Freepik

FreepikWarehousing & Logistics India Q4/2025 Market Outlook & Key Trends

Unpacking the 56% investment pivot, vertical efficiency, and the institutional drivers shaping the logistics outlook for 2026

December 9, 2025Real Estate

Written by:Jorge Aguinaga

Executive Summary

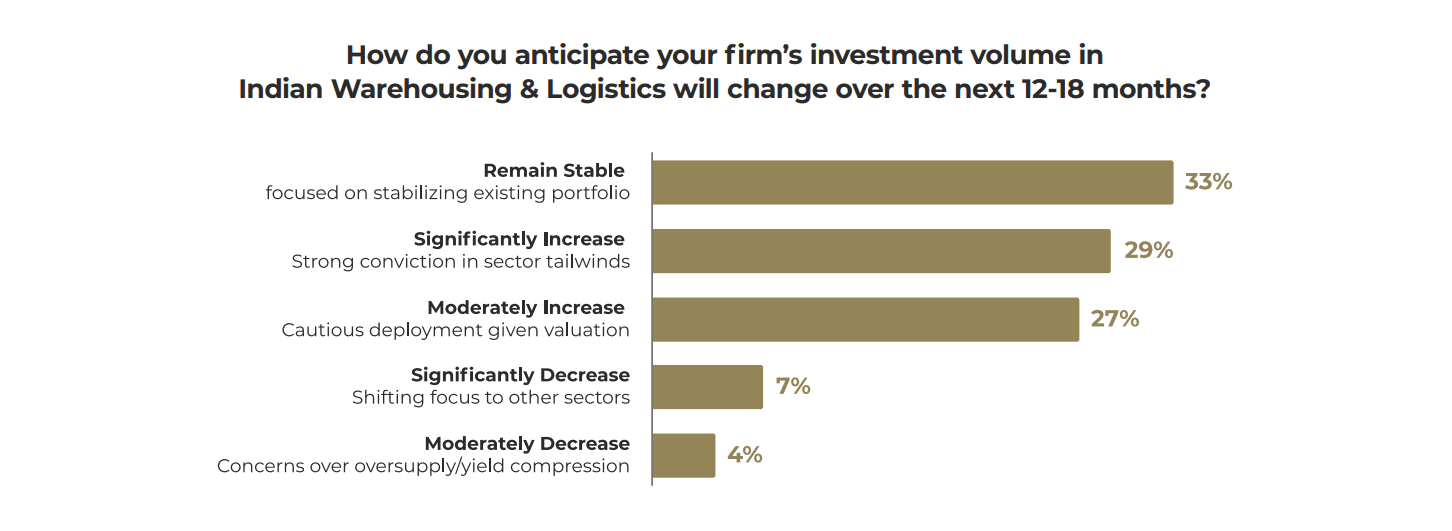

India’s warehousing and logistics sector is executing a decisive pivot from stabilised growth to aggressive expansion, with 56% of investors preparing to increase their capital deployment over the next 12 to 18 months.

This renewed optimism is driven by a structural maturity in the market, where the focus has shifted from simple capacity addition to the delivery of future-proofed, Grade A++ infrastructure capable of supporting global supply chains.

This report distils the strategic insights shared at GRI Warehousing & Logistics India 2025, exploring how the asset class has graduated to an institutional stronghold. While operational hurdles such as high fuel costs and supply chain fragmentation persist, the investment thesis is now firmly anchored in the potential for global exits.

The sector is witnessing a distinct evolution in capital strategies, moving away from domestic reliance towards public markets and foreign institutional partnerships, which now represent the dominant exit avenues for large-scale portfolios.

This renewed optimism is driven by a structural maturity in the market, where the focus has shifted from simple capacity addition to the delivery of future-proofed, Grade A++ infrastructure capable of supporting global supply chains.

This report distils the strategic insights shared at GRI Warehousing & Logistics India 2025, exploring how the asset class has graduated to an institutional stronghold. While operational hurdles such as high fuel costs and supply chain fragmentation persist, the investment thesis is now firmly anchored in the potential for global exits.

The sector is witnessing a distinct evolution in capital strategies, moving away from domestic reliance towards public markets and foreign institutional partnerships, which now represent the dominant exit avenues for large-scale portfolios.

