Credit: Freepik

Credit: FreepikConfidence in the global real estate market signals a capital deployment cycle

The official report revealing insider insights from the world's most respected real estate leaders at the Global Chairmen's Retreat 2025 in Abu Dhabi

Executive Summary

Key Takeaways

- A large majority (79%) of global real estate leaders plan to increase their firm's investment volume over the next 12-18 months, indicating market confidence and a capital deployment cycle.

- A liquidity bottleneck is being caused by a trillion dollars' worth of assets trapped in closed-ended funds due to their mandated or upcoming liquidation, requiring the return of core capital, possibly from new sources like 401(k) buyers.

- Geopolitical instability surpasses financial and structural concerns as the greatest long-term risk to global real estate returns over the next 3-5 years, while data centres are predicted to be the best-performing asset class globally over the next 12 months.

Download the PDF of this 'GRI Global Chairmen's Retreat 2025 Spotlight' report here.

Opening Discussion

The Trillion-Dollar Liquidity Challenge

A critical issue dominating the industry is the need to address a trillion dollars' worth of assets trapped in closed-ended funds. These funds must liquidate, with many having been due to do so over the last 36 months or scheduled to do so over the next 24 months, creating a massive liquidity bottleneck that needs to be resolved for the market to move forward.The solution hinges on the return of core capital to buy these fixed-up, broken assets. New sources of core capital, such as the potential opening up of 401(k) buyers in the US to private investments, are seen as key.

Investors are now reportedly shifting their perspective towards seeking less volatile, longer-term core and core-plus returns for inflation hedging and cash flow.

Discounts and Secondary Market Opportunities

The market is presenting significant buying opportunities due to high discounts and the slow unwinding of old funds. One major investment group, for example, reported deploying capital at a 25-30% discount on their fifth fund, even on quality assets, providing early double-digit unlevered discounts.However, there is a bifurcation in the secondary core fund market. Funds seen as well-constructed or appropriately marked trade at small discounts (2-5%), while those with market disruption or questionable marks are trading at 25% discounts.

It is also believed that the US core market is currently overvalued by a minimum of 8-10 points. Investors are advised that in this environment, information is king, requiring rigorous due diligence to separate good assets from bad ones.

The "Dead Mall Syndrome" and Location-Based Entertainment (LBE)

The decline of traditional malls - the "dead mall syndrome" - is driven by three main factors: the destructive impact of e-commerce (with 60% of consumers preferring online shopping); the unexpected competition from video games/virtual worlds (with the industry three times the size of global film and music combined, and one-third of US teenage gamers spending more on virtual than physical clothes); and a shift towards the “experience economy” (where almost 80% of consumers prefer spending money on experiences over products).The emerging replacement for malls is Location-Based Entertainment (LBE), a rapidly booming asset class. Examples of successful LBE include big-box attractions like TeamLab, which attracts 2.5 million visitors per year at its main Tokyo location, and smaller, mall-based concepts like Camp or Hotshack, which show extremely fast capital payback periods.

However, experienced investors demonstrate caution regarding the scalability and risk of LBE. Challenges include "fad” risk and the lack of staying power for many concepts; the difficulty in scaling concepts beyond a single blockbuster location; the risk of cannibalisation among different sites; and the need to deploy substantial capital for businesses that may fail.

Furthermore, the lease-based structure of these businesses poses a problem, as they often seek long 10-year leases which can become a major problem if the concept becomes obsolete, trapping the landlord.

A critical issue dominating the industry is the need to address a trillion dollars' worth of assets trapped in closed-ended funds. (Credit: GRI Institute)

A critical issue dominating the industry is the need to address a trillion dollars' worth of assets trapped in closed-ended funds. (Credit: GRI Institute)The Dynamics of Capital - How are Global Trends Transforming Real Estate?

Shift from Equity to Credit

Institutional investors have been adjusting their target allocations, leaning into credit, structured equity, and secondary strategies over the last 12 months, primarily to move higher up in the capital structure and manage risk. This shift was also a way to manufacture distributions during a time when monetisations and distributions of invested capital (DPI) were hard to come by.However, some expect this to be a temporary pivot, driven by better current returns from debt. As a result, investors are holding their capital in short-duration debt to achieve great returns while avoiding the uncertainty and illiquidity of equity.

A significant driver for the move toward credit and debt products is the increased focus on current income and fast, large distributions from clients. Credit products offer a more guaranteed income stream early on, which helps to offset the “J-curve” issue often associated with higher-return equity strategies which typically take longer to generate income.

This shift to income is seen as a relatively new trend, and is observed across the Gulf region. For core-plus investors, a laser focus is on immediate deployment into a seed portfolio that generates income from day one.

Bureaucracy and Market Inefficiency

Bureaucracy within investment firms creates market inefficiencies. Specifically, real estate groups often can't deal with debt products because these fall under a separate private credit or mezzanine (MES) department. This organisational structure results in a situation where the real estate team may forgo opportunities with a superior yield and a more secure position within the capital stack.This structural separation means that while a debt fund might attach at 60% and detach at 75% leverage, core equity funds have to cover the lower leverage portion of 0% to 40%. This can result in an inverted market where preferred equity prices are sometimes cheaper than debt as the equity investors lack the mandate to pursue debt instruments.

Artificial Intelligence (AI) in Investment and Operations

AI is rapidly becoming integrated into the investment process, with some major firms reporting the proposal to have an AI agent present in the investment committee (IC) by the end of 2025. This AI agent can process due diligence and third-party data quickly, offering real-time insights and risk commentary during IC meetings.AI is also being used to identify key markets by crunching massive demographic data sets (population, income, housing stock) with less bias than humans, allowing investors to buy assets ahead of trends.

Furthermore, AI is revolutionising operations by allowing for the collection of minuscule but valuable data to run optimisation equations for services and maintenance.

