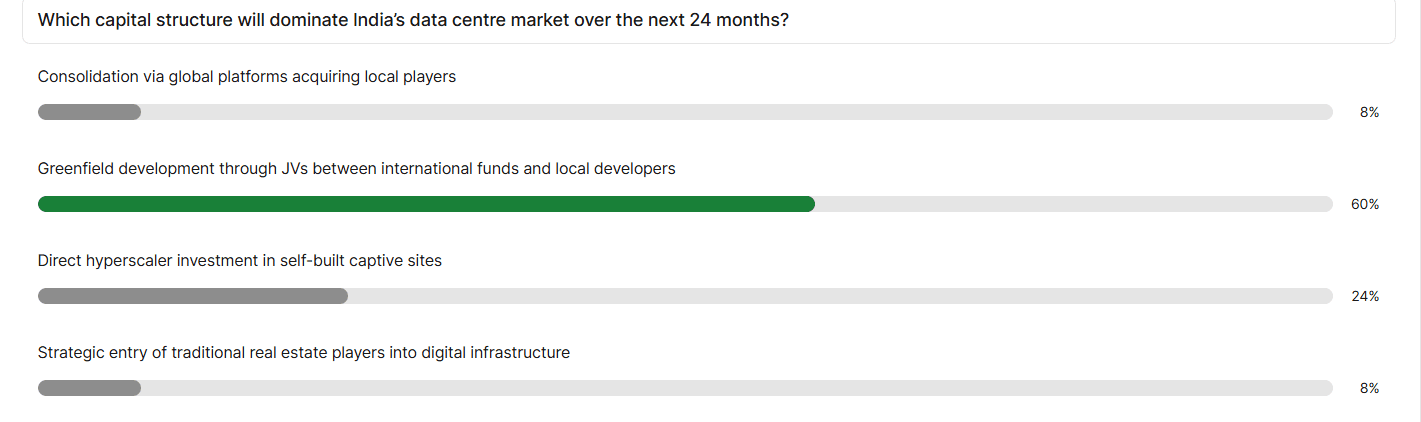

To quantify real-time strategic foresight, the GRI Institute conducted a market survey among C-suite executives, institutional investors, and digital infrastructure leaders actively deploying capital within the subcontinent.The resulting data paints a definitive picture of the capital landscape over the next 24 months, which is overwhelmingly leaning toward collaborative greenfield expansion. A significant 60% majority of these industry authorities anticipates joint ventures between international funds and local developers as the dominant market structure.

(GRI Institute)

(GRI Institute)This collaborative approach drastically outpaces direct hyperscaler investments in self-built captive sites, which represents just 24% of the strategic foresight.

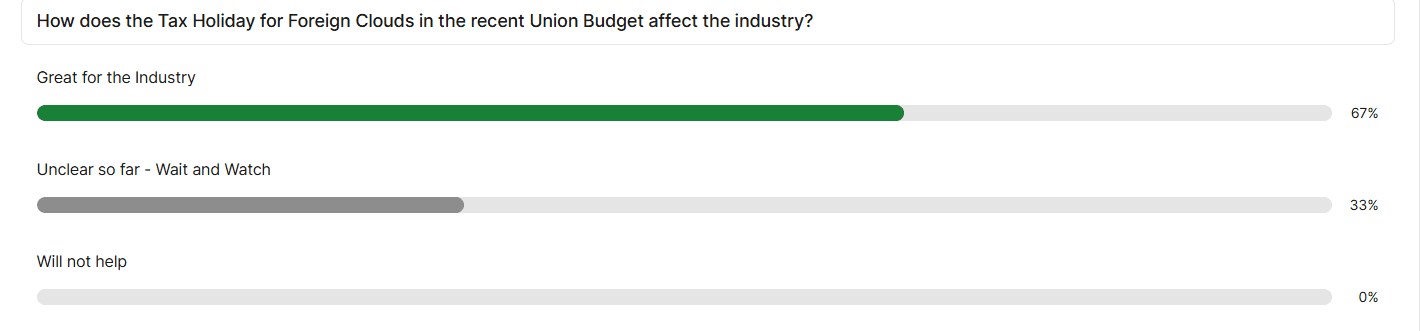

Furthermore, executive confidence in regulatory catalysts is remarkably high. Exactly 67% of market participants view the recent Union Budget tax holidays for foreign clouds as a major growth accelerator.

