GRI Institute

GRI InstituteHow is a deeply polarised market redefining Portugal’s next investment cycle?

Senior insights from GRI Women Leading Portuguese Real Estate on the structural trends, regulatory overhauls, and emerging assets shaping the market in H2 2026

July 7, 2026Real Estate

Written by:Rory Hickman

Executive Summary

Portugal’s real estate market is navigating a profound structural divergence, characterised by resilient international investment in luxury assets alongside an acute domestic housing shortage. This polarisation is driving a fundamental shift towards operational agility, accelerated by sweeping regulatory overhauls aimed at stripping away bureaucratic friction.

This tension defined discussions among top industry leaders at the GRI Women Leading Portuguese Real Estate 2026 roundtable in Lisbon, held as part of Portugal GRI 2026. The picture emerging is one of tactical adaptation, where future growth relies on solving for supply gaps, executing asset conversions, and unlocking alternative sectors.

Ahead of further regional discussions during the upcoming Europe GRI 2026 - Summer Edition in Paris on 9th-10th September, these insights outline the strategic mindset shaping the Portugal’s next investment cycle.

► The full Portugal GRI 2026 Spotlight report is available here

This tension defined discussions among top industry leaders at the GRI Women Leading Portuguese Real Estate 2026 roundtable in Lisbon, held as part of Portugal GRI 2026. The picture emerging is one of tactical adaptation, where future growth relies on solving for supply gaps, executing asset conversions, and unlocking alternative sectors.

Ahead of further regional discussions during the upcoming Europe GRI 2026 - Summer Edition in Paris on 9th-10th September, these insights outline the strategic mindset shaping the Portugal’s next investment cycle.

► The full Portugal GRI 2026 Spotlight report is available here

Key Takeaways

- A severe structural polarisation is splitting the market, with resilient foreign capital targeting luxury developments while the domestic middle class faces a chronic housing shortage.

- The "Simplex" regulatory reforms have unlocked the development pipeline by eliminating bureaucratic licensing delays in exchange for total developer accountability.

- Changing generational and expat demographics are accelerating the growth of alternative sectors, particularly transit-oriented build-to-rent, co-living, and independent senior housing.

► Portuguese Real Estate Market Evolution

Despite persistent global macroeconomic uncertainties, the Portuguese real estate market continues to exhibit remarkable resilience, consistently attracting both domestic and foreign institutional investment.The market is underpinned by robust fundamentals including a stable economy, a flourishing tourism ecosystem, and sustained cross-sector demand.

Beyond its established appeal as an investment destination, Portugal has increasingly positioned itself as a primary choice for global citizens seeking to live, work, and establish long-term operations.

(GRI Institute)

► The Luxury and High-End Residential Landscape

The high-end residential sector in Portugal is currently characterising itself through intense demand matched against a chronic under-supply of premium inventory. This supply-demand imbalance has turned prime locations into highly competitive arenas often described as a structural war for premium land parcels.The geographical focus remains heavily concentrated in core urban zones and exclusive coastal enclaves, notably Lisbon, Porto, and specific micro-locations within Cascais and Estoril.

A significant challenge in the current market is the inflation of the "high-end" label. While a proliferation of projects claims luxury status, true market differentiation relies strictly on three immutable pillars:

- Flawless micro-locations

- Exceptional construction quality

- Authentic lifestyle integration

When compared to traditional ultra-luxury European destinations such as Saint-Tropez, Capri, or Milan, Portugal offers a distinct competitive edge: the rare ability to marry high-end modern luxury with genuine cultural authenticity, historic preservation, and environmental nature.

This authenticity premium has driven the expansion of branded residences and mixed-use hospitality concepts, where five-star hotel operations act as catalysts, providing essential operational services, brand equity, and premium amenities to adjacent residential components.

► Mid-Market Shortage

In stark contrast to the fluid capital tracking luxury developments, the Portuguese domestic market faces a severe housing crisis within the middle-income and youth demographics.Following nearly a decade of minimal mid-market residential development, the country is grappling with an acute structural shortage.

Land values have inflated significantly with baseline parcel prices routinely reaching millions of Euros which, combined with elevated construction costs, makes it financially unviable for smaller development platforms to execute affordable housing projects.

One key market constraint today is that, under current financial structures, if a developer owns a land parcel capable of delivering identical volumes for either build-to-sell (BTS) or build-to-rent (BTR) paths, the BTS model is invariably prioritised.