Macro-Outlook on Inflation and Interest Rates

Many market players believe that over the next 5-7 years, there will be lower central bank rates but higher inflation, based on the idea that inflation is required to distribute the financial burdens and manage the global government debt crisis. This combination of low interest rates and high inflation is viewed as advantageous for real estate, spurring rental growth while capital remains inexpensive.Countering this, others note that the disinflationary impact of AI and increased labour productivity - similar to the 1990s tech boom - could allow for low inflation growth.

Leo Machado, Partner & Managing Director GCC at the GRI Institute, addresses global real estate market leaders at the Global Chairmen’s Retreat 2025. (Credit: GRI Institute)

Leo Machado, Partner & Managing Director GCC at the GRI Institute, addresses global real estate market leaders at the Global Chairmen’s Retreat 2025. (Credit: GRI Institute)Asset Class Shake-Up - Who’s Leading, Who’s Lagging in Tomorrow’s Real Estate Markets?

Bifurcation and Premiumisation of the Office Market

The office market is experiencing a significant divide, or bifurcation, between high-quality class-A assets and older, lower-quality class-B/C stock.Best-in-class, amenitised buildings in prime locations are commanding extraordinary rent growth and high occupancy, as tenants are willing to pay top prices for vibrant spaces to draw employees back to work.

A prime office location must provide a superior employee experience. Employees, especially in markets with low unemployment, are choosing workplaces based on the proximity of shops, restaurants, bars, and social activities.

The location's ability to offer a vibrant, post-work social life is key to employee retention and attracting talent, even overshadowing the internal quality of the building itself. This focus on a broader lifestyle is leading to a preference for central business districts (CBDs) or well-connected areas with external entertainment infrastructure.

Conversely, there is a large overhang of older, vacant office space that is being repurposed, converted to residential housing, or simply torn down, particularly in suburban US markets.

Office-to-Residential Conversion Trend

There is a huge, ongoing need for housing in most cities globally, making the conversion of obsolete commercial properties a primary solution.In the US, particularly in suburban markets, older office buildings are being emptied and torn down to be replaced by residential housing, often with a good land basis.

While it is generally considered easier to get commercial properties converted to housing in the US, European jurisdictions face significant complications due to stringent regulations, zoning restrictions, and the high cost imposed by affordable housing requirements.

AI Impact on Office Demand

A major, albeit speculative, concern in the office market is the long-term negative impact of AI on the demand for office space.Participants noted that entry-level work performed by junior staff is the most susceptible to being replaced by AI. This raises a philosophical dilemma about how new professionals will gain experience, potentially leading to a substantial shrinking of the commoditised workforce.

While AI is expected to increase the productivity and value of higher-level employees, who will demand the best workspaces, the overall effect on the real estate footprint for mass-market jobs is a significant, unsolved threat.

Localised Investment Strategies and Mixed-Use Developments

There is a strong argument against the top-down, broad-brush approach often taken by institutional capital which categorically avoids entire asset classes such as office or retail.Many market players advocate for a micro-market approach, arguing that success depends on the specific market, the quality of the asset, and the quality of the local operating partner.

Furthermore, the best investment model for the future will be mixed-use developments, combining retail, office, and various forms of housing (student, serviced, residential) in one controlled area to create an active, thriving community that leverages the desire for social interaction and entertainment infrastructure.

Global Interest Rate Shifts - What’s Next for Real Estate Strategy and Capital?

The Shift from Monetary to Fiscal Dominance

The global economy has shifted from a regime dominated by monetary policy (2009–2020) to one of fiscal dominance.This change means that government spending and policy are now the primary drivers of economic support and growth, particularly in the US, benefiting from measures like the long-term budget bill. This fiscal activism is an extra factor that central banks, and thus monetary policy, must now account for.

The goal of this new policy regime is often framed as creating economic resilience and self-reliance, even if it is productivity-inefficient, as seen in the US under President Trump's tariff policies.

High and Volatile Inflation Environment

The confluence of concentrated growth in specific sectors, supply chain disruptions (exacerbated by tariffs), and increased fiscal activism, is likely to lead to higher and more volatile inflation.This volatility increases the inflation risk premium on holding non-bonds, suggesting that while the US Federal Reserve is expected to cut the Fed funds rate, bond yields may not fall to such an extent, leading to a flattening or steeping of the yield curve, thus creating greater uncertainty, particularly regarding the short end of the interest rate curve.

Interest Rate Strategy: Floating vs. Fixed Debt

A significant shift has occurred in the relative attractiveness of floating versus fixed-rate debt, particularly in the US multifamily real estate sector.Floating rate debt, particularly between 2011 and 2022, was highly advantageous, offering a significantly lower index (0.5%) compared to the 7-year Treasury (2.1%), along with superior prepayment flexibility.

However, the calculus has changed dramatically, with the current fixed rate (~5.25% for multifamily) now lower than the floating rate (~5.85%).

Due to this new financial landscape, a number of firms report changing their preference to favour fixed-rate debt as a strategy to lessen the risk and uncertainty caused by fluctuations in short-term interest rates.

US Exceptionalism

The United States is expected to continue exhibiting "US exceptionalism," growing faster than the rest of the developed world. This expansion is primarily fuelled by two key elements: fiscal stimulus resulting from a major budget act that will provide tax rebates to households, and substantial investment in AI.It is estimated that AI investment, including data centres, contributes around two-thirds of the current growth in the US. However, this boom is concentrated, raising concerns about its long-term sustainability and the risk of a market correction, as high-tech investment has returned to dot-com bubble levels.

European Core Capital Bottleneck

The European real estate market faces challenges due to a lack of core capital. This is partly due to alternative opportunities, such as Meta-backed bonds, which offer attractive yields making core real estate investment less appealing on a relative basis.This environment has created a disconnect between public market valuations and private market values. The current market is characterised as having very few buyers, implying that the smooth absorption of large asset sales would be challenging.

As a result of this deficit in conventional core capital, it has been noted that private credit has effectively taken on the role of the new core capital.

Equity and Debt - Will Capital Structures Define Real Estate’s Next Triumph?

Robust and Competitive Debt Market Conditions

The current debt market is highly liquid and widely accessible. Spreads are exceptionally narrow, even with elevated absolute interest rates. This environment fosters intense competition amongst lenders based on price.Issuance volumes, particularly in the Commercial Mortgage-Backed Securities (CMBS) sector, are strong, serving as a metric that the market is fully operational. Furthermore, reduced loan-to-value (LTV) ratios are creating significant opportunities for providers of gap capital, such as mezzanine and preferred equity, to bridge the financing needs.

European Non-Bank Lending

Europe's debt landscape is experiencing a fundamental change, moving away from its historically "over-banked" structure. The withdrawal of traditional banks, partly due to new regulations like Basel III and market stress, has opened the door for alternative lenders.Banks are increasingly disposed to provide lower-leverage senior funding, typically around 45-50% LTV, and collaborate with non-bank partners, given the superior capital efficiency of this strategy.

This shift allows non-bank entities to profitably bridge the difference in the capital stack, an approach that is further bolstered by the growing availability of institutional credit from insurance companies.

Real Estate and Corporate Private Credit Risk

There is a strong line between real estate credit and corporate private credit, with notable differences in risk profiles. The growth in corporate non-bank lending has far outpaced that of real estate non-bank lending, which potentially strains underwriting diligence.Meanwhile, real estate debt offers distinct advantages by being collateralised against tangible, hard assets, thereby streamlining the underwriting process and mitigating fraud risks far more readily than the evaluation of a corporate business plan.

Additionally, during economic downturns, real estate has historically demonstrated better recovery rates, generally exceeding 60%, a notable improvement over the sub-50% recovery figures often seen on the corporate debt side.

Delayed Pricing Correction

A significant factor preventing clear pricing is the behaviour of lenders. Unlike regulated banks which were forced to acknowledge losses and sell assets, many non-bank lenders are engaging in "extending and pretending" to delay distressed asset recognition. This practice is preventing true price correction, leaving existing capital structures effectively frozen.Consequently, current stakeholders, whether senior lenders or equity holders, frequently remain invested out of necessity, accepting returns that deviate from those expected in a free-market transaction. This scarcity of clean, arm's-length transactions is holding back market visibility.

Europe's debt landscape is experiencing a fundamental change, moving away from its historically "over-banked" structure. (Credit: GRI Institute)

Europe's debt landscape is experiencing a fundamental change, moving away from its historically "over-banked" structure. (Credit: GRI Institute)Day Conclusions

AI in Investment and Business Operations

Real estate industry leaders hold great enthusiasm for the capability of AI to process vast data sets rapidly, reducing biases typically associated with human review. This technology is not just a support mechanism for investment committees (IC) but is increasingly taking on the role of an IC itself.AI tools are already capable of reviewing fiduciary materials and providing real-time feedback by listening to the committee’s discussions and simulating its own investment committee view.

Day-to-day operations are also seeing significant productivity enhancements, with AI handling accounting functions, analysing lease agreements for due diligence, and dramatically reducing the time needed to produce IT memos.

However, the industry must carefully navigate regulatory questions concerning data deployment, particularly when entering sensitive documents, such as NDAs, into these AI systems.

The Office Sector and the Search for Alternative Uses

While industrial logistics, traditionally a primary discussion point, was surprisingly absent from discussions among real estate leaders, the office sector dominated, maintaining its statistical position as the largest real estate sector.The clear consensus is that the highest quality, best-in-class, and well-located assets continue to perform exceptionally well, attracting people irrespective of their employer. Conversely, regional offices face severe challenges, prompting an urgent focus on alternative uses.

The US market, in particular, has a negative reputation, with some estimating a 20-30% reduction in office stock, driving opportunistic shifts towards converting buildings into data centres, residential units, or entertainment assets.

This move is supported by a belief that real estate's value lies in the occupier experience, leading to the use of AI to optimise hospitality protocols and create more attractive, seamless experiences within spaces.

Credit, Private Capital, and Price Discovery

The credit markets are perceived to be in phenomenal shape, described as being at an all-time peak with very tight spreads. This flood of capital has been driven by private credit funds stepping in to fill the gap left by banks reducing their real estate credit appetite.This dynamic has created significant opportunities in filling the capital stack, specifically through mezzanine, preferred equity, and financing for development projects.

However, the market still faces a challenge in the repricing cycle, with a protracted period of adjustment expected rather than a severe downturn. This is exacerbated by a significant bid-ask spread, particularly in Europe, and the difficulty in underwriting office assets.

Ultimately, the reluctance of LPs to deploy additional equity is seen as a key impediment to new transactions and allowing the industry to fully recover.

Global Economic Order and US Exceptionalism

The global economy is shifting towards a new framework that prioritises resilience over pure cost efficiency. This transition is strengthening the role of fiscal policy and contributing to greater inflation volatility, as governments expand spending to support industrial, energy and supply-chain security. In the US, persistent and elevated fiscal deficits further reinforce the influence of fiscal policy relative to monetary policy.US exceptionalism is expected to continue, largely underpinned by sustained government support and the AI boom, which accounts for a substantial portion of the country's economic growth. The baseline forecast predicts continued growth for the next year, with a diminished risk of recession, and expectations include three further Fed rate cuts, with the first likely starting in March 2026.

Meanwhile, the focus on national security and reshoring manufacturing in critical areas like AI, chips, and pharmaceuticals is expected to increase costs and further drive inflation.

Emerging Asset Classes and Investment Structures

The consensus suggests a need to look beyond traditional real estate sectors toward more specialist and niche asset classes. An emphasis was placed on social and entertainment infrastructure as a new growth driver, as people continue to seek opportunities to socialise.While assets like beds and sheds (residential, senior living, and logistics) remain attractive due to favourable demographics, data centres are also a prominent sector of interest.

However, investors demonstrate an element of skepticism due to the ever-shortening economic lifespan of these assets, requiring constant technology upgrades and a balance between obsolescence and returns.

Meanwhile, the greater openness of lenders to cross-asset class investment is allowing for the development of more creative and unique financial stacks and structures to match these evolving opportunities.

The consensus suggests a need to look beyond traditional real estate sectors toward more specialist and niche asset classes. (Credit: GRI Institute)

The consensus suggests a need to look beyond traditional real estate sectors toward more specialist and niche asset classes. (Credit: GRI Institute)

The survey which took place at the GRI Global Chairmen's Retreat 2025 in November in Abu Dhabi, among the world’s most respected real estate market players, involved a comprehensive set of questions covering crucial areas ranging from immediate industry health and chief investor anxieties, to strategic capital deployment intentions over the next 12 to 18 months.

The collective expertise and strategic outlook from these industry leaders are revealed in the following section in the form of the full survey results and analysis.

The insights herein offer an indispensable barometer for understanding current market dynamics and informing forward-looking real estate investment strategies.

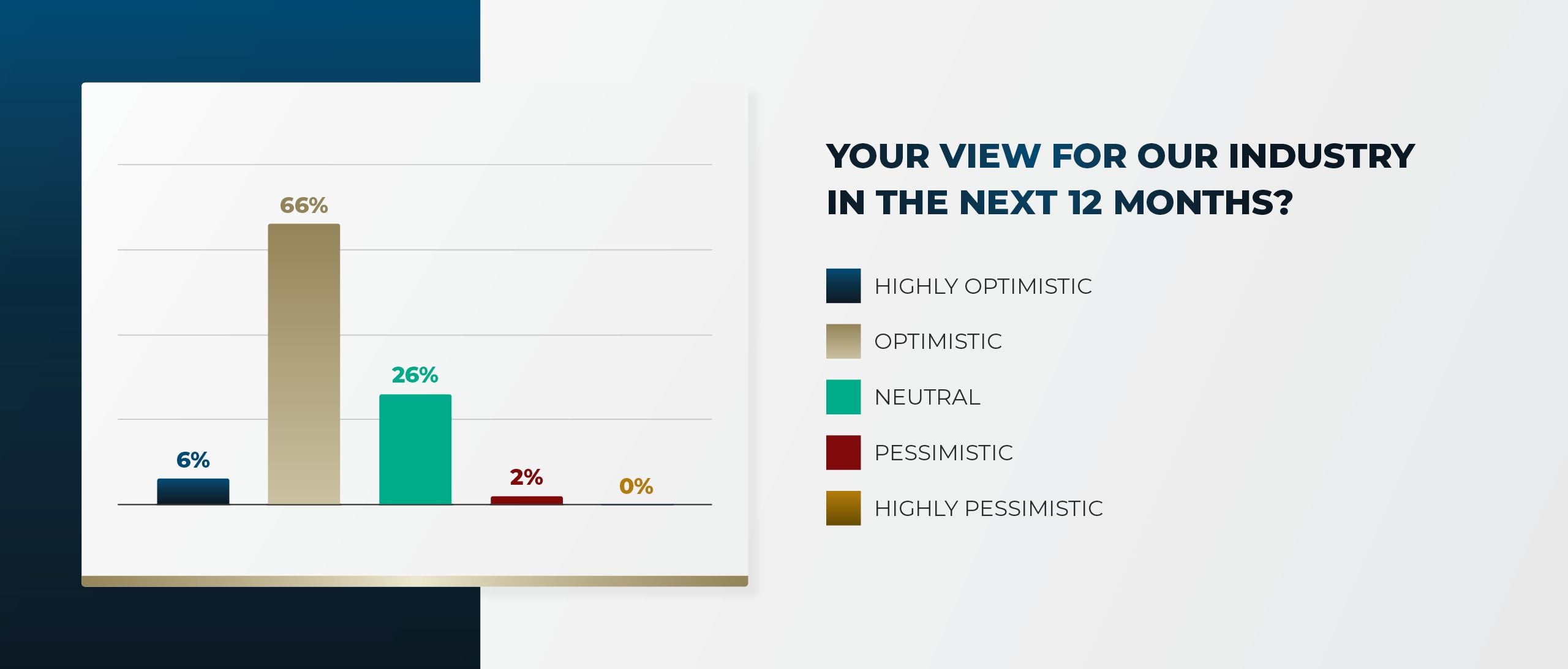

What is your view for our industry in the next 12 months?

The global real estate sentiment among industry leaders experienced a profound positive shift since the previous survey that took place in January 2025 at the Chairmen’s Retreat 2025 in St Moritz.

When compared with the most recent survey from November 2025 at the Global Chairmen’s Retreat 2025 in Abu Dhabi, the combined net optimism (highly optimistic and optimistic views) surged from 60% to 72%, while net pessimism (pessimistic and highly pessimistic views) dropped from 13% to a mere 2%. This remarkable change signals a transition from cautious optimism to stronger confidence.

The vast majority of respondents who held pessimistic views in January 2025 shifted into the optimistic camp by November 2025. The neutral view remained relatively stable among respondents, only dropping 1%, suggesting the shift was primarily from the formerly pessimistic players moving into the optimistic camp.

The shift in sentiment between January and November 2025 likely reflects a growing conviction that the global real estate market has reached or passed its bottom and is entering a recovery phase.

This optimism is generally supported by several improving market environment and macro factors observed throughout 2025, including interest rate stabilisation and improved capital accessibility.

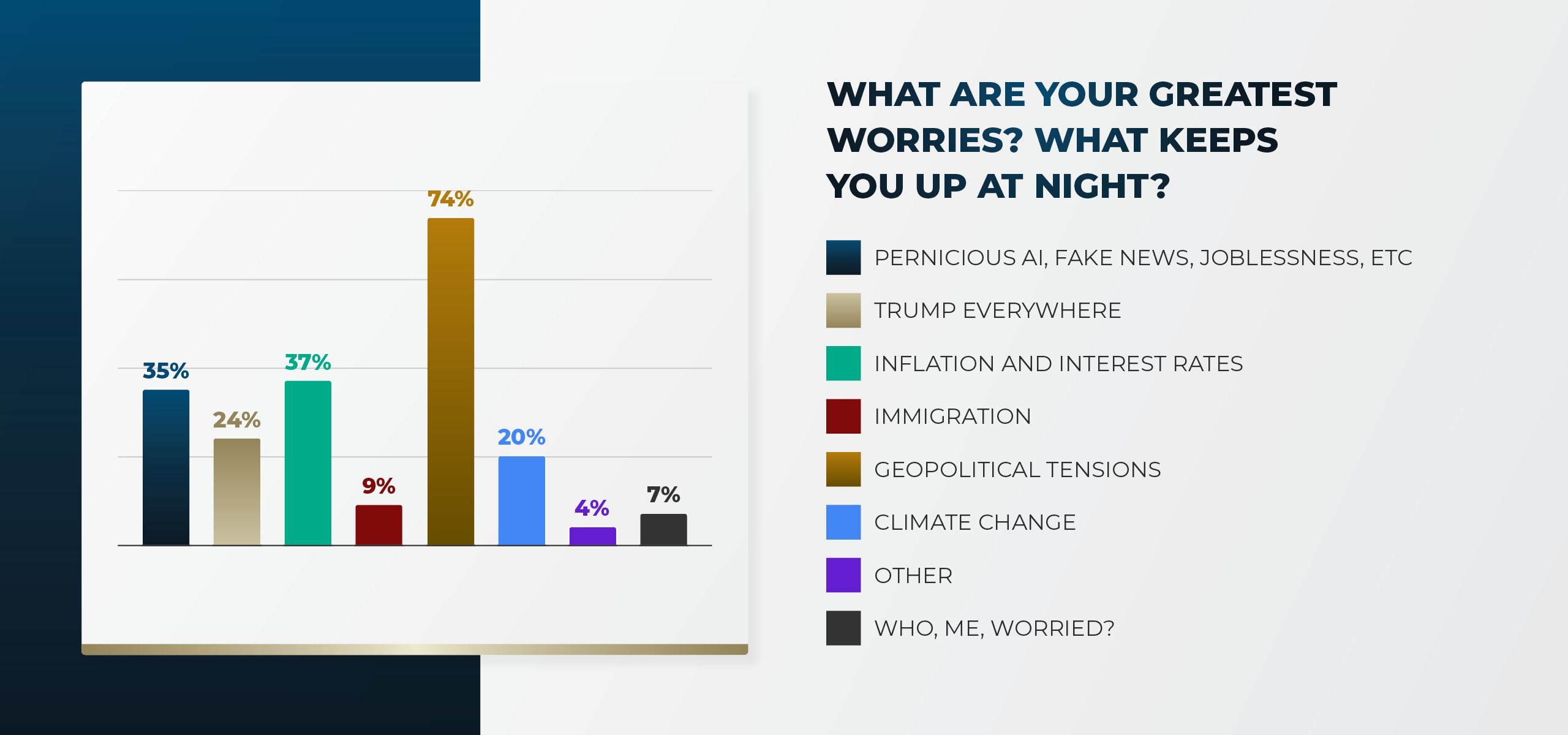

What are your greatest worries? What keeps you up at night?

The greatest worries for global real estate leaders underwent a fundamental shift in 2025, moving decisively from economic anxiety to geopolitical concerns.

When reviewing the survey results from the Chairmen’s Retreat 2025 in January in St Moritz, inflation and interest rates were the chief concern at 55%, reflecting the immediate pressure of high debt costs and central bank policy uncertainty on the real estate sector.

However, this worry has significantly retreated to 37%, following results from the Global Chairmen’s Retreat 2025 in November in Abu Dhabi, suggesting the market has seen a peak in the rate cycle while also successfully adjusting to the overall higher cost of capital.

Simultaneously, anxieties related to geopolitical tensions (including conflicts and security concerns) have surged substantially from 40% to become the dominant worry at 74%, indicating that escalating global conflicts and geo-economic fragmentation now supersede financial concerns as the most immediate threat to market stability and international investment flows.

This pivot reflects a year of increasing global volatility, likely driven by escalating international conflicts, rising US-China trade tensions, and sustained US domestic political uncertainty (which held steady at 24%).

The data suggests that while the real estate industry is finding its footing amid a new monetary policy landscape, its focus has been entirely captured by the growing threat of global instability, which now dictates capital allocation, risk assessment, and long-term planning more than other macro factors.

How do you anticipate your firm's real estate investment volume will change over the next 12-18 months compared to the previous period?

The results indicate a highly active and confident market sentiment among global real estate market players, pointing to a strong cycle of capital deployment.

A formidable total of 79% of respondents plan to increase their investment volume, suggesting that global capital has overcome recent uncertainties and is actively moving off the sidelines.

The most telling figure is that almost half (46%) anticipate a significant increase of more than 20% in investment volume. This signals that investors are not merely maintaining activity but are seeking to unlock dry powder at scale, aiming to capitalise on pricing dislocations and opportunities created by the higher interest rate environment.

The minimal share (4%) predicting any decrease underscores high confidence in the long-term fundamentals and resilience of the global real estate sector. The primary challenge moving forward will be securing quality assets amid high liquidity.

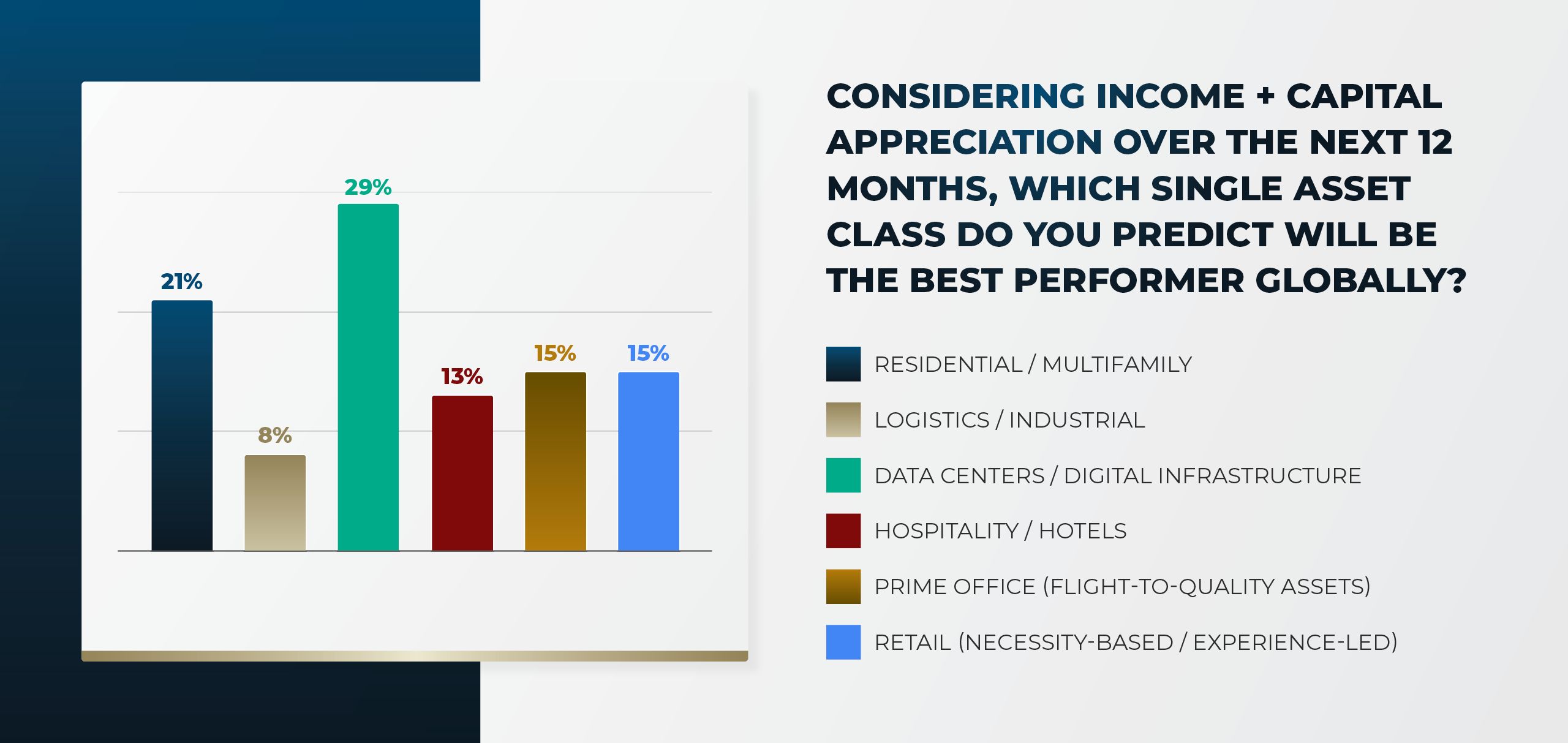

Considering income + capital appreciation over the next 12 months, which single asset class do you predict will be the best performer globally?

The results highlight an interesting shift in global investment conviction, establishing data centres and digital infrastructure as the sector expected to deliver the highest returns over the next 12 months, underscoring the powerful structural tailwinds created by AI, cloud computing, and massive data consumption.

This shows investors are prioritising high-growth, long-lease, and inflation-linked digital infrastructure over traditional real estate.

Residential and multifamily (21%) hold a strong second place, reinforcing their perception as a core, defensive asset class driven by demographic fundamentals globally.

The similar weight given to prime office (15%) and retail (15%) suggests that capital is highly selective. Investors believe that only the most superior office assets or highly defensive, experience-led / necessity-based retail will thrive, leaving no room for mid-tier or obsolete assets.

The surprisingly low ranking of logistics and industrial (8%) suggests that while it remains a strong sector, investors believe the period of exceptional returns (post-e-commerce boom) may be softening, or that the yields on these assets have compressed too far to be the best performer compared to the growth potential of data centres.

