GRI Institute

GRI InstituteDeutsche GRI 2026 Barometer: How Germany is engineering its real estate recovery

Exclusive survey results reveal industry perspectives on price discovery, the rise of alternative living, and the necessity of hands-on asset management

May 12, 2026Real Estate

Written by:Rory Hickman

Executive Summary

The German real estate market is caught in a high-stakes stalemate. As captured by the sentiment of senior leaders polled at the GRI Institute’s Deutsche GRI 2026, the industry is not experiencing a sudden collapse, but rather a profound freeze.

A decade of easy money has collided with a new reality of elevated debt costs, yet well-capitalised property owners remain stubbornly resistant to accepting steep write-downs - a standoff which has essentially killed the traditional playbook of passive yield compression, leaving the market starving for liquidity and searching for a new catalyst to break the gridlock.

Rather than waiting for a macroeconomic miracle, the industry is undergoing a fundamental shift in its DNA. The survey reveals that survival in this next cycle belongs to those willing to actively manufacture their own upside through tactical repositioning, creative capital structuring, and hands-on asset management.

Ahead of further industry discussions at Europe GRI 2026 Summer Edition, the following barometer breaks down exactly how the market's top players are navigating this structural reset and where they are placing their bets to bridge the gap.

► Read the full Deutsche GRI 2026 Spotlight report here

A decade of easy money has collided with a new reality of elevated debt costs, yet well-capitalised property owners remain stubbornly resistant to accepting steep write-downs - a standoff which has essentially killed the traditional playbook of passive yield compression, leaving the market starving for liquidity and searching for a new catalyst to break the gridlock.

Rather than waiting for a macroeconomic miracle, the industry is undergoing a fundamental shift in its DNA. The survey reveals that survival in this next cycle belongs to those willing to actively manufacture their own upside through tactical repositioning, creative capital structuring, and hands-on asset management.

Ahead of further industry discussions at Europe GRI 2026 Summer Edition, the following barometer breaks down exactly how the market's top players are navigating this structural reset and where they are placing their bets to bridge the gap.

► Read the full Deutsche GRI 2026 Spotlight report here

Key Takeaways

- The German market remains entrenched in a protracted price-discovery phase, characterised by a persistent bid-ask spread and a slow recalibration of asset values.

- Cautious lending from traditional banks has created a significant gap in the capital stack, forcing sponsors to rely on alternative credit and mezzanine financing.

- Investors are pivoting toward active value-add strategies and hands-on asset management, focusing their capital on structurally resilient sectors.