Key Takeaways

- Aggressive expansion plans now dominate as 56% of firms prepare to increase investment, supported by a diversifying capital stack.

- To offset rising land costs, the market is actively shifting towards vertical Grade A++ ecosystems with automation readiness and multi-level truck access.

- A valuation paradox persists where location drives 49% of premium value versus just 4% for ESG, yet investors warn that sustainability is non-negotiable.

The Strategic Outlook for 2026

The Indian logistics sector has reached a critical inflection point, transitioning from a decade of foundational organisation to a phase of sophisticated institutionalisation.Unlike Western markets which matured organically through domestic consolidation, India’s growth trajectory has been distinct: institutional capital arrived before the market fully consolidated, creating a unique high-growth ecosystem that is now attracting a second wave of domestic wealth.

This structural maturity is reflected in the GRI Warehousing & Logistics India Barometer 2025/Q4, which reveals that 56% of firms are planning to significantly increase capital allocation in the coming 18 months.

High-conviction capital is driving the sector, with those planning “Significant” increases outnumbering those planning moderate growth. (GRI Institute)

However, this capital is not chasing the same box-moving assets of the past. The investment focus has narrowed sharply onto high-specification assets that can withstand the dual pressures of climate resilience and automation.

The outlook for 2026 is defined by a race for efficiency. With land valuations in key hubs like Mumbai and Delhi appreciating faster than rental yields, the traditional land banking model is obsolete.

The new imperative is asset sweating - maximising Floor Space Index (FSI) through verticality and technology to bridge the gap between soaring input costs and competitive lease rates.

Consequently, the strategic narrative for the next year is less about where to build, and more about how to build assets that remain liquid for the eventual exit into public markets, such as REITs, and global portfolios.

Fireside Chat on Warehousing in India

Drawing a distinct parallel to the evolution of European logistics hubs, a candid discussion between Norbert Sumislawski, Managing Director - International Project Management at Panattoni, and Prateek Jhawar, Managing Director and Head - Infrastructure & Real Assets at Avendus, revealed that the Indian warehousing sector is currently navigating a developmental phase comparable to where markets like Poland stood a decade ago.This maturation signals a fundamental shift away from simple capacity expansion towards a cycle defined by technical precision and adherence to global operational standards.

After completing its first decade of organised activity, the market is witnessing robust investor confidence driven by India’s expanding role as a worldwide production hub; this has established a distinct capital cycle where early institutional investment is now being bolstered by a significant influx of domestic capital.

Investment focus remains heavily concentrated on Tier-1 cities where demand trends have built a clear case for in-city warehousing, with major metropolitan areas such as Bangalore and Delhi continuing to serve as primary hubs for high-specification developments.

Alongside this geographic focus, there is a pronounced shift towards Build-to-Suit (BTS) projects as developers adapt to the specific requirements of manufacturers, moving the sector decisively beyond basic storage towards Grade A+ facilities that integrate advanced technology and sustainability features.

As automation is identified as the future of warehousing, manpower demand is expected to decrease in favour of robotics, necessitating technical upgrades such as superior floor flatness and high-capacity power cabling during the initial construction phase to avoid cost-prohibitive retrofitting.

Furthermore, due to the hot climate, the industry is seeing a growing trend towards installing HVAC and cooling systems rather than relying solely on ambient storage.

Sustainability has evolved into a dominant theme, with financing increasingly tied to ESG compliance, meaning banks and capital providers now expect assets to be not only green-certified but operationally efficient to reduce tenant costs.

Consequently, features like rainwater harvesting and solar panels are becoming standard requirements, mirroring developed markets where non-compliant buildings are illiquid - a standard rapidly becoming the norm in India where assets must be operationally green to ensure sellability.

Despite this positive outlook, a significant economic headwind is the disparity between rising land prices and rental levels which have remained relatively stagnant over the last few years, creating a challenging environment where developers must invest in future-proof specifications before rents have fully caught up.

However, there is a strong expectation that rental corrections will occur as the market matures and tenants increasingly acknowledge the value of operationally efficient, high-grade facilities.