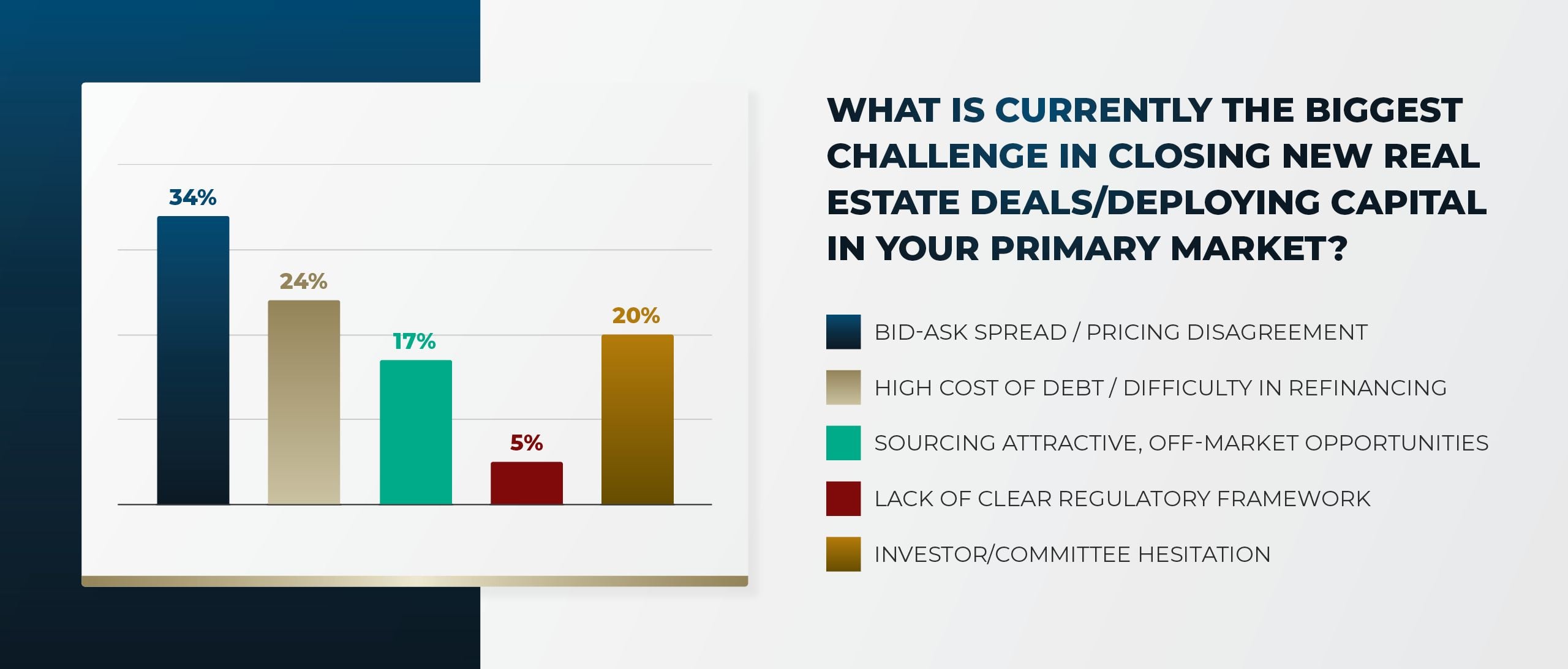

What is currently the biggest challenge in closing new real estate deals / deploying capital in your primary market?

The results clearly establish that the primary impediment to transaction volume is pricing misalignment, followed by the cost of capital.

The bid-ask spread (34%) is the single greatest challenge. This indicates that despite the high capital appetite seen in the third question, sellers' price expectations have not yet fully adjusted to the new interest rate environment and higher cost of capital. This gap is freezing liquidity.

High cost of debt (24%) is the second major factor. This is a direct measure of the ongoing impact of elevated interest rates, affecting both new deal underwriting and the refinancing of maturing loans.

The combination of investor / committee hesitation (20%) and the difficulty in sourcing attractive opportunities (17%) shows that capital is being deployed slowly. Investors are selective, demanding a higher risk premium for the uncertainty, and are struggling to find truly compelling deals that meet their return hurdles in an efficient market.

The low response for lack of clear regulatory framework (5%) suggests that, for this sophisticated global audience, macro-financial factors far outweigh localised regulatory concerns as a barrier to entry.

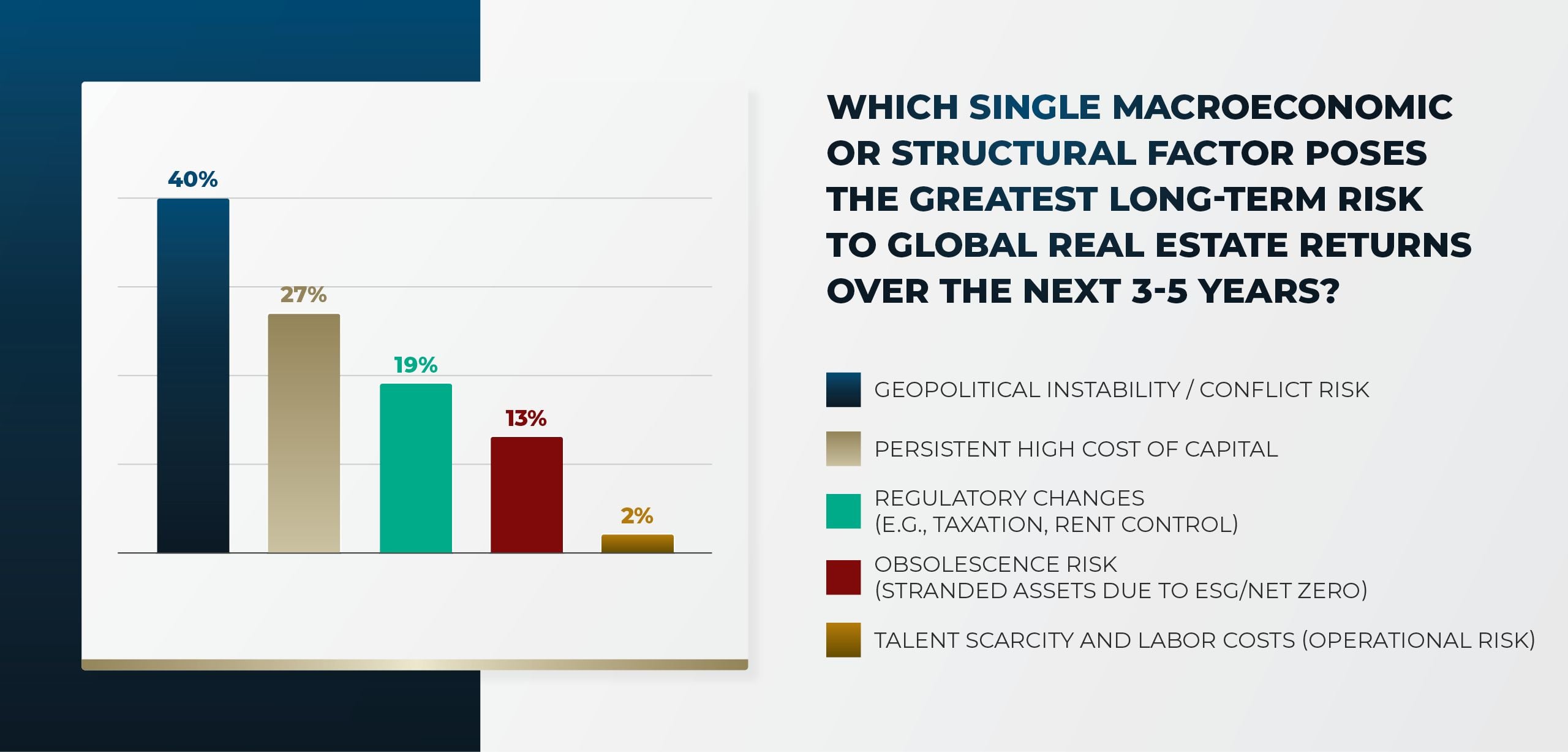

Which single macroeconomic or structural factor poses the greatest long-term risk to global real estate returns over the next 3-5 years?