Investment Cycle

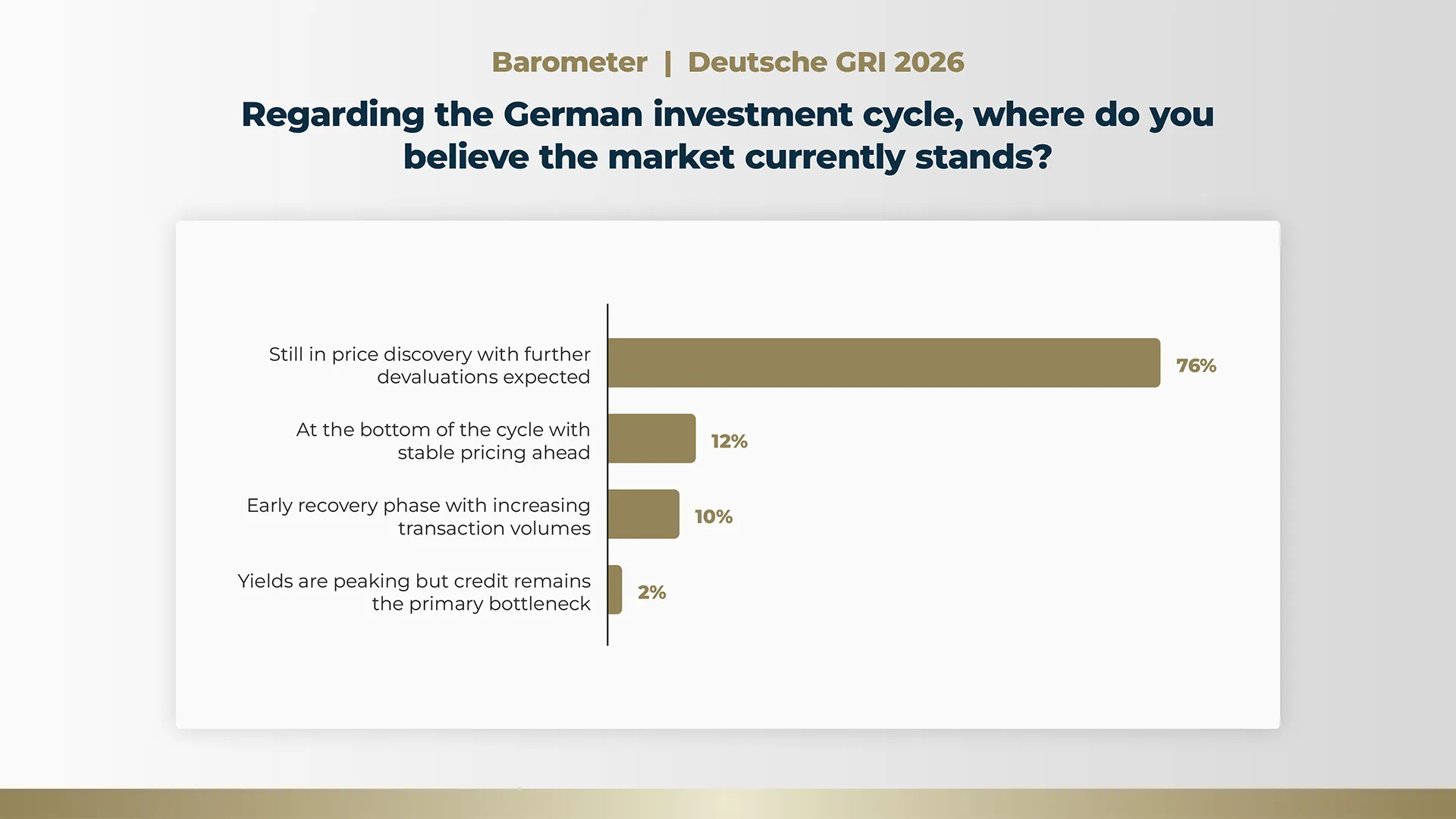

Survey results regarding the German investment cycle reveal a distinctly cautious outlook, with 76% of respondents indicating that the market remains entrenched in a phase of price discovery with further devaluations anticipated.

This overwhelming consensus underscores a lingering lack of confidence, suggesting that the industry has not yet found a stable equilibrium between buyer bids, seller expectations, and transaction volumes.

Only a small fraction of participants believe the market has reached the bottom with stable pricing ahead (12%), or has entered an early recovery phase characterised by increasing transaction volumes (10%).

This sentiment aligns heavily with current market realities, where experts highlight a persistent gap between buyers and sellers, exacerbated by the reluctance of current owners to write down their book values.

In this context, the German market is experiencing a slow-motion correction compared to other European regions, largely because domestic banks and institutional investors have historically been well-capitalised enough to hold onto assets without being forced into immediate distressed sales.

Consequently, transaction volumes remain subdued as participants await a more realistic recalibration of asset values to reflect the higher interest rate environment.

Interestingly, while only 2% of respondents selected peaking yields and credit constraints as their primary answer here, broader discussions confirm that conservative lending restrictions, shifting interest rates, and a lack of core capital are heavily prolonging this price discovery period.

Until sellers are compelled to accept marked-down valuations, either through mounting refinancing pressures or regulatory scrutiny, the real estate sector is expected to remain in this transitional, wait-and-see phase before a genuine transactional recovery can fully materialise.