(GRI Institute)

There are zero dissenters claiming the policy will fail, though 33% maintain a cautious watch-and-wait posture regarding its long-term implementation.

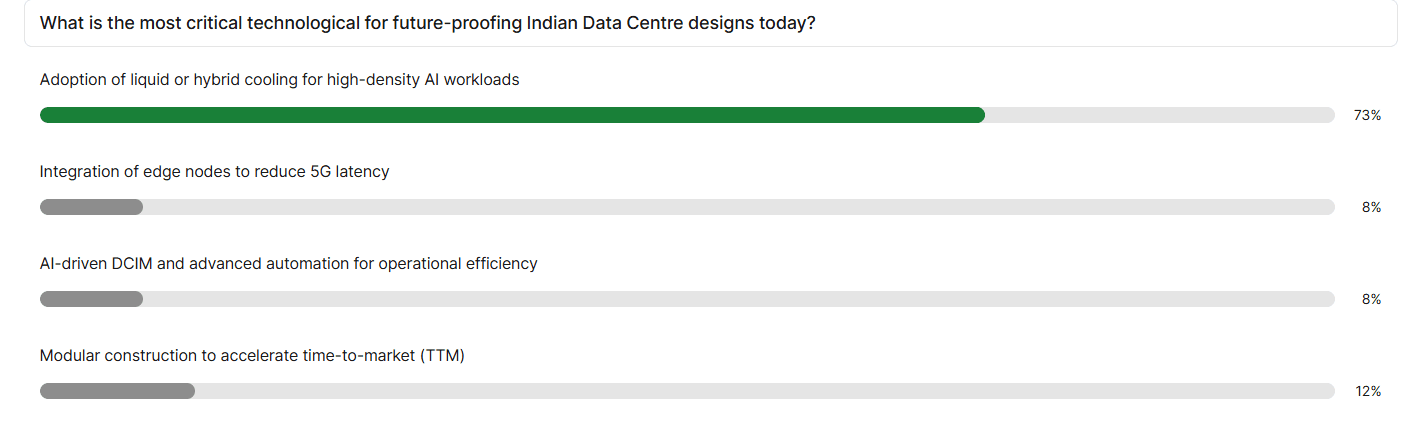

On the operational front, future-proofing strategies are strictly dictated by thermal management imperatives. A decisive 73% of surveyed leaders identify the adoption of liquid or hybrid cooling for high-density AI workloads as the absolute most critical technological priority.

(GRI Institute)

Architecting the APAC Digital Horizon

Ultimately, the Indian digital infrastructure market is navigating a profound maturation phase, actively transforming operational roadblocks into catalysts for innovation.While supply chain and execution hurdles persist, the convergence of deep capital pools, robust governmental support, and an aggressive pivot toward high density AI environments establishes an exceptionally strong foundation.

The industry is rapidly developing the engineering capabilities required to master liquid cooling and gigawatt scale campuses, ensuring structural readiness for the next super-cycle of global demand.

As operators evolve into comprehensive infrastructure partners, the subcontinent is uniquely positioned to lead the broader APAC region. With an unrivalled concentration of technological talent, abundant renewable energy potential, and the necessary financial backing, the market possesses all requisite components to meet the sovereign AI mandate.

The long term trajectory remains overwhelmingly positive, promising resilient, institutional grade growth that will definitively shape the global future of data centres.

Thank you to everyone who participated in the GRI Data Centre India 2026 forum. Look out for more discussions on these issues at our upcoming gatherings.