Credit: GRI Institute

Credit: GRI InstituteEurope’s real estate recovery is characterised by cautious LPs, the “defense dividend”, and specialised sectors

Insights from GRI Women Leading European Real Estate on capital shifts and the new operational era, plus exclusive survey results

March 5, 2026Real Estate

Written by:Helen Richards

Key Takeaways

- European real estate is entering a recovery phase bolstered by the "defense dividend", where increased sovereign spending on infrastructure and energy is attracting global investors.

- The market has transitioned from passive asset appreciation to an operational era where top-tier returns are dictated by deep technical expertise in specialised sectors.

- While valuation gaps are narrowing, the primary constraint for managers has shifted from pricing uncertainty to a cautious LP base.

In 2026, European real estate is exhibiting clear markers of recovery. As even previously shunned asset classes, such as retail and office, are regaining favour through significant repricing, the new era of investment will be defined by operational excellence, patient capital, and deep technical conviction.

This was the verdict that emerged at the GRI Women Leading European Real Estate forum, which gathered Europe’s most prominent female real estate leaders in London ahead of Europe GRI 2025 - Winter Edition.

Alongside the high-level knowledge exchange that took place during the meeting, participants took part in an open survey, gauging sentiment on the most critical market-related matters, including investment constraints, sector preferences, and capital flows.

The primary engine behind this renewed interest is what economists have dubbed the "defense dividend." The geopolitical landscape has necessitated a massive, multi-decade jump in defense and sovereign infrastructure spending across the European bloc.

Investors are now viewing these sectors through a pragmatic ESG lens. While defense was once an exclusion for many ESG-focused funds, the conversation has shifted toward the social and governance necessity of regional security and energy independence.

This surge in state-backed spending is creating a "buy" signal for real estate as increased industrial activity and the modernisation of energy grids are driving demand for specialised logistics, manufacturing hubs, and modernised office spaces in strategic European corridors.

On the debt side, the market has transitioned into a landscape of high supply, and even traditional banks are showing signs of a rebound, vocal about wanting to grow their loan books in the first half of the year. This high supply has driven spreads to all-time lows, making it an exceptionally compelling time for borrowers to refinance and extract liquidity to execute long-term business plans.

As valuations stabilise, the gap between buyers and sellers that previously paralysed the market is narrowing, allowing for more transparent trading. In this environment, managers are increasingly utilising secondaries to perform capital stack resets, injecting fresh equity into assets during refinancing events to sustain their business strategies.

Investors are increasingly bifurcating between new-build stock and the refurbishment of older assets, which often trade at a significant discount to replacement value.

A recurring theme is the power crunch - the ability to secure power allocation has become the ultimate differentiator for both logistics hubs and data centres.

Similarly, new sectors like truck parking are being institutionalised, focusing on secure locations driven by the fundamentals of e-commerce.

By professionalising a fragmented sector and addressing granular issues like safe parking for high-value goods, investors are finding alpha in the literal "gears" of the supply chain.

Participants took part in an open survey, gauging sentiment on the most critical market-related matters, including investment constraints, sector preferences, and capital flows. (Credit: GRI Institute)

Participants took part in an open survey, gauging sentiment on the most critical market-related matters, including investment constraints, sector preferences, and capital flows. (Credit: GRI Institute)

In an operational world, conviction must be backed by deep data, technical know-how, and the patience to ride out the cycle.

The survey results underscore a significant shift; valuation uncertainty and pricing gaps, which paralysed the market previously, have slipped down the priority list as pricing stabilises.

Instead, GPs are now grappling with an LP base that demands tangible proof of performance, specifically in the form of distributions and a proven track record.

Participants highlighted that even "naughty box" sectors like retail and office are seeing a selective return of interest as they reprice to attractive levels.

However, the living sector’s appeal lies in its resilience; as one leader noted, the housing crisis is so profound it is unlikely to be solved within a working lifetime.