Build-to-sell provides rapid capital recycling, high short-term profitability, and straightforward bank financing, as Portuguese financial institutions routinely provide development liquidity backed by pre-sales revenue generated during construction.

(GRI Institute)

► Portuguese BTR Dynamics

To establish a sustainable institutional BTR framework, the Portuguese real estate industry requires structural and product-level divergence from traditional models.Fiscal incentives - such as the implementation of a reduced 6% VAT rate for eligible construction and rehabilitation works active until 2032, provided relevant invoicing is executed by 2029 - offer necessary support but are insufficient on their own to reorient developer priorities.

True institutionalisation of the rental sector requires targeted municipal planning interventions and dedicated asset design strategies:

- Long-Term Rental Covenants: Regulations must ensure that assets developed under affordable or rental incentives are legally bound to the rental market for minimum horizons of 20 to 25 years, preventing premature conversion to build-to-sell when macro yields shift.

- Optimised Product Design: BTR assets must feature highly efficient, smaller layouts tailored specifically for utility and comfort rather than expansive luxury. Instead of standard 120-square-metre configurations, units should focus on compact, functional layouts.

- Transit-Oriented Development: BTR projects should be prioritised in suburban rings surrounding major employment hubs, situated within strict walking distances of main train and transit stations. Municipally permitting lower underground parking ratios near transit hubs drastically reduces excavation and construction costs, passing those savings directly to rental affordability.

However, because current operational BTR stock is virtually non-existent, this demand remains highly frustrated by lack of supply.

(GRI Institute)

► Demographic Realities and Alternative Assets

The intersection of shifting demographics and real estate metrics is paving the way for specialised alternative asset classes, specifically co-living, student housing, and independent senior living operations. The student housing sector has matured rapidly, yet substantial room for expansion remains.Operators are increasingly looking toward hybrid co-living designs that integrate student accommodation with young professional housing, successfully eliminating the financial drag of summer vacancy periods.

Furthermore, an immediate opportunity exists in the strategic repositioning and conversion of obsolete commercial office buildings.

Assets that lack modern ESG compliance, high-spec technological infrastructure, or large, flexible floor plans can no longer attract premium corporate tenants, which makes converting these structures into residential co-living layouts offer a highly viable secondary lifecycle.