The results emphatically position geopolitical instability as the single most critical long-term concern for global real estate returns, with 40% of global leaders viewing it as the paramount long-term risk, surpassing immediate financial and structural concerns.

This reflects the audience's exposure to cross-border capital flows and recognises that macro-political fragmentation and conflict pose a fundamental threat to market stability, trade, and investor confidence - a risk far beyond property fundamentals.

Persistent high cost of capital (27%) secures the second position. Investors recognise that even with the stabilisation of rates, the era of ultra-low, zero-cost debt may be over, making capital costs a permanent structural constraint on valuation and underwriting going forward.

Regulatory changes (19%) and obsolescence risk (13%) are significant, yet secondary. This indicates that while localised policies (taxation, rent control) pose specific threats, the market currently perceives them as less pervasive than macro-finance or geopolitics.

Furthermore, while ESG is critical, its immediate impact as a risk factor is currently rated lower than the cost of capital or political instability.

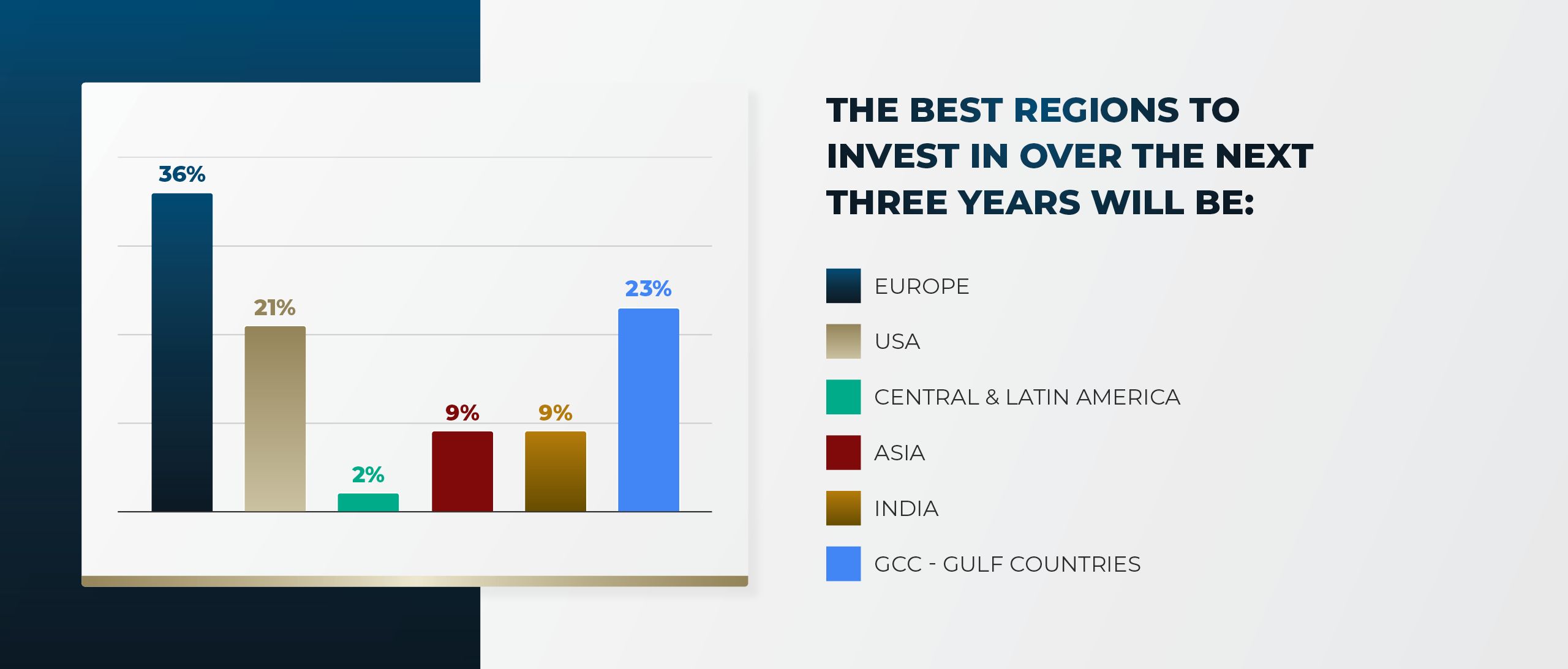

Which will be the best regions to invest in over the next three years?

The global real estate market sentiment points to Europe as the top investment region for the next three years (36%), driven by the belief that the market has repriced and is now an attractive entry point, supported by expected ECB interest rate cuts and strong rental growth potential from supply shortages.

The second tier is divided between the GCC countries (23%), which appeal due to government-backed mega-projects and significant wealth inflow, and the USA (21%), where sentiment is tempered by a potentially higher-for-longer interest rate environment.

Overall, investors are prioritising markets offering either a cyclical recovery (Europe) or structural, rapid growth (GCC), while regions like Central and Latin America receive minimal attention (2%) due to perceived higher risks.

Thank you to our most esteemed members who contributed their invaluable expertise to the discussions at the GRI Global Chairmen’s Retreat 2025, as well as our sponsors Affinius Capital, Pretium, CAIN, and Sculptor Capital Management for their support.

The quality and candour of the discussions cement the GRI Global Chairmen’s Retreat as the definitive meeting point for the very top tier of global real estate leadership.