Credit: Adobe Stock

Credit: Adobe StockUncovering hidden potential in the European CRE market

How prime locations and the refinancing cycle are creating new investment opportunities in office, retail, and logistics sectors

October 27, 2025Real Estate

Written by:Rory Hickman

Key Takeaways

As the commercial real estate (CRE) sector adapts to evolving market conditions, industry leaders are navigating a landscape shaped by changing consumer behaviours, economic uncertainty, and shifting investment priorities.

While traditional sectors like offices and retail continue to face structural challenges, signs of a potential turnaround are beginning to emerge, particularly for the best properties in prime locations.

In this article, we delve into the current CRE scenario based on insights shared during discussions at the GRI Institute’s gatherings and the latest industry research to offer an analysis of how the market is evolving and where the top opportunities lie in the coming year.

Office and retail assets remain constrained by structural challenges linked to workplace change and consumer behaviour, though niche opportunities may still arise in prime locations and signs of a turnaround have been seen.

Although office space is still at the bottom of the list, things are "picking up" and are expected to change in the next six months, especially if transaction volumes in the US increase. Offices and retail have been through their repricing cycles and are now seen as attractive investment options.

The CRE market is currently in a refinancing cycle, with many assets trapped because owners do not want to crystallise asset value in a slow transaction market. The largest driver for a pickup in acquisitions is likely to be a return of core capital that will make clearing prices more visible.

Lenders have generally been accommodating, giving people more time to work through their loans, and there's no sign of distress being forced by banks. Geopolitics and AI are major uncertainties, but the main professional challenge is to ensure time is spent on the right deals and avoiding losses.

A new trend is the integration of operators into core strategy to secure income and ensure resilience. While some investors prefer a traditional lease agreement, others are embracing management contracts. A lease is only as secure as the tenant's financial standing, and in case of a problem, a management contract allows the investor to take over operations.

Well-located offices are also seen as a strong bet considering the leverage with tenants and historically strong performance, while retail in top locations is viewed as a solid core strategy, as the tenant typically handles the capex and fit-out, making it a resilient option with less operational work for the investor.

While these transactions are often limited to large investors or sovereign funds, and despite the challenges, core is still considered the backbone of the market for long-term players who need secure revenue streams and cash flow.

With offices and retail sectors showing signs of a potential rebound, the focus is shifting towards high-quality, well-located assets that have weathered the repricing cycles. These prime properties - especially those in sought-after locations - are likely to see renewed investor interest in the coming months, presenting new opportunities for those poised to act.

While the logistical and light industrial sectors remain resilient, the key to unlocking the next big opportunities may be found in well-positioned office and retail assets that can be repurposed or repositioned to meet the evolving demands of the market.

The ongoing refinancing cycle suggests that the market is not yet in full recovery, but there are emerging hints that core capital may soon flow back into the sector, revealing more attractive clearing prices. However, this will require investors to be strategic, focusing on assets with the strongest long-term potential and resilience.

Investors who can balance traditional models with innovative strategies - such as integrating operators for greater income security or embracing mixed-use developments - are likely to find themselves at the forefront of the next wave of CRE growth.

Learn more about these issues in our full report - European Commercial Real Estate Outlook 2025/26. Access below:

- Despite ongoing challenges, prime office and retail assets in top locations are showing signs of recovery, presenting new opportunities for investors.

- The current CRE refinancing cycle is leading to trapped assets, with core capital poised to drive acquisitions as clearing prices become more visible.

- Investors are focusing on well-positioned assets, coupled with innovative strategies such as integrating operators or embracing mixed-use developments.

As the commercial real estate (CRE) sector adapts to evolving market conditions, industry leaders are navigating a landscape shaped by changing consumer behaviours, economic uncertainty, and shifting investment priorities.

While traditional sectors like offices and retail continue to face structural challenges, signs of a potential turnaround are beginning to emerge, particularly for the best properties in prime locations.

In this article, we delve into the current CRE scenario based on insights shared during discussions at the GRI Institute’s gatherings and the latest industry research to offer an analysis of how the market is evolving and where the top opportunities lie in the coming year.