Rising land costs and stagnant rents force developers to future-proof assets before yields catch up, shared Norbert Sumislawski in a Fireside Chat with Prateek Jhawar. (GRI Institute)

Warehousing in India

Securing Institutional Vs. Domestic Capital Inflow, Public Market Access, and Strategies for Tenacity

While the initial phase of the Indian warehousing sector was defined by the establishment of physical infrastructure, the current narrative is increasingly dominated by a sophisticated evolution in capital structures and market financialisation.A pivotal transformation is underway regarding investment sources; whereas the industry was originally anchored almost exclusively by global institutional funds, there is now a palpable surge in domestic capital participation.

High Net-Worth Individuals (HNIs) and family offices, who previously shied away from the sector, are now demonstrating a willingness to underwrite development risks, mirroring the capital recycling trends observed in mature Asian markets including Korea, Japan, and China.

This diversification of funding is supported by a marked shift in risk perception, evidenced by the compression of cap rates from historical highs of 9% to sub-7% levels, signalling that warehousing is increasingly accepted as a stable, core asset class.

As the market matures, the focus has inevitably turned towards securing viable exit mechanisms, a component that was historically absent but is now being addressed through the emergence of InvITs and potential IPOs.

A nuanced debate persists regarding the optimal route for public listing; InvITs are generally viewed as the preferred vehicle for investors seeking the stability and consistency of yield-bearing portfolios, whereas IPOs are considered more suitable for entities that can demonstrate high-growth scalability, typically requiring immense portfolios of 15-20 million square feet to be viable.

This financial deepening is occurring alongside a redefinition of geographical strategies, where the concept of Tier-1 locations is expanding outward due to urban sprawl, simultaneously creating a compelling case for in-city warehousing to service immediate last-mile logistics (LML) requirements.

Despite this financial optimism, the sector must navigate significant headwinds, primarily the stubborn disconnect between escalating land prices - driven partly by competition from alternative asset classes like data centres and residential developments - and rental levels which have yet to fully realign with these increased input costs.

While direct competition with data centres is often limited to specific micro-markets like Panvel, the general inflation of land values necessitates that developers maximise the utility of every square inch of Floor Space Index (FSI) and explore mixed-use capabilities.

The market has ultimately transitioned from a fragmented landscape to one demanding "full-blown managers" capable of navigating complex approvals and execution risks, reinforcing that long-term value creation will rely on patient capital that appreciates the often-understated terminal value of these industrial assets.

The Future of Grade A++

New Warehousing Zones, Value-Adds, and Regulation-Backed Infrastructure

A definitive shift in asset classification is reshaping the industrial landscape, as the industry moves beyond the now-standard "Grade A+" designation towards a new tier of excellence.What was once celebrated as premium infrastructure just half a decade ago has effectively been relegated to a baseline hygiene factor, compelling the market to adopt the Grade A++ benchmark.

This elevated standard is no longer defined merely by superior physical dimensions - such as 10 to 12-metre eaves or high-tolerance flooring - but by a holistic ecosystem that integrates advanced sustainability features, automation readiness, and essential social infrastructure.

Crucially, this recalibration is driven by financial imperatives as much as operational ones; institutional investors increasingly view ESG compliance and technical future-proofing as mandatory prerequisites to ensure asset liquidity for exits after typical five-year hold periods. Without these objective standards, developments risk becoming illiquid in a market that is aggressively moving toward global institutional norms.

However, a persistent structural challenge remains the dichotomy between Grade A++ land prices and Grade B rental expectations, where input costs have surged while tenants remain price-sensitive regarding base rentals.

To counter this compression of yields, institutional developers are innovating their acquisition strategies, increasingly opting for long-term land leases of up to 30 years rather than outright purchase - a model that fundamentally differentiates them from local players who rely primarily on the capital appreciation of the land itself.

Simultaneously, developers are maximising land utility through vertical expansion, dispelling the historical myth that upper floors command significantly lower rentals; with robust ramp access designed for heavy trucking, second-floor spaces are now achieving rental parity with ground floors, effectively doubling the productive capacity of expensive land parcels.

Beyond the physical asset, the sector is witnessing a paradigm shift from traditional leasing to "Real Estate as a Service" models, where value is increasingly derived from operational integrations rather than simple square footage.