The survey results reveal a dominant consensus among senior real estate professionals that capital is increasingly flowing toward sectors with strong structural fundamentals.

The living sector emerged as the primary beneficiary of "conviction-driven" capital, with more than half of respondents identifying it as the top area for deployment due to a chronic supply-demand imbalance.

Logistics followed with 20%, as investors double down on supply chain resilience and emerging sub-sectors like powered land and truck parking.

The ability to manage assets through their lifecycle, drive net operating income (NOI) growth, and professionalise data management is now the primary differentiator for top-performing GPs.

This shift is particularly evident in the living sector considering the immaturity of the sector, requiring a more professional, data-driven approach to stock selection and operations.

The era of simply buying a building and waiting for cap rate compression is over; today’s winners must be ready to work the assets harder than ever before.

These insights were shared during GRI Institute’s GRI Women Leading European Real Estate forum, with participation from Agata Jurek-Zbrojska (CMS), Audrey Klein (Spencer House Partners), Catherine Webster (Thriving Investments), Cherine Aboulzelof (BGO), Ioanna Paschalidou (Henderson Park Capital), Irene Ryan (Starwood Capital Group), Jenny Wang (Sunrise Real Estate), Jessica Hardman (Aboria Capital), and Shelby Weiss (GREYKITE).

This was the verdict that emerged at the GRI Women Leading European Real Estate forum, which gathered Europe’s most prominent female real estate leaders in London ahead of Europe GRI 2025 - Winter Edition.

Alongside the high-level knowledge exchange that took place during the meeting, participants took part in an open survey, gauging sentiment on the most critical market-related matters, including investment constraints, sector preferences, and capital flows.

Shifting Capital Landscape

A significant recalibration is underway in global capital flows as North American LPs increasingly pivot toward Europe. No longer viewed merely as a secondary diversification play, the continent is being reclassified as a primary strategic destination for capital allocation. This trend is underpinned by a search for relative value as US markets face their own set of pricing and regulatory hurdles.The primary engine behind this renewed interest is what economists have dubbed the "defense dividend." The geopolitical landscape has necessitated a massive, multi-decade jump in defense and sovereign infrastructure spending across the European bloc.

Investors are now viewing these sectors through a pragmatic ESG lens. While defense was once an exclusion for many ESG-focused funds, the conversation has shifted toward the social and governance necessity of regional security and energy independence.

This surge in state-backed spending is creating a "buy" signal for real estate as increased industrial activity and the modernisation of energy grids are driving demand for specialised logistics, manufacturing hubs, and modernised office spaces in strategic European corridors.

European Real Estate forum in London gathered the industry’s most prominent female leaders to address the future of the European real estate market. (Credit: GRI Institute)

The Liquidity Puzzle

For many investment managers, the last three years have been a struggle to exit investments. This frozen environment has led to a surge in the secondary market, which has seen a huge jump in adoption over the last five years. Roughly 70% of this market is now driven by managers recapping their own funds or assets to create liquidity.On the debt side, the market has transitioned into a landscape of high supply, and even traditional banks are showing signs of a rebound, vocal about wanting to grow their loan books in the first half of the year. This high supply has driven spreads to all-time lows, making it an exceptionally compelling time for borrowers to refinance and extract liquidity to execute long-term business plans.

As valuations stabilise, the gap between buyers and sellers that previously paralysed the market is narrowing, allowing for more transparent trading. In this environment, managers are increasingly utilising secondaries to perform capital stack resets, injecting fresh equity into assets during refinancing events to sustain their business strategies.

Consensus among real estate leaders highlights the importance of technical expertise and operational knowledge. (Credit: GRI Institute)

High Conviction Sectors

Current strategies emphasise that in a mature market, being a jack of all trades is no longer viable. Instead, investors are diving into highly specialised sectors with high barriers to entry that require technical expertise or operational knowledge to institutionalise.The Living Sector

The housing crisis, particularly in the UK, remains a primary driver for investment. While the total housing market is massive, institutional ownership remains minor, representing a significant runway for growth.Investors are increasingly bifurcating between new-build stock and the refurbishment of older assets, which often trade at a significant discount to replacement value.

