Credit: OECD & GRI Institute

Credit: OECD & GRI InstituteFuture-Proofing Real Estate: Inside the OECD’s Roadmap to COP30

GRI Institute members participated in the OECD meeting to lay the foundations for climate-resilient investment in real estate

November 5, 2025Real Estate

Written by:Rory Hickman

Key Takeaways

- GRI Institute members met the OECD in Paris to inform its COP30 roadmap for future-proofing climate-resilient real estate investment.

- Climate risks in property are material financial risks that must be embedded in investment and policy frameworks.

- Progress depends on standardised open data and coordinated public-private action for pragmatic, internationally aligned implementation.

In the lead-up to COP30 in Brazil this November, members of the GRI Institute were invited to the headquarters of the Organisation for Economic Co-operation and Development (OECD) in Paris for a roundtable discussion with the OECD Sustainable Buildings Unit.

The meeting formed part of the OECD’s broader project Future-Proofing Real Estate Investment, which seeks to bridge the gap between climate goals and market realities by integrating climate-related risks into financial and investment frameworks for the built environment.Representing the top decision-makers of the global real estate industry - CEOs, presidents, founders, and senior investment executives - GRI Institute members were invited to provide input grounded in operational, financial, and regulatory experience, reflecting the OECD’s recognition of the Institute’s membership base as an exceptional source of leadership-level insight.

GRI Institute members provided input during a roundtable discussion with the OECD Sustainable Buildings Unit ahead of COP30 in Brazil. (Credit: OECD & GRI Institute)

OECD Sustainable Buildings Unit Overview

The OECD’s Sustainable Buildings Unit has evolved significantly in recent years, moving through three major transitions:- From a local policy focus to engagement across all levels of governments.

- From addressing operational carbon to adopting a whole-life-carbon approach that includes construction materials, renovation, and demolition.

- From treating buildings as physical assets to recognising real estate as a financial asset central to climate and economic stability.

The outcomes will inform the OECD’s forthcoming report, entitled “Future-Proofing Real Estate Investment: Placed-Based Risks”, offering policy recommendations for governments. The short version of the report will be presented at COP30 in the form of Policy Highlights.

Preliminary Findings

The OECD’s work builds on frameworks from the Bank for International Settlements and the Network for Greening the Financial System. These models trace how physical risks - such as floods, heatwaves, and wildfires - and transition risks linked to policy, technology, and market shifts translate into financial risks including credit, market, operational, underwriting, and liquidity risks.The preliminary findings of the OECD’s analysis reveal some key points:

Place-Based Exposure and Systemic Impacts:

Location and design shape climate risks in real estate, with local shocks spreading into wider economic systems.Material Financial Impact:

Climate-related risks are already affecting credit ratings, asset values, insurance coverage, and liquidity; disproportionately affecting those least able to adapt.Implementation Gaps:

Risk management mechanisms exist but remain uneven; stronger coordination between prevention and finance is needed for systemic resilience.Tools and Data Gaps:

Technologies such as scenario models and hazard maps are advancing, but remain limited by the lack of harmonised, granular, asset-level data restricting place-based risk analysis and valuation.Policy Gaps and Investment Needs:

Despite progress in resilience financing and new insurance schemes, equity safeguards and comprehensive resilience strategies remain incomplete. Transformative, long-term investment is required to build resilient and low-carbon real estate.