This includes exploring dynamic pricing mechanisms based on pallet positions or throughput, driven by the sophistication of 3PL operators and the need for flexibility in urban logistics.

Furthermore, social infrastructure has become a critical differentiator; following legislative changes to limits on women’s working hours to allow them to work nightshifts, premium facilities are now expected to provide comprehensive 24/7 welfare amenities, including worker housing, crèches, and safe transport, which directly impact a tenant's ability to retain labour.

From a geographic perspective, the supply-demand imbalance is forcing a rental correction in established industrial clusters. In saturated hubs like Chakan (Pune) and Chennai, where land scarcity is acute, rentals have surged significantly - in some cases from INR 20-21 to over INR 32 per square foot - as tenants are compelled to pay for quality in the absence of alternative supply.

However, the industry’s maturation is somewhat impeded by the absence of codified government regulations defining these grades, leaving a grey area where non-compliant structures compete on price with high-spec assets.

Consequently, the onus remains on institutional players to educate the market on the invisible premiums of Grade A++ development - such as high-capacity fire safety systems - which ensure long-term operational resilience and business continuity.

To offset soaring land valuations, the market is rapidly shifting towards vertical Grade A++ ecosystems where automation readiness is the new baseline for viability. (GRI Institute)

Mixed-Asset Logistics Parks

Enhanced Revenue Models, Innovation in Structures, and In-City Warehousing

The logistics landscape in India is rapidly expanding beyond traditional warehousing boxes into complex, mixed-asset ecosystems that operate on fundamentally different financial and operational models.In specialised zones such as port-based logistics parks and airports, the value equation shifts dramatically; unlike standard warehousing where rental income constitutes nearly 90% of the asset's value, specialised infrastructure sees rent contributing only about 40%, with the majority of revenue driven by throughput, connectivity, and ancillary services.

These high-barrier projects often involve long-term government leasehold structures - typically ranging from 30-60 years - where the asset's viability hinges on precise end-use definitions and concession agreements rather than freehold ownership.

A prime example of this evolution is the development of Multi-Modal Logistics Parks (MMLPs), which operate on strict revenue-share models that prohibit land sub-leasing and mandate value-added construction.

Success in these large-scale infrastructure projects is heavily dependent on external connectivity, leading developers to increasingly advocate for the inclusion of railway sidings and access roads within their own scope to mitigate the paralysing delays often caused by inter-departmental bureaucracy.

Simultaneously, the sector is witnessing an aggressive push into in-city warehousing, a nascent asset class that is redefining urban logistics far beyond the headline-grabbing quick commerce sector.

While dark stores are a visible component, the actual demand spectrum is surprisingly diverse, encompassing cloud kitchens requiring piped gas and grease traps, high-security currency chests, self-storage facilities, and even climate-controlled storage for high-value art and fashion.

To make these high-cost urban land parcels financially viable, developers are innovating structurally through vertical densification; the emerging gold standard involves integrating robust ramp systems that allow 20-foot trucks to access upper levels, effectively rendering every floor a ground floor and eliminating the 10-15% rental discount typically applied to lift-accessed spaces.

However, the exorbitant cost of urban land means that pure-play warehousing is rarely feasible in isolation, often forcing developers to adopt mixed-use strategies - blending retail, office, and hospitality - or to repurpose brownfield assets like defunct malls to make the unit economics work.

Furthermore, the pressure of rising land prices and labour costs is accelerating the transition from manual operations to sophisticated automation, particularly within the cold chain sector.

The industry is moving towards Automated Storage and Retrieval Systems (ASRS) and "pallet-in, pallet-out" models, which allow for massive vertical densification - illustrated by cases where requirements for 4 million square feet of horizontal space were consolidated into a mere 800,000 square feet by building vertically up to 14 metres.

Despite these clear efficiency gains, there remains significant tenant apprehension regarding automation, requiring developers to actively educate occupiers to shift them away from legacy specifications towards modern, tech-enabled infrastructure.

Ultimately, the sector is maturing into a collaborative environment where success is defined by the ability to integrate technology, maximise land utility through verticality, and secure diversified revenue streams beyond simple rental arbitrage.

Thank you to everyone who participated in the GRI Warehousing & Logistics India 2025 conference.