Logistics and the Power Crunch

In the logistics space, conviction now means being incredibly picky about the micro details. Tenants today are rejecting assets for small flaws, such as triangular yards or insufficient floor flatness for warehouse robots.A recurring theme is the power crunch - the ability to secure power allocation has become the ultimate differentiator for both logistics hubs and data centres.

New Frontiers: Digital and Infrastructure

Innovative strategies are emerging in powered land investment. By acquiring land subject to securing power and permits, investors can capitalise on the massive demand for AI and internet adoption without necessarily taking on the full technology risk of data centre development.Similarly, new sectors like truck parking are being institutionalised, focusing on secure locations driven by the fundamentals of e-commerce.

By professionalising a fragmented sector and addressing granular issues like safe parking for high-value goods, investors are finding alpha in the literal "gears" of the supply chain.

Participants took part in an open survey, gauging sentiment on the most critical market-related matters, including investment constraints, sector preferences, and capital flows. (Credit: GRI Institute)The Verdict for 2026

The consensus is that the era of rising tides lifting all boats is over. As the market moves forward, the decisions that matter most involve stock selection, scale, and the ability to realise deals through optionality at exit.In an operational world, conviction must be backed by deep data, technical know-how, and the patience to ride out the cycle.

The Survey Results

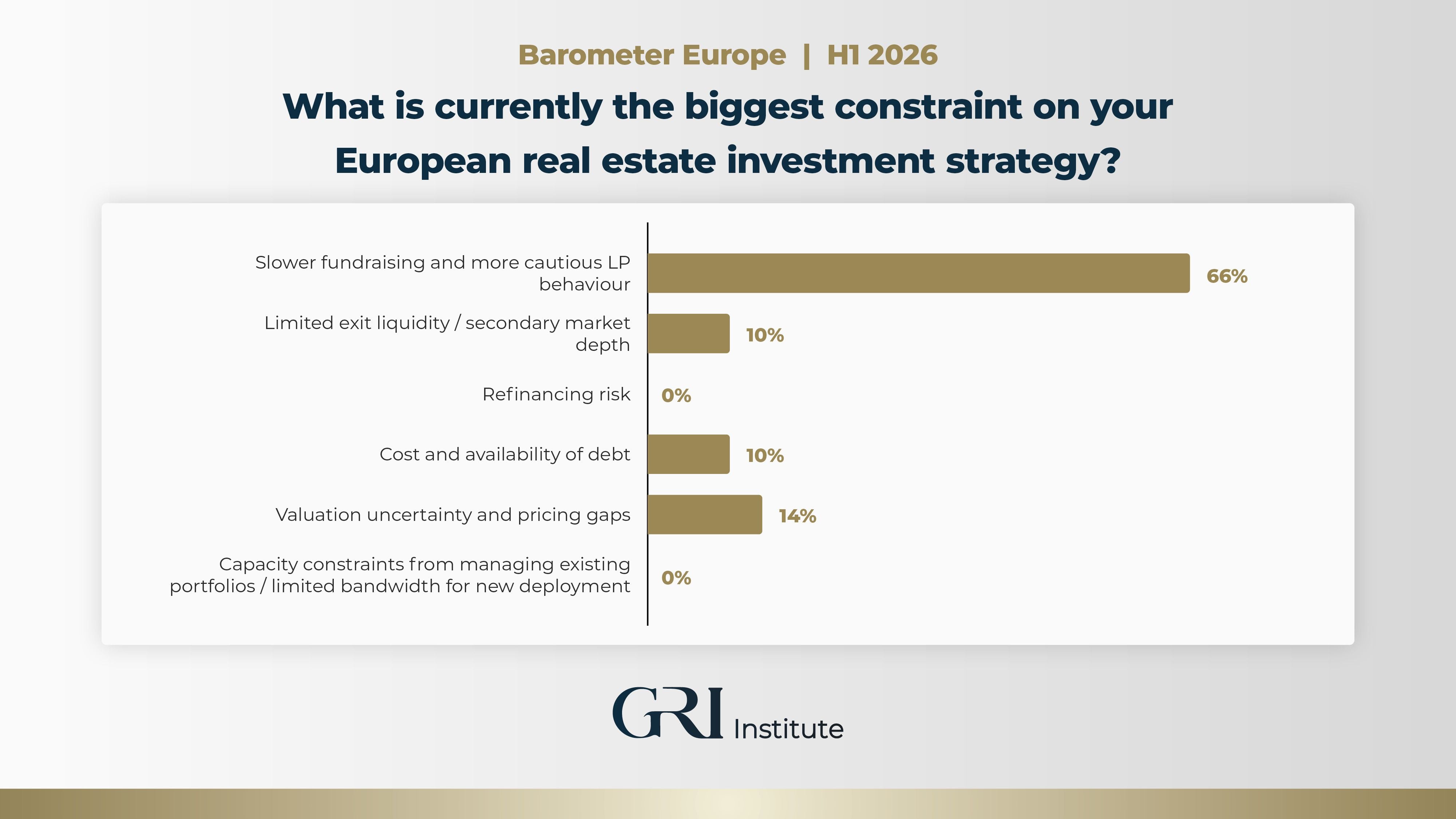

What is currently the biggest constraint on your European real estate investment strategy?

Despite signs of recovery in 2026, the primary challenge remains the cautious behaviour of LPs. For many GPs, the fundraising environment has shifted into a marathon, requiring more than just a glossy pitch book to unlock capital.The survey results underscore a significant shift; valuation uncertainty and pricing gaps, which paralysed the market previously, have slipped down the priority list as pricing stabilises.

Instead, GPs are now grappling with an LP base that demands tangible proof of performance, specifically in the form of distributions and a proven track record.

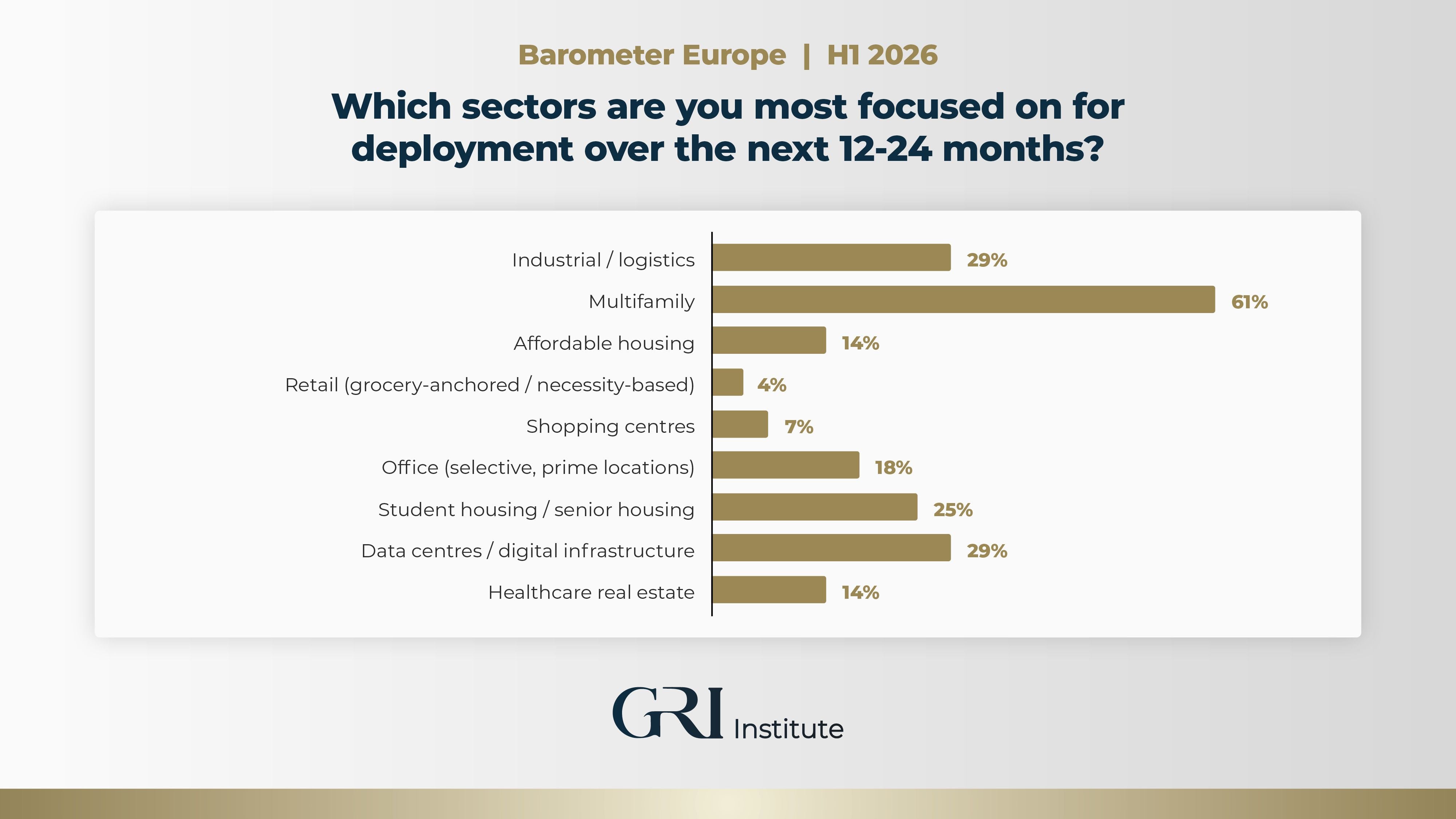

Which sectors are you most focused on for deployment over the next 12-24 months?

Regarding sector preferences, the "beds and sheds" thesis remains dominant. Multifamily housing continues to be a clear favourite, buoyed by a chronic supply-demand imbalance across the continent.Participants highlighted that even "naughty box" sectors like retail and office are seeing a selective return of interest as they reprice to attractive levels.

However, the living sector’s appeal lies in its resilience; as one leader noted, the housing crisis is so profound it is unlikely to be solved within a working lifetime.

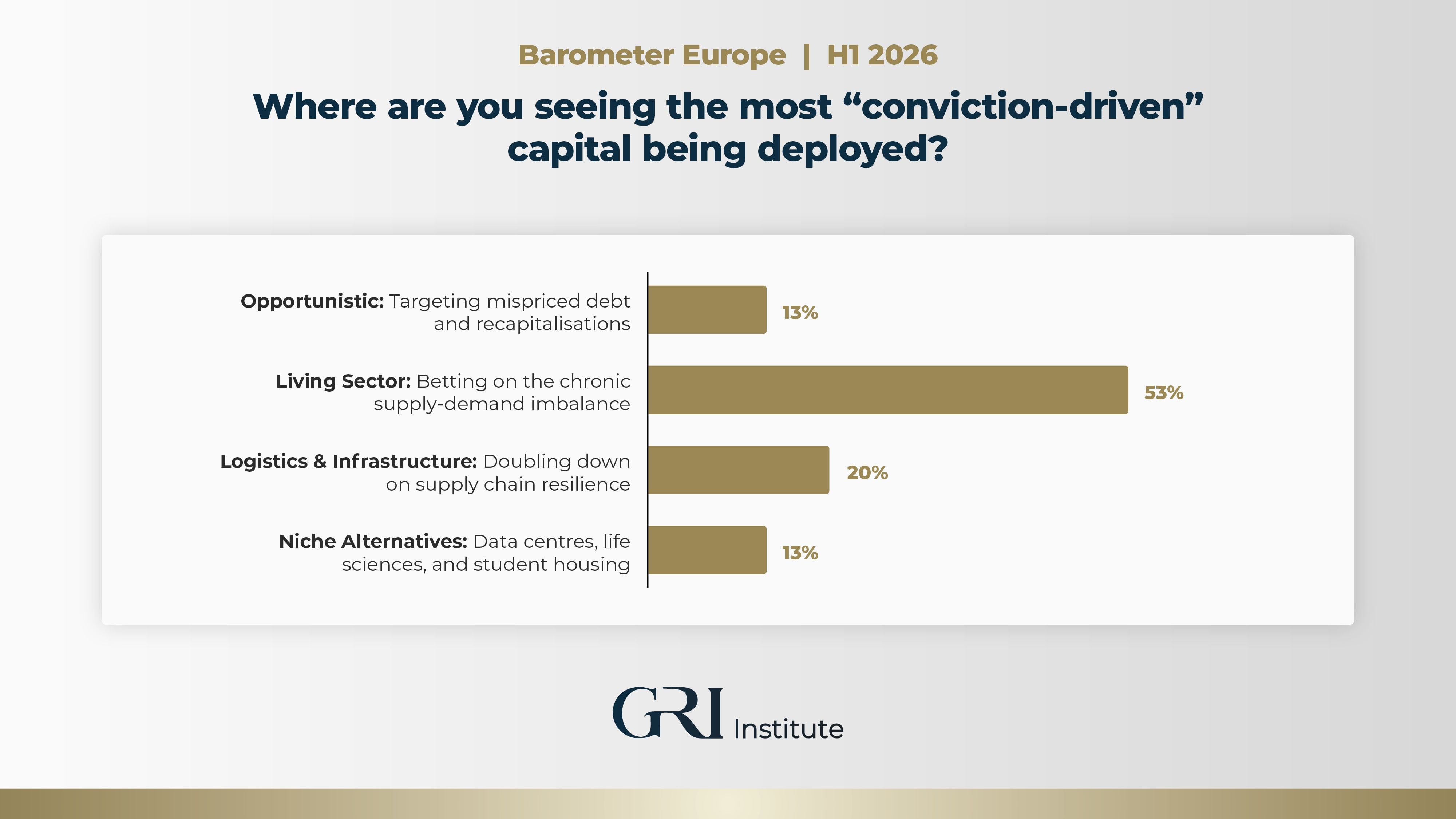

Where are you seeing the most “conviction-driven” capital being deployed?

The survey results reveal a dominant consensus among senior real estate professionals that capital is increasingly flowing toward sectors with strong structural fundamentals.

The living sector emerged as the primary beneficiary of "conviction-driven" capital, with more than half of respondents identifying it as the top area for deployment due to a chronic supply-demand imbalance.

Logistics followed with 20%, as investors double down on supply chain resilience and emerging sub-sectors like powered land and truck parking.

Over the next 12-18 months, what will most differentiate top-performing GPs?

Perhaps the most telling insight from the discussions and polling was the recognition that real estate has moved beyond being a mere asset to being an operational business.The ability to manage assets through their lifecycle, drive net operating income (NOI) growth, and professionalise data management is now the primary differentiator for top-performing GPs.

This shift is particularly evident in the living sector considering the immaturity of the sector, requiring a more professional, data-driven approach to stock selection and operations.

The era of simply buying a building and waiting for cap rate compression is over; today’s winners must be ready to work the assets harder than ever before.

These insights were shared during GRI Institute’s GRI Women Leading European Real Estate forum, with participation from Agata Jurek-Zbrojska (CMS), Audrey Klein (Spencer House Partners), Catherine Webster (Thriving Investments), Cherine Aboulzelof (BGO), Ioanna Paschalidou (Henderson Park Capital), Irene Ryan (Starwood Capital Group), Jenny Wang (Sunrise Real Estate), Jessica Hardman (Aboria Capital), and Shelby Weiss (GREYKITE).