Debt Challenges

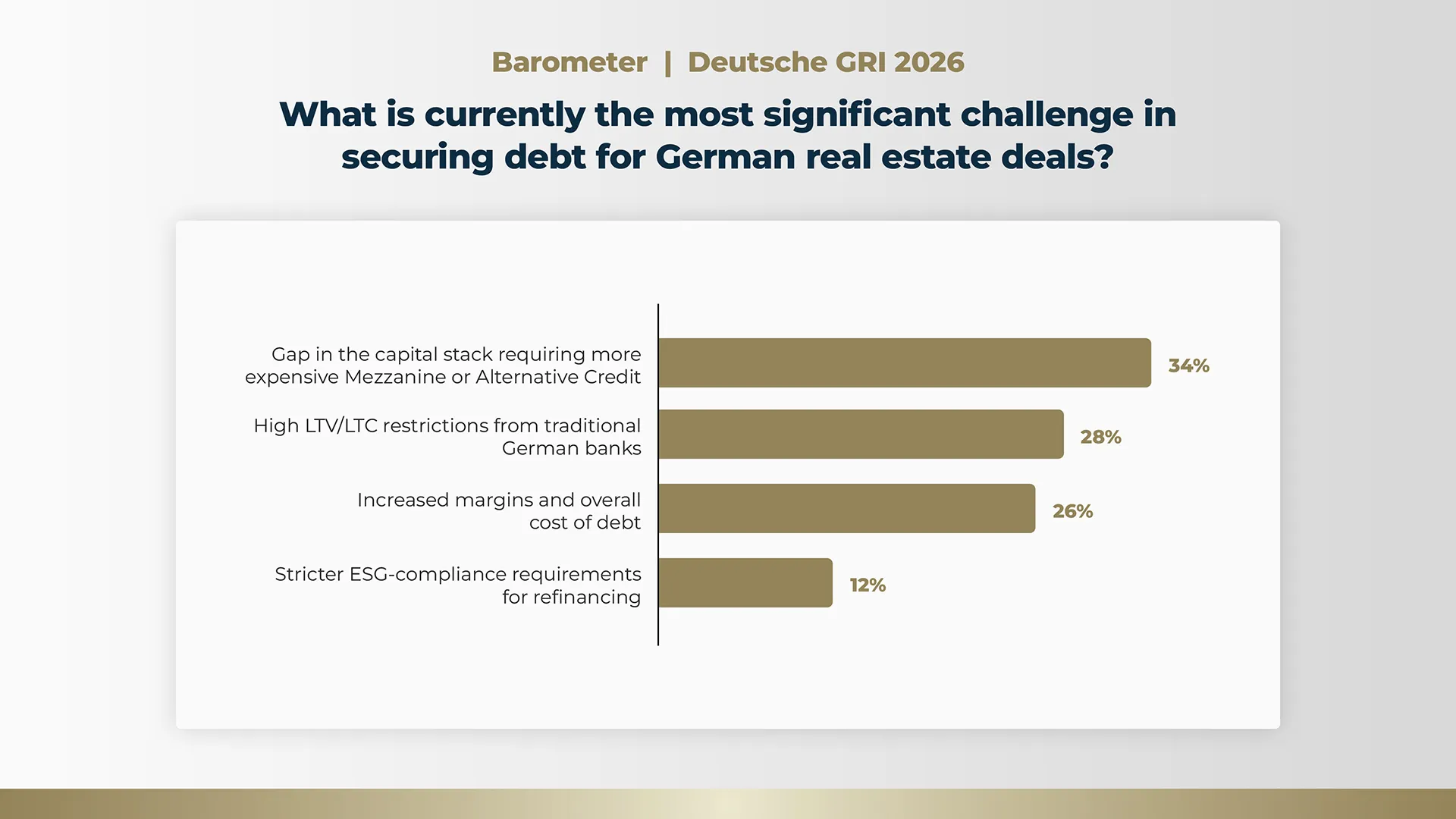

When it comes to securing debt, the results indicate a fragmented landscape, with the largest group of respondents (34%) identifying a gap in the capital stack requiring more expensive mezzanine or alternative credit as their most significant challenge.

Closely following are high loan-to-value (LTV) and loan-to-cost (LTC) restrictions from traditional German banks (28%), and increased margins alongside the overall cost of debt (26%).

Stricter ESG compliance requirements for refinancing represent a smaller, yet notable, hurdle at 12%. This relatively even split among the top three choices illustrates a complex financing environment where borrowers are being squeezed from multiple directions simultaneously.

These findings strongly echo the discussions regarding the evolving role of traditional lenders and the rising necessity of alternative financing. As senior banks pull back their exposure to mitigate risk, LTV and LTC limits have become much more conservative, effectively capping out around 60% to 65% for many development and value-add projects.

To bridge the resulting shortfall, sponsors are increasingly forced to turn to debt funds and mezzanine providers. While these alternative capital sources offer the flexibility needed to get deals done, they significantly drive up the blended cost of capital, often demanding yields of 6%, 7%, or even 8%, compared to senior debt rates that currently hover around 4%.

Furthermore, the overall cost of debt remains a persistent barrier to transaction fluidity. With base rates remaining elevated, borrowing costs have materialised at a level that fundamentally challenges historical business plans, leaving a vast number of deals unable to be refinanced without significant equity injections or lender write-offs.

Additionally, lenders are implementing much stricter underwriting standards, scrutinising sponsor track records, business plan execution capabilities, and ESG compliance more rigorously than in the previous cycle.

As a result, borrowers are navigating a landscape where debt is not only more expensive and less abundant, but also burdened with heavier operational and reporting demands.

Investment Strategies

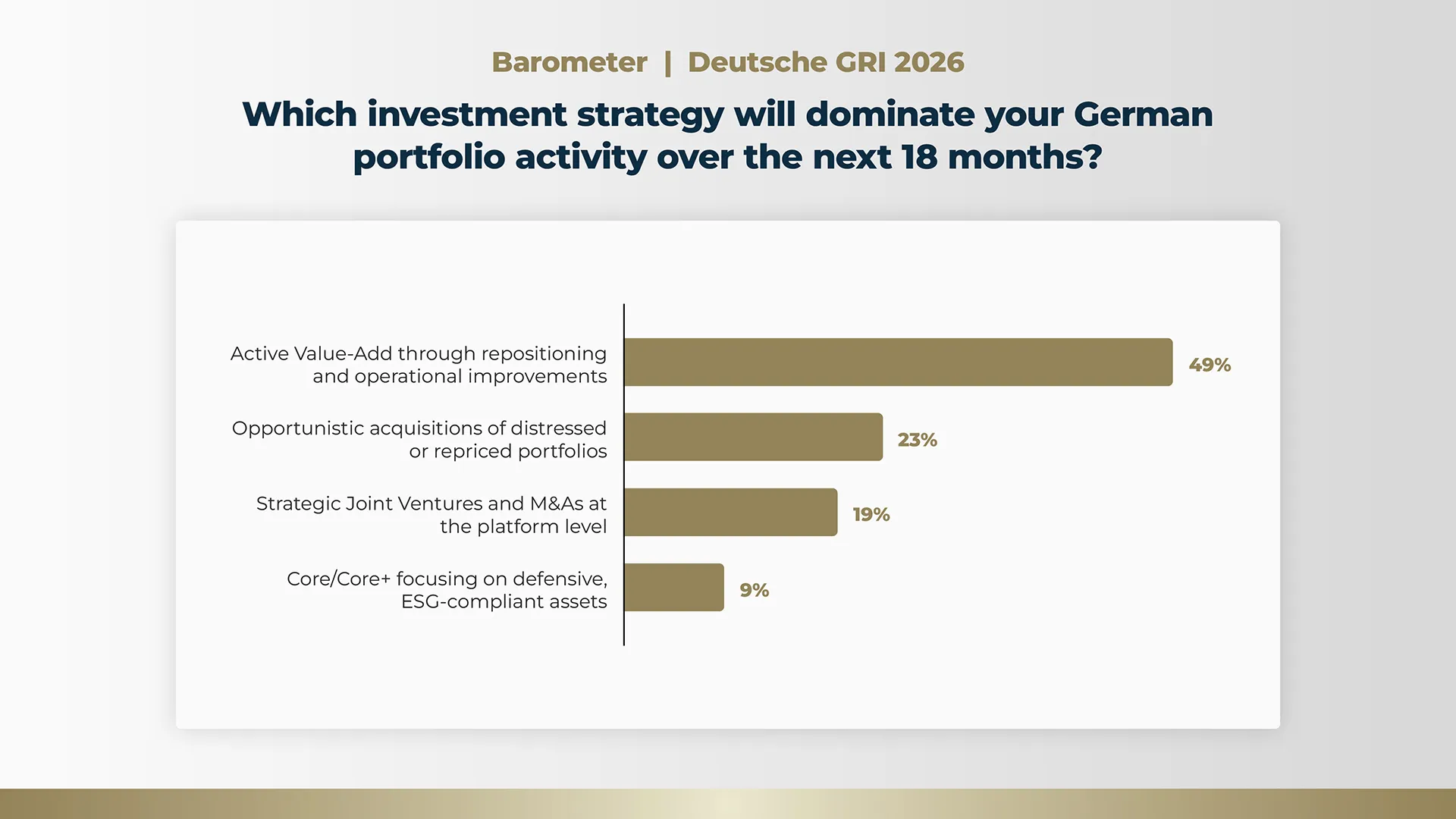

On the subject of investment strategies over the next 18 months, the survey reveals a decisive shift towards hands-on asset management, with nearly half of the respondents (49%) pointing to active value-add approaches as their primary focus - starkly contrasting with the passive styles of the past decade.

As discussed by market participants, the era of relying on easy yield compression and low interest rates to drive returns has ended, meaning that creating genuine alpha now requires intense operational excellence.

Whether it involves converting stranded offices into serviced apartments, executing brownfield logistics developments, or implementing targeted ESG upgrades, investors are prioritising business plans where they can actively control value creation.

Opportunistic acquisitions of distressed or repriced portfolios form the second most popular approach at 23%. With many legacy capital structures currently broken and a significant volume of deals struggling to refinance under the new interest rate environment, buyers with fresh capital are actively hunting for non-performing loans and deeply discounted assets.

Close behind, 19% of respondents plan to rely on strategic joint ventures and M&A at the platform level. This trend is driven by the necessity to pool resources, share risk, and inject structured equity into balance sheets without resorting to highly dilutive capital raises.

Tellingly, only 9% of leaders identified Core or Core+ defensive investments as their dominant strategy. This low figure perfectly encapsulates the current absence of traditional