Industry Leader Outlook

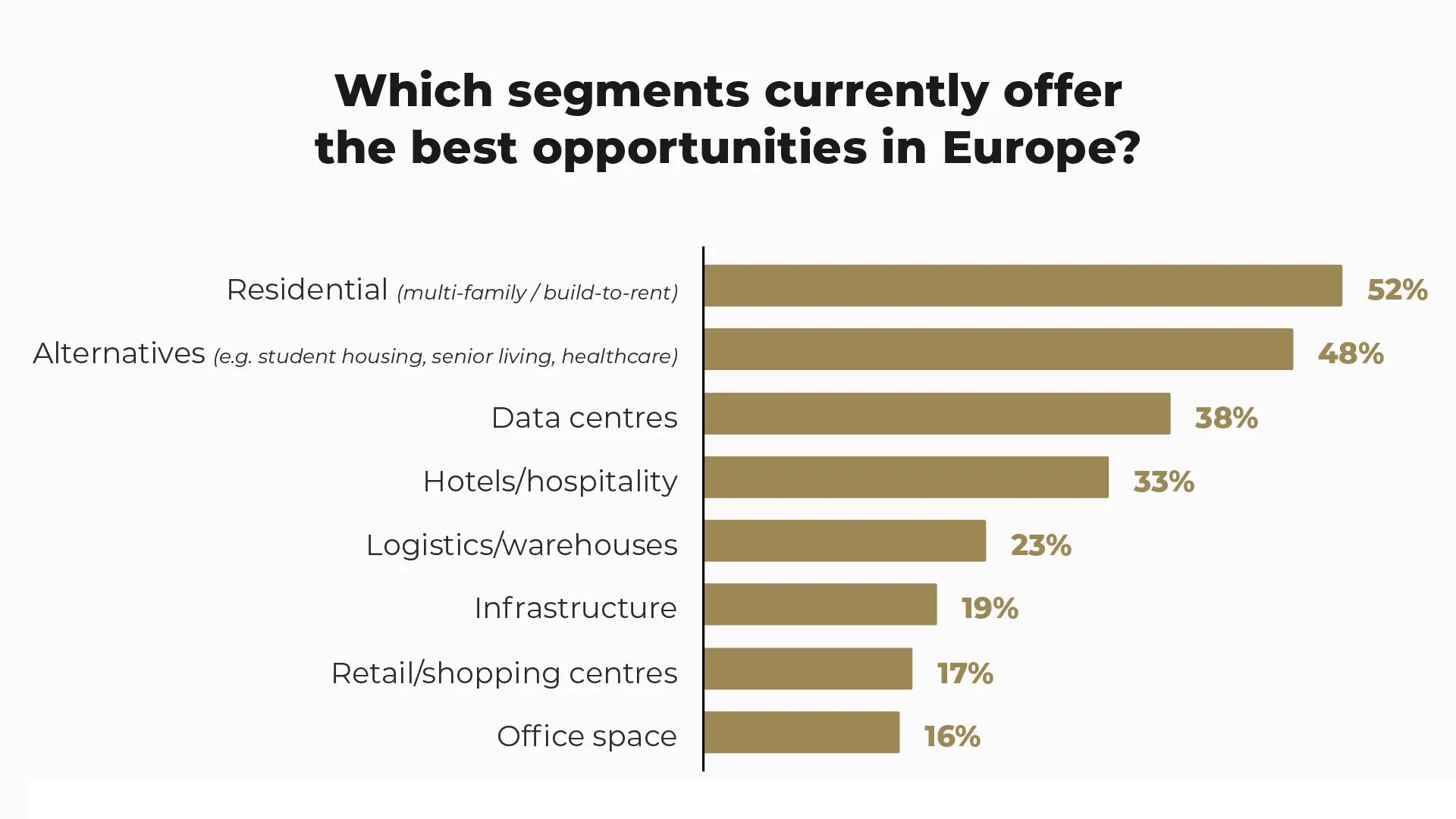

In a recent GRI Institute survey of top industry leaders, when asked about their outlook on the segments with the best opportunities over the next 12 months, CRE sectors performed less favourably than others, with logistics at 23%, retail at 17%, and offices at 16%.Office and retail assets remain constrained by structural challenges linked to workplace change and consumer behaviour, though niche opportunities may still arise in prime locations and signs of a turnaround have been seen.

Although office space is still at the bottom of the list, things are "picking up" and are expected to change in the next six months, especially if transaction volumes in the US increase. Offices and retail have been through their repricing cycles and are now seen as attractive investment options.

Although commercial real estate lags significantly behind other sectors when it comes to industry outlook, signs of a potential turnaround are beginning to emerge. (Source: GRI Barometer: European RE Outlook H2 2025)

The CRE market is currently in a refinancing cycle, with many assets trapped because owners do not want to crystallise asset value in a slow transaction market. The largest driver for a pickup in acquisitions is likely to be a return of core capital that will make clearing prices more visible.

Lenders have generally been accommodating, giving people more time to work through their loans, and there's no sign of distress being forced by banks. Geopolitics and AI are major uncertainties, but the main professional challenge is to ensure time is spent on the right deals and avoiding losses.

Commercial Core

The definition of a secure core asset has narrowed, with a truly high-quality core investment now classed as a prime property, located in a top area, with a strong tenant - regardless of the sector. This is contrasted with properties that are considered core simply due to having a long lease, but are technically obsolete or struggle to find tenants.A new trend is the integration of operators into core strategy to secure income and ensure resilience. While some investors prefer a traditional lease agreement, others are embracing management contracts. A lease is only as secure as the tenant's financial standing, and in case of a problem, a management contract allows the investor to take over operations.

Well-located offices are also seen as a strong bet considering the leverage with tenants and historically strong performance, while retail in top locations is viewed as a solid core strategy, as the tenant typically handles the capex and fit-out, making it a resilient option with less operational work for the investor.

While these transactions are often limited to large investors or sovereign funds, and despite the challenges, core is still considered the backbone of the market for long-term players who need secure revenue streams and cash flow.

Retail in top locations is viewed as a solid core strategy, as the tenant typically handles the capex and fit-out, making it a resilient option (Freepik)

GRI Analysis

As the commercial real estate sector continues to navigate a period of transformation, the path forward seems less about quick fixes and more about strategic recalibration.With offices and retail sectors showing signs of a potential rebound, the focus is shifting towards high-quality, well-located assets that have weathered the repricing cycles. These prime properties - especially those in sought-after locations - are likely to see renewed investor interest in the coming months, presenting new opportunities for those poised to act.

While the logistical and light industrial sectors remain resilient, the key to unlocking the next big opportunities may be found in well-positioned office and retail assets that can be repurposed or repositioned to meet the evolving demands of the market.

The ongoing refinancing cycle suggests that the market is not yet in full recovery, but there are emerging hints that core capital may soon flow back into the sector, revealing more attractive clearing prices. However, this will require investors to be strategic, focusing on assets with the strongest long-term potential and resilience.

Investors who can balance traditional models with innovative strategies - such as integrating operators for greater income security or embracing mixed-use developments - are likely to find themselves at the forefront of the next wave of CRE growth.

Learn more about these issues in our full report - European Commercial Real Estate Outlook 2025/26. Access below: