Credit: GRI Institute

Credit: GRI InstituteReal Estate's Great Unfreeze: GRI survey reveals 79% of investors plan to increase investment volumes

Top real estate leaders share their outlook on recovery, geopolitical concerns, and high-growth sectors in an exclusive GRI survey

November 27, 2025Real Estate

Written by:Helen Richards

Key Takeaways

- Optimism in the global real estate market surged from 60% to 72% between January and November 2025, signalling recovery confidence.

- Geopolitical instability has become the primary concern for real estate leaders, surpassing financial worries like interest rates.

- Data centres and digital infrastructure are expected to outperform other asset classes, reflecting growth driven by AI and cloud computing.

The survey which took place at the GRI Global Chairmen's Retreat 2025 in November in Abu Dhabi, among the world’s most respected real estate market players, involved a comprehensive set of questions covering crucial areas ranging from immediate industry health and chief investor anxieties, to strategic capital deployment intentions over the next 12-18 months.

The collective expertise and strategic outlook from these industry leaders are revealed in the following section in the form of the full survey results and analysis.

The insights herein offer an indispensable barometer for understanding current market dynamics and informing forward-looking real estate investment strategies.

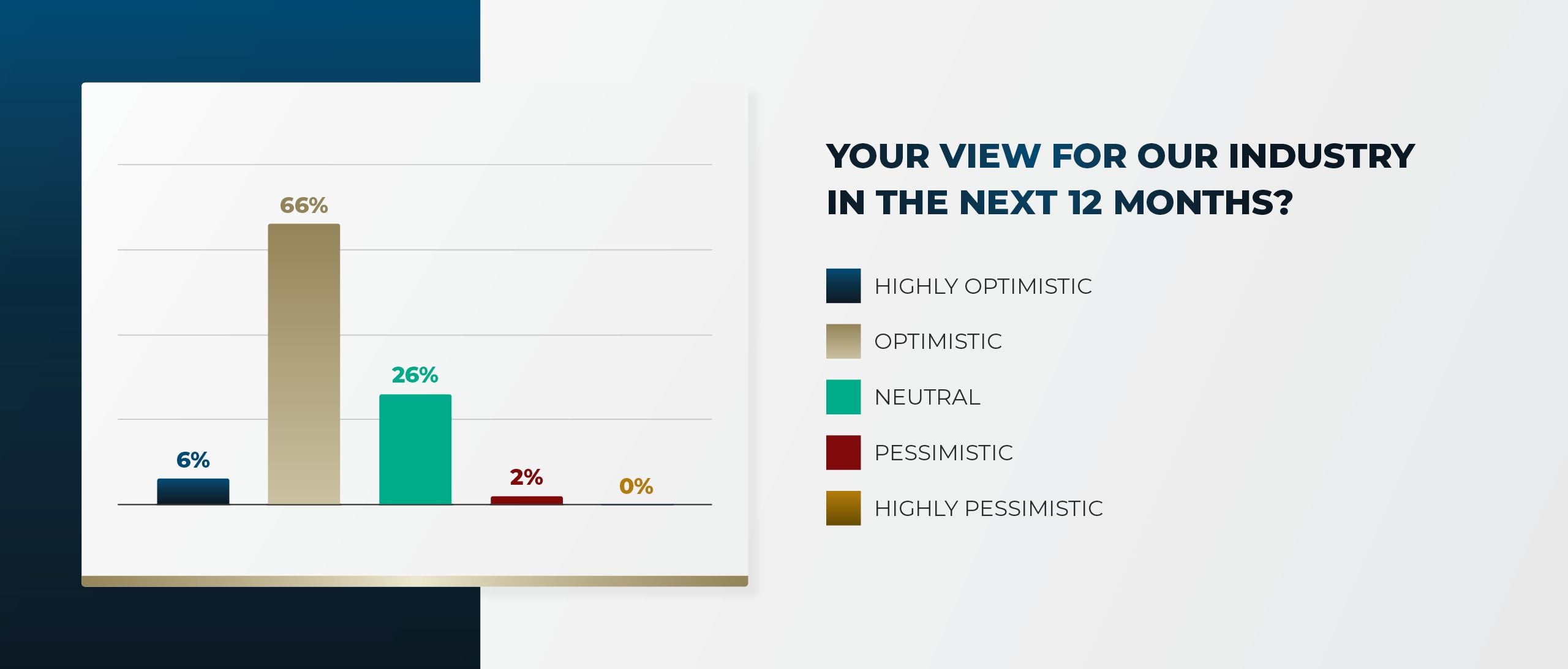

The global real estate sentiment among industry leaders experienced a profound positive shift since the previous survey that took place in January at the Chairmen’s Retreat 2025 in St Moritz.

When compared with the most recent survey from November at the Global Chairmen’s Retreat 2025 in Abu Dhabi, the combined net optimism (highly optimistic and optimistic views) surged from 60% to 72%, while net pessimism (pessimistic and highly pessimistic views) dropped from 13% to a mere 2%. This remarkable change signals a transition from cautious optimism to stronger confidence.

The vast majority of respondents who held pessimistic views in January 2025 shifted into the optimistic camp by November. The neutral view remained relatively stable among respondents, only dropping 1%, suggesting the shift was primarily from the formerly pessimistic players moving into the optimistic camp.

The shift in sentiment between January and November likely reflects a growing conviction that the global real estate market has reached or passed its bottom and is entering a recovery phase.

This optimism is generally supported by several improving market environment and macro factors observed throughout 2025, including interest rate stabilisation and improved capital accessibility.

The greatest worries for global real estate leaders underwent a fundamental shift in 2025, moving decisively from economic anxiety to geopolitical concerns.

When reviewing the survey results from the Chairmen’s Retreat 2025 in January, inflation and interest rates were the chief concern at 55%, reflecting the immediate pressure of high debt costs and central bank policy uncertainty on the real estate sector.

However, this worry has significantly retreated to 37%, suggesting the market has seen a peak in the rate cycle while also successfully adjusting to the overall higher cost of capital.

Simultaneously, anxieties related to geopolitical tensions (including conflicts and security concerns) have surged substantially from 40% to become the dominant worry at 74%, indicating that escalating global conflicts and geo-economic fragmentation now supersede financial concerns as the most immediate threat to market stability and international investment flows.

This pivot reflects a year of increasing global volatility, likely driven by escalating international conflicts, rising US-China trade tensions, and sustained US domestic political uncertainty (which held steady at 24%).

The data suggests that while the real estate industry is finding its footing amid a new monetary policy landscape, its focus has been entirely captured by the growing threat of global instability, which now dictates capital allocation, risk assessment, and long-term planning more than other macro factors.

The results indicate a highly active and confident market sentiment among global real estate market players, pointing to a strong cycle of capital deployment.

A formidable total of 79% of respondents plan to increase their investment volume, suggesting that global capital has overcome recent uncertainties and is actively moving off the sidelines.

The most telling figure is that almost half (46%) anticipate a significant increase of more than 20% in investment volume. This signals that investors are not merely maintaining activity but are seeking to unlock dry powder at scale, aiming to capitalise on pricing dislocations and opportunities created by the higher interest rate environment.

The minimal share (4%) predicting any decrease underscores high confidence in the long-term fundamentals and resilience of the global real estate sector. The primary challenge moving forward will be securing quality assets amid high liquidity.

The results highlight an interesting shift in global investment conviction, establishing data centres and digital infrastructure as the sector expected to deliver the highest returns over the next 12 months, underscoring the powerful structural tailwinds created by AI, cloud computing, and massive data consumption.

This shows investors are prioritising high-growth, long-lease, and inflation-linked digital infrastructure over traditional real estate.

Residential and multifamily (21%) hold a strong second place, reinforcing their perception as a core, defensive asset class driven by demographic fundamentals globally.

The similar weight given to prime office (15%) and retail (15%) suggests that capital is highly selective. Investors believe that only the most superior office assets or highly defensive, experience-led / necessity-based retail will thrive, leaving no room for mid-tier or obsolete assets.

The surprisingly low ranking of logistics and industrial (8%) suggests that while it remains a strong sector, investors believe the period of exceptional returns (post-e-commerce boom) may be softening, or that the yields on these assets have compressed too far to be the best performer compared to the growth potential of data centres.

The results clearly establish that the primary impediment to transaction volume is pricing misalignment, followed by the cost of capital.

The bid-ask spread (34%) is the single greatest challenge. This indicates that despite the high capital appetite seen in the third question, sellers' price expectations have not yet fully adjusted to the new interest rate environment and higher cost of capital. This gap is freezing liquidity.

High cost of debt (24%) is the second major factor. This is a direct measure of the ongoing impact of elevated interest rates, affecting both new deal underwriting and the refinancing of maturing loans.

The combination of investor / committee hesitation (20%) and the difficulty in sourcing attractive opportunities (17%) shows that capital is being deployed slowly. Investors are selective, demanding a higher risk premium for the uncertainty, and are struggling to find truly compelling deals that meet their return hurdles in an efficient market.

The low response for lack of clear regulatory framework (5%) suggests that, for this sophisticated global audience, macro-financial factors far outweigh localised regulatory concerns as a barrier to entry.

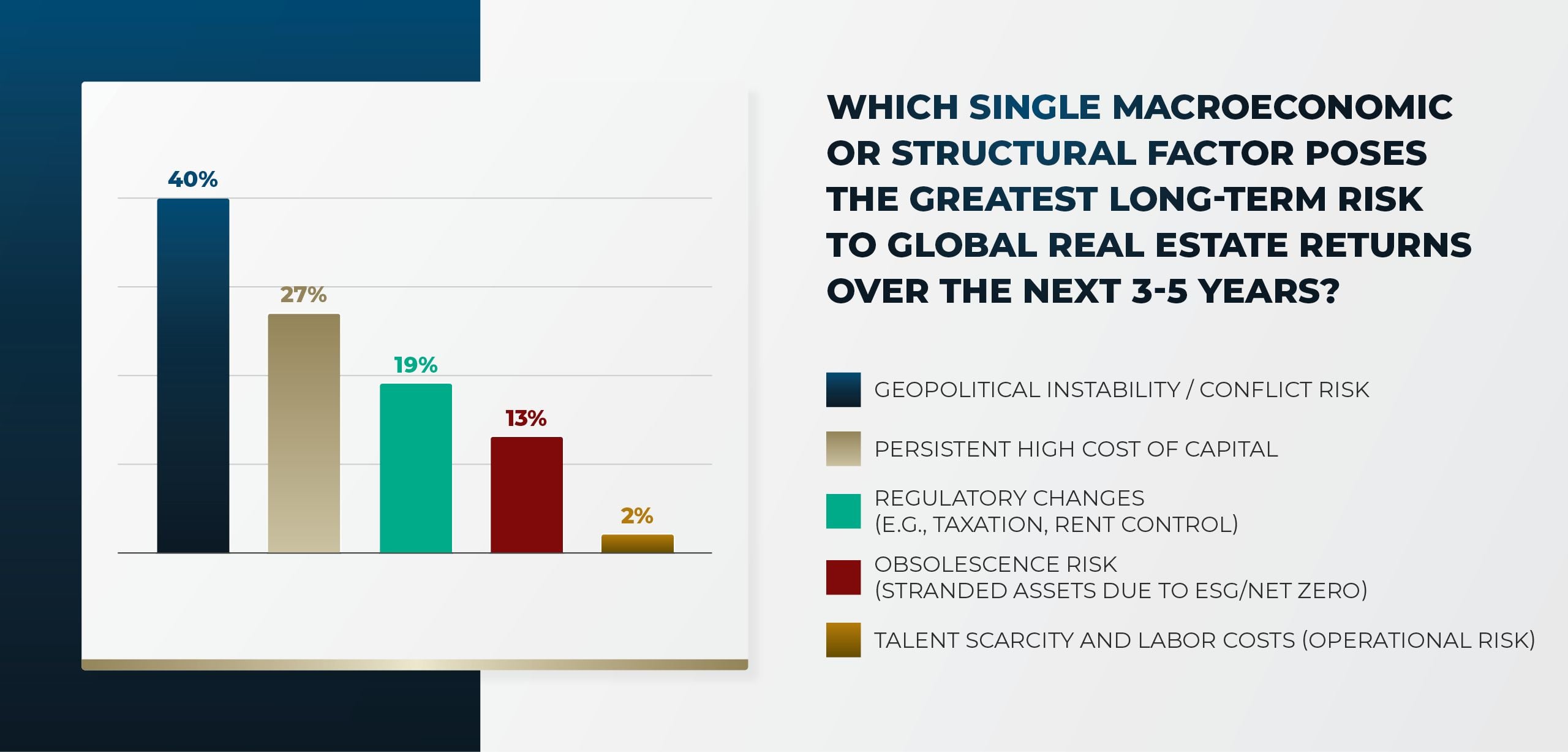

The results emphatically position geopolitical instability as the single most critical long-term concern for global real estate returns, with 40% of global leaders viewing it as the paramount long-term risk, surpassing immediate financial and structural concerns.

This reflects the audience's exposure to cross-border capital flows and recognises that macro-political fragmentation and conflict pose a fundamental threat to market stability, trade, and investor confidence - a risk far beyond property fundamentals.

Persistent high cost of capital (27%) secures the second position. Investors recognise that even with the stabilisation of rates, the era of ultra-low, zero-cost debt may be over, making capital costs a permanent structural constraint on valuation and underwriting going forward.

Regulatory changes (19%) and obsolescence risk (13%) are significant, yet secondary. This indicates that while localised policies (taxation, rent control) pose specific threats, the market currently perceives them as less pervasive than macro-finance or geopolitics.

Furthermore, while ESG is critical, its immediate impact as a risk factor is currently rated lower than the cost of capital or political instability.

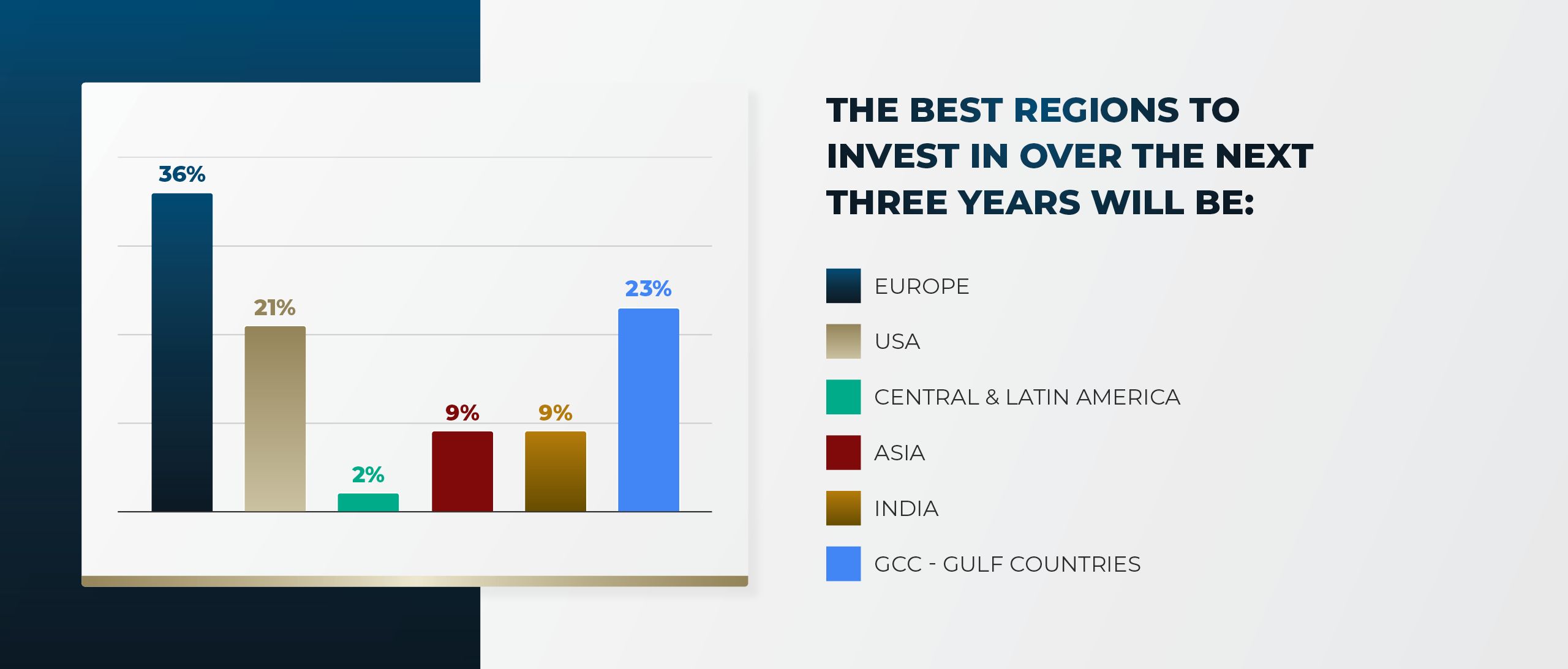

The global real estate market sentiment points to Europe as the top investment region for the next three years (36%), driven by the belief that the market has repriced and is now an attractive entry point, supported by expected ECB interest rate cuts and strong rental growth potential from supply shortages.

The second tier is divided between the GCC countries (23%), which appeal due to government-backed mega-projects and significant wealth inflow, and the USA (21%), where sentiment is tempered by a potentially higher-for-longer interest rate environment.

Overall, investors are prioritising markets offering either a cyclical recovery (Europe) or structural, rapid growth (GCC), while regions like Central and Latin America receive minimal attention (2%) due to perceived higher risks.

Looking ahead, real estate leaders must balance cautious optimism with strategic investments in high-growth sectors, particularly in regions poised for cyclical recovery or rapid development, while remaining agile in response to geopolitical and economic shifts that could impact long-term stability.

Discover more insights from the GRI Global Chairmen’s Retreat in our full report.

The collective expertise and strategic outlook from these industry leaders are revealed in the following section in the form of the full survey results and analysis.

The insights herein offer an indispensable barometer for understanding current market dynamics and informing forward-looking real estate investment strategies.

What is your view for our industry in the next 12 months?

(GRI Institute)

The global real estate sentiment among industry leaders experienced a profound positive shift since the previous survey that took place in January at the Chairmen’s Retreat 2025 in St Moritz.

When compared with the most recent survey from November at the Global Chairmen’s Retreat 2025 in Abu Dhabi, the combined net optimism (highly optimistic and optimistic views) surged from 60% to 72%, while net pessimism (pessimistic and highly pessimistic views) dropped from 13% to a mere 2%. This remarkable change signals a transition from cautious optimism to stronger confidence.

The vast majority of respondents who held pessimistic views in January 2025 shifted into the optimistic camp by November. The neutral view remained relatively stable among respondents, only dropping 1%, suggesting the shift was primarily from the formerly pessimistic players moving into the optimistic camp.

The shift in sentiment between January and November likely reflects a growing conviction that the global real estate market has reached or passed its bottom and is entering a recovery phase.

This optimism is generally supported by several improving market environment and macro factors observed throughout 2025, including interest rate stabilisation and improved capital accessibility.

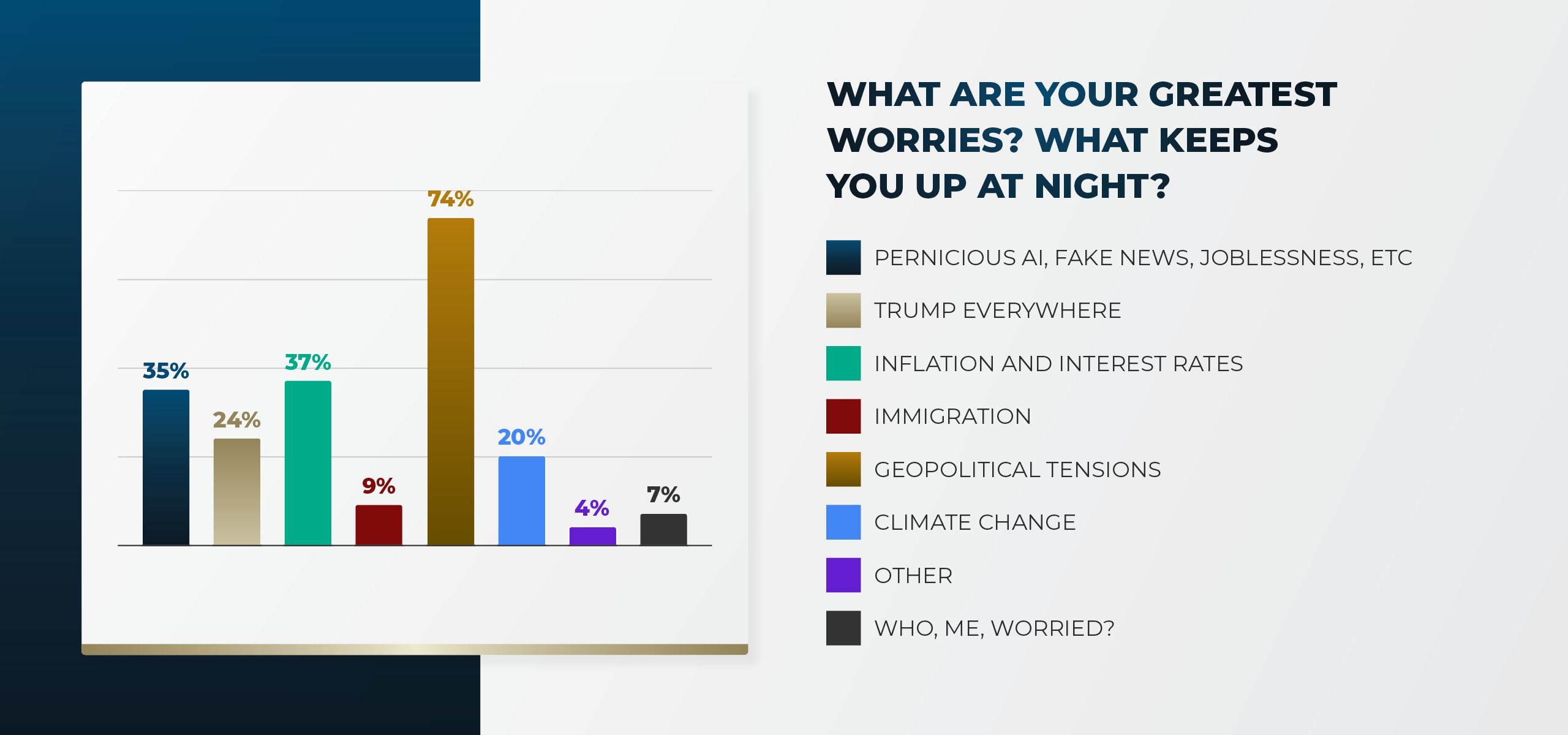

What are your greatest worries? What keeps you up at night?

(GRI Institute)

The greatest worries for global real estate leaders underwent a fundamental shift in 2025, moving decisively from economic anxiety to geopolitical concerns.

When reviewing the survey results from the Chairmen’s Retreat 2025 in January, inflation and interest rates were the chief concern at 55%, reflecting the immediate pressure of high debt costs and central bank policy uncertainty on the real estate sector.

However, this worry has significantly retreated to 37%, suggesting the market has seen a peak in the rate cycle while also successfully adjusting to the overall higher cost of capital.

Simultaneously, anxieties related to geopolitical tensions (including conflicts and security concerns) have surged substantially from 40% to become the dominant worry at 74%, indicating that escalating global conflicts and geo-economic fragmentation now supersede financial concerns as the most immediate threat to market stability and international investment flows.

This pivot reflects a year of increasing global volatility, likely driven by escalating international conflicts, rising US-China trade tensions, and sustained US domestic political uncertainty (which held steady at 24%).

The data suggests that while the real estate industry is finding its footing amid a new monetary policy landscape, its focus has been entirely captured by the growing threat of global instability, which now dictates capital allocation, risk assessment, and long-term planning more than other macro factors.

How do you anticipate your firm's real estate investment volume will change over the next 12-18 months compared to the previous period?

(GRI Institute)

The results indicate a highly active and confident market sentiment among global real estate market players, pointing to a strong cycle of capital deployment.

A formidable total of 79% of respondents plan to increase their investment volume, suggesting that global capital has overcome recent uncertainties and is actively moving off the sidelines.

The most telling figure is that almost half (46%) anticipate a significant increase of more than 20% in investment volume. This signals that investors are not merely maintaining activity but are seeking to unlock dry powder at scale, aiming to capitalise on pricing dislocations and opportunities created by the higher interest rate environment.

The minimal share (4%) predicting any decrease underscores high confidence in the long-term fundamentals and resilience of the global real estate sector. The primary challenge moving forward will be securing quality assets amid high liquidity.

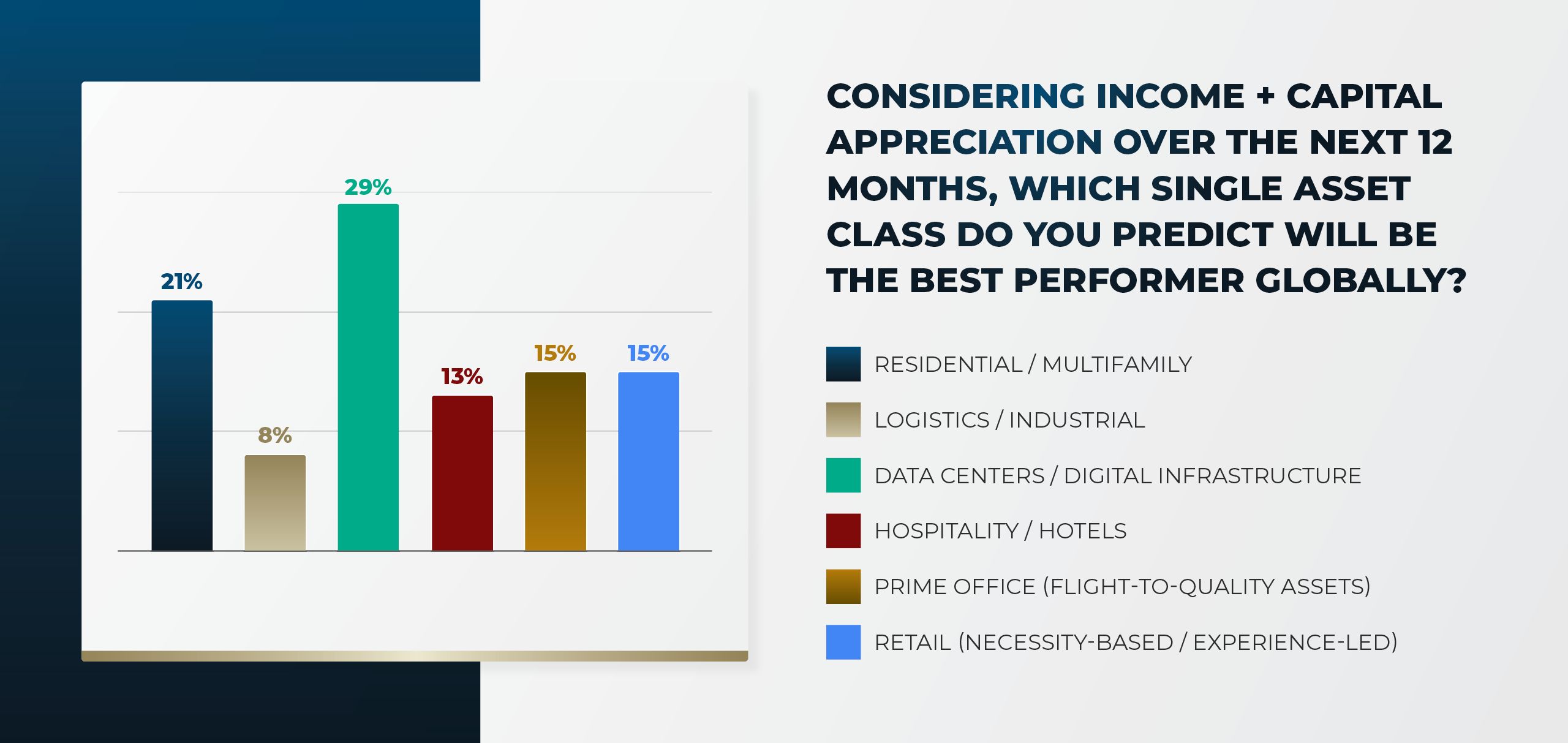

Considering income + capital appreciation over the next 12 months, which single asset class do you predict will be the best performer globally?

(GRI Institute)

The results highlight an interesting shift in global investment conviction, establishing data centres and digital infrastructure as the sector expected to deliver the highest returns over the next 12 months, underscoring the powerful structural tailwinds created by AI, cloud computing, and massive data consumption.

This shows investors are prioritising high-growth, long-lease, and inflation-linked digital infrastructure over traditional real estate.

Residential and multifamily (21%) hold a strong second place, reinforcing their perception as a core, defensive asset class driven by demographic fundamentals globally.

The similar weight given to prime office (15%) and retail (15%) suggests that capital is highly selective. Investors believe that only the most superior office assets or highly defensive, experience-led / necessity-based retail will thrive, leaving no room for mid-tier or obsolete assets.

The surprisingly low ranking of logistics and industrial (8%) suggests that while it remains a strong sector, investors believe the period of exceptional returns (post-e-commerce boom) may be softening, or that the yields on these assets have compressed too far to be the best performer compared to the growth potential of data centres.