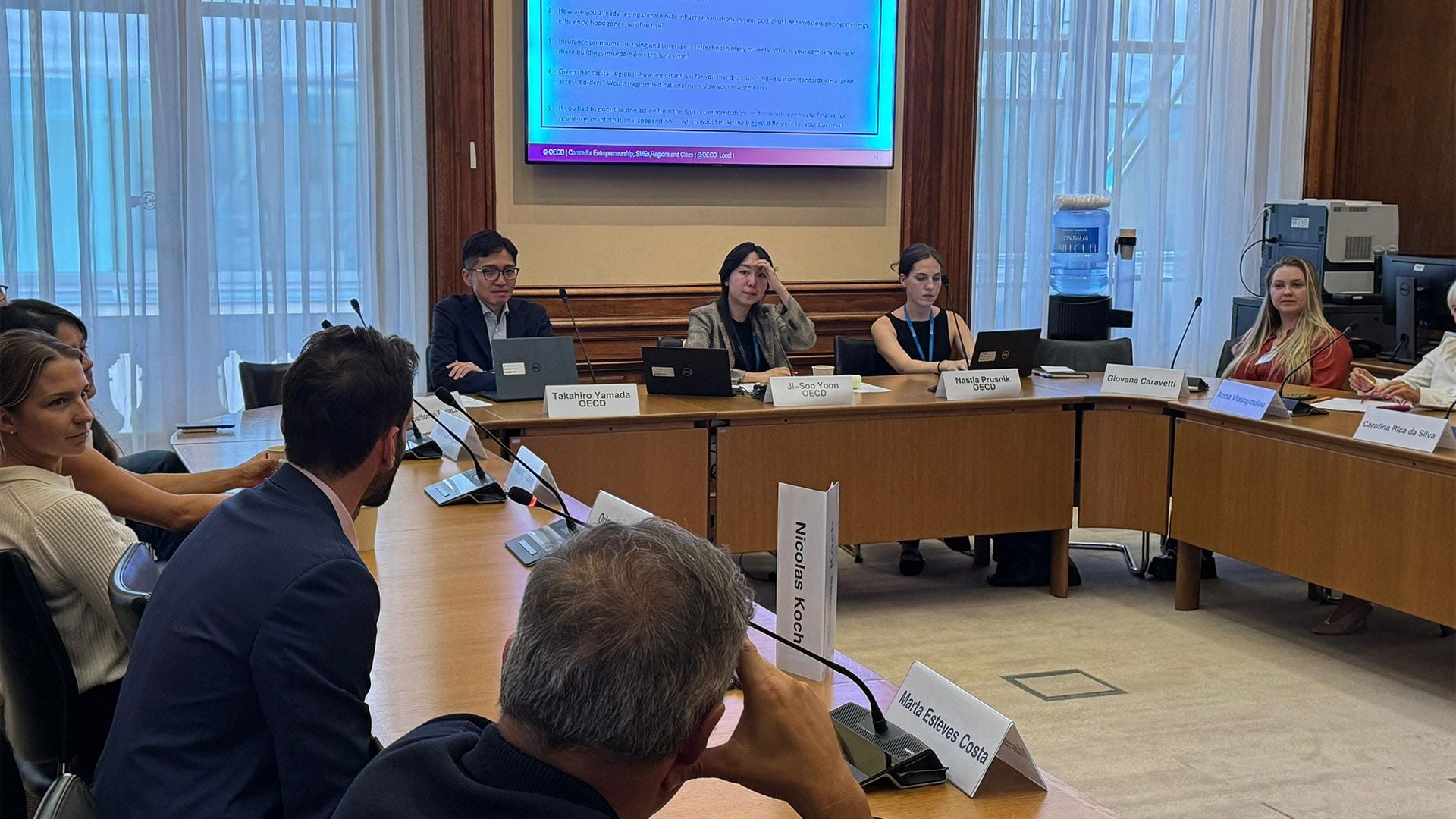

The OECD Sustainable Buildings Unit’s Ji-Soo Yoon and Takahiro Yamada led this collaborative discussion at the organisation’s Paris headquarters. (Credit: OECD & GRI Institute)

Addressing the Challenges

Challenges in Climate-Related Risks

Participants agreed that building-level disclosure is essential but complex. Much of the relevant data is held privately by investors, banks, and asset managers, creating obstacles to transparency.Some noted that without government incentives, owners may be reluctant to share sensitive information, while others cautioned that strict disclosure mandates could disadvantage regions with more advanced ESG regulations.

Need for Harmonisation

Several participants highlighted disparities across Europe. Differences in building quality, regulatory maturity, and national energy certification systems complicate comparisons and investment decisions.There was broad support for harmonised energy and risk metrics, allowing investors to assess portfolios across borders more consistently.

Data Granularity and Practical Limits

While some participants argued that only asset-level granularity can enable accurate financial risk modelling, others suggested sample-based or phased approaches would be more realistic.The debate reflected a balance between ambition and feasibility, with a shared understanding that excessive complexity could delay implementation.

Market Realities and Investment Timelines

A recurring theme was the mismatch between short-term financial horizons and long-term climate goals. Real estate investors and insurers typically operate within 3-10-year cycles, while governments legislate for 30-50-year outcomes.Participants warned that overly ambitious regulations, such as prohibiting transactions of lower-rated buildings, could lead to market shocks and devaluation, particularly for long-term holders like insurers and REITs.

Barriers to Transparency

Concerns were raised about ownership opacity, market competitiveness, and the potential devaluation of assets following public disclosure of building performance. It was noted that in some markets, unclear beneficial ownership structures and money-laundering risks further complicate transparency efforts.Top-Down vs Bottom-Up Governance

Several speakers warned against overly centralised policymaking detached from local realities. They emphasised that policy must account for regional conditions and include the perspectives of those who manage and finance assets daily.Anecdotal evidence showed how poorly tailored regulations can lead to unintended environmental and economic consequences.

Private Sector as an Agent of Change

Participants also acknowledged the role of private market leaders in driving progress, often faster than governments. Examples such as institutional investors setting their own carbon-reduction benchmarks or withdrawing capital from underperforming funds were cited as signs that market forces can accelerate sustainability transitions.OECD Recommendations

As a result of this project, the OECD plans to include the following four key recommendations for policy makers:- Avoid building in high-risk areas and make climate-related risks visible in planning and investment decisions.

- Foster a robust ecosystem of open and interoperable climate-related risk real estate data.

- Link finance to decarbonisation and resilience.

- Anchor a global framework for future-proofing real estate through international standards and risk sharing.

The OECD’s aim is to ensure that future real estate investment aligns with both economic stability and climate resilience, offering governments a roadmap supported by industry insight.

GRI Institute members’ participation provided the OECD with grounded feedback from those operating at the highest level of global property investment. Their input is expected to shape the report’s recommendations, ensuring that the policies proposed in Brazil later this year are practical, data-driven, and market-aligned.

The OECD-GRI collaboration demonstrates how cross-sector dialogue can build resilient frameworks for climate and economic goals. (Credit: OECD & GRI Institute)

Overall Takeaways

The Paris meeting underscored the urgency of integrating climate considerations into financial systems without disconnecting from the realities of the market. The discussion converged around several key takeaways:- Climate-related risks are financial risks, demanding equal attention from investors and policymakers.

- Open, standardised data remains the foundation for credible risk management and policy coherence.

- Incremental, harmonised steps are preferable to sweeping mandates that may prove unworkable.

- Coordination between stakeholders with different time horizons - governments, insurers, investors, and owners - is essential.

- Private sector leadership and local adaptation can complement, rather than compete with, regulatory initiatives.

The OECD Future-Proofing Real Estate Investment Taskforce is set to expand even after COP30. The OECD team is actively seeking more organisations and companies to join this effort.

If you are interested in participating in the OECD Future-Proofing Real Estate Investment Taskforce, please contact Ji-Soo Yoon.

Learn more about the OECD here