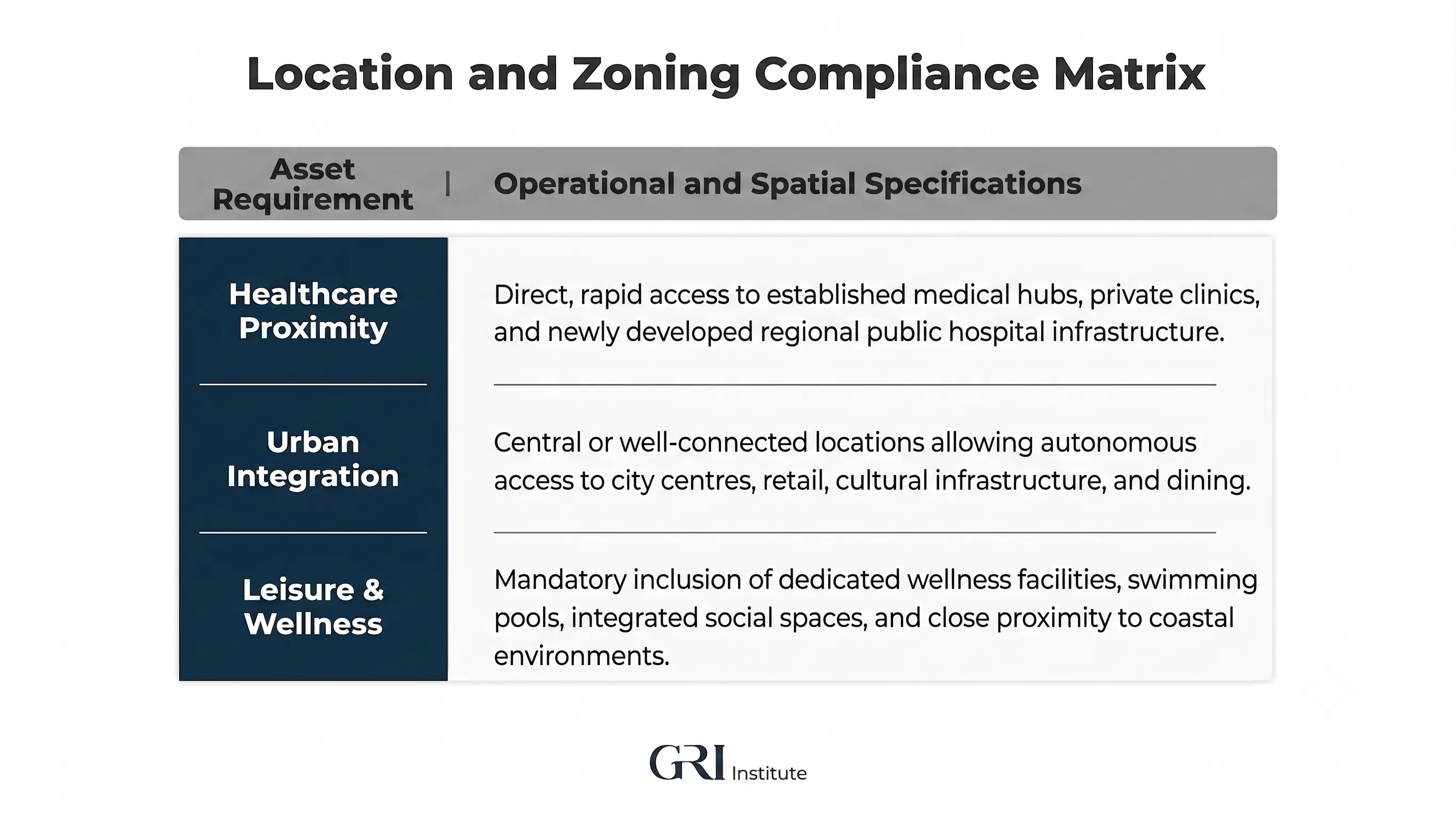

Concurrently, the aging population of both Portugal and northern Europe (including substantial expat flows from the Nordics, Germany, and the UK) is driving unprecedented interest in independent senior living.

This segment targets autonomous individuals aged 65 and over who wish to spend extended periods - such as six- to seven-month winter blocks in temperate coastal zones - while maintaining properties in their home countries.

Operational strategies frequently utilise tourist-licensed apartment frameworks refurbished specifically for senior requirements. The critical success factors for these independent living developments require strict compliance with specialised zoning and location matrices:

► Regulatory Modernisation

Historically, extensive administrative bureaucracy and multi-year licensing delays served as a primary detractor for institutional capital in Portugal, routinely compressing project yields and inflating development risk.The legislative introduction of the reformed administrative framework commonly referred to as the Simplex overhauls has fundamentally altered the development pipeline by aggressively reducing bureaucratic friction.

The core philosophy of the new framework represents a complete paradigm shift: moving away from slow, prospective municipal approvals toward absolute developer and technical accountability.

Under the updated regulations, if a project strictly complies with pre-approved municipal master plans, urban parameters, or detailed allotment frameworks, developers can bypass traditional waiting periods and initiate construction almost immediately upon submission.

Administrative response times have also been compressed to clear limits, with simplified initial planning requests (Pedido de Informação Prévia, or PIP) targeted at 20- to 30-day windows.

(GRI Institute)

► Licensing Overhauls

Crucially, the statutory period during which municipal councils retain retroactive supervision and enforcement rights over completed projects has been dramatically reduced from a legacy 10-year term down to just one single year, introducing vital long-term security for institutional funds.This operational shift demands an immediate transformation in the mindset of developers and technical teams. The era of submitting rudimentary, conceptual four-wall drawings with the intention of negotiating variations during multi-year approval delays is entirely over.

The current framework mandates highly advanced, rigorously detailed engineering and architectural execution completed entirely upfront. Because the technical signatures assume full legal and insurance liability for structural compliance, projects must be defensive, meticulously designed, and fully finalised prior to submission.

This institutional standard of project preparation is proving highly beneficial for banking institutions, facilitating smoother integration with corporate mortgage and project finance platforms by delivering clean, fully insured, and legally de-risked development structures from day one.

► Access even more insights on the region in our Portugal GRI 2026 Spotlight report here

These insights were shared during industry leader discussions at the GRI Women Leading Portuguese Real Estate 2026 roundtable, featuring contributions from moderator Filipa Arantes Pedroso (ImoLegal), along with Celma de Almeida Lavradio (Blue Buffalo Capital), Diane Daudin Clavaud (Nobu Hotels), and Izabela Vasconcelos (Sempre Investimentos).

► Check out all upcoming GRI Institute Europe gatherings here.