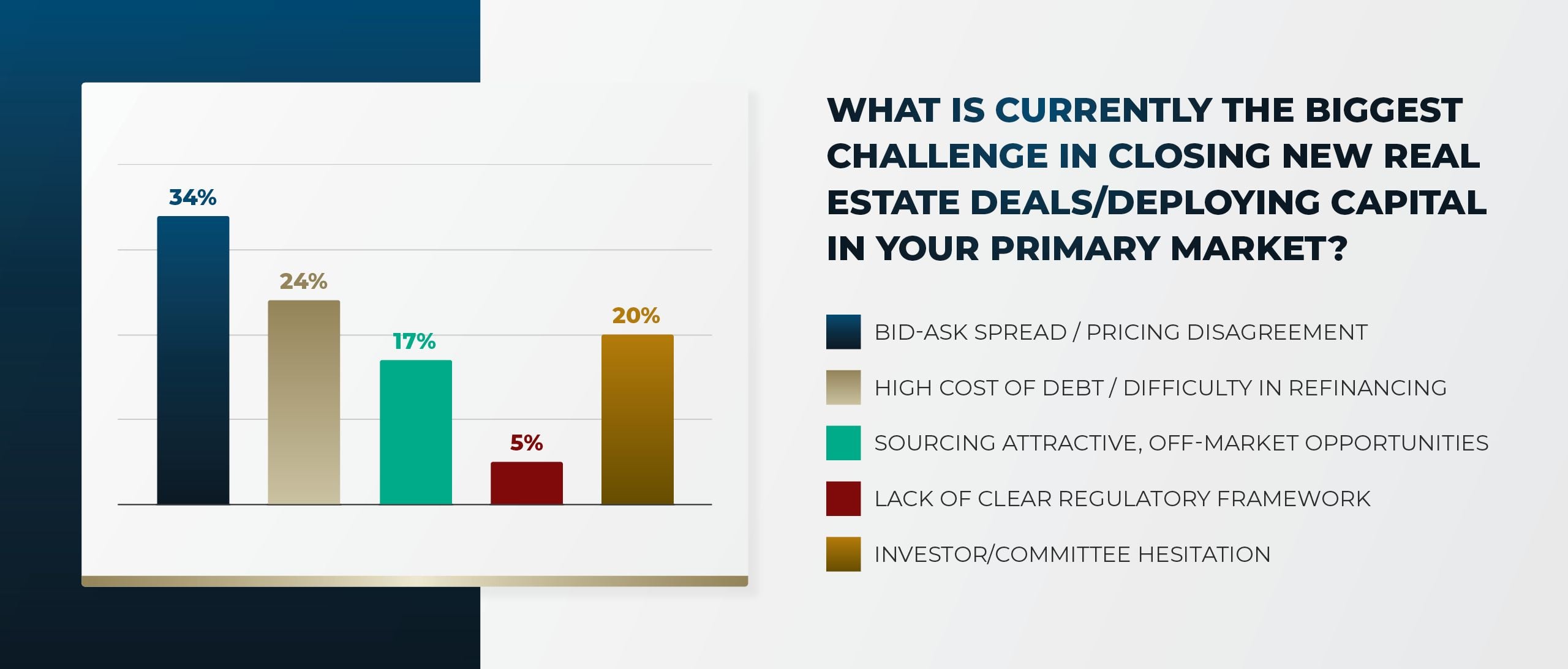

What is currently the biggest challenge in closing new real estate deals / deploying capital in your primary market?

(GRI Institute)

The results clearly establish that the primary impediment to transaction volume is pricing misalignment, followed by the cost of capital.

The bid-ask spread (34%) is the single greatest challenge. This indicates that despite the high capital appetite seen in the third question, sellers' price expectations have not yet fully adjusted to the new interest rate environment and higher cost of capital. This gap is freezing liquidity.

High cost of debt (24%) is the second major factor. This is a direct measure of the ongoing impact of elevated interest rates, affecting both new deal underwriting and the refinancing of maturing loans.

The combination of investor / committee hesitation (20%) and the difficulty in sourcing attractive opportunities (17%) shows that capital is being deployed slowly. Investors are selective, demanding a higher risk premium for the uncertainty, and are struggling to find truly compelling deals that meet their return hurdles in an efficient market.

The low response for lack of clear regulatory framework (5%) suggests that, for this sophisticated global audience, macro-financial factors far outweigh localised regulatory concerns as a barrier to entry.

Which single macroeconomic or structural factor poses the greatest long-term risk to global real estate returns over the next 3-5 years?

(GRI Institute)

The results emphatically position geopolitical instability as the single most critical long-term concern for global real estate returns, with 40% of global leaders viewing it as the paramount long-term risk, surpassing immediate financial and structural concerns.

This reflects the audience's exposure to cross-border capital flows and recognises that macro-political fragmentation and conflict pose a fundamental threat to market stability, trade, and investor confidence - a risk far beyond property fundamentals.

Persistent high cost of capital (27%) secures the second position. Investors recognise that even with the stabilisation of rates, the era of ultra-low, zero-cost debt may be over, making capital costs a permanent structural constraint on valuation and underwriting going forward.

Regulatory changes (19%) and obsolescence risk (13%) are significant, yet secondary. This indicates that while localised policies (taxation, rent control) pose specific threats, the market currently perceives them as less pervasive than macro-finance or geopolitics.

Furthermore, while ESG is critical, its immediate impact as a risk factor is currently rated lower than the cost of capital or political instability.

Which will be the best regions to invest in over the next three years?

(GRI Institute)

The global real estate market sentiment points to Europe as the top investment region for the next three years (36%), driven by the belief that the market has repriced and is now an attractive entry point, supported by expected ECB interest rate cuts and strong rental growth potential from supply shortages.

The second tier is divided between the GCC countries (23%), which appeal due to government-backed mega-projects and significant wealth inflow, and the USA (21%), where sentiment is tempered by a potentially higher-for-longer interest rate environment.

Overall, investors are prioritising markets offering either a cyclical recovery (Europe) or structural, rapid growth (GCC), while regions like Central and Latin America receive minimal attention (2%) due to perceived higher risks.

Chairmen’s Conclusions

The results from the GRI Global Chairmen's Retreat 2025 highlight a pivotal moment for the global real estate market, where optimism is rising alongside significant challenges. Geopolitical instability has emerged as a dominant concern, shaping capital deployment strategies, while sectors like digital infrastructure are seen as key growth areas.Looking ahead, real estate leaders must balance cautious optimism with strategic investments in high-growth sectors, particularly in regions poised for cyclical recovery or rapid development, while remaining agile in response to geopolitical and economic shifts that could impact long-term stability.

Discover more insights from the GRI Global Chairmen’s Retreat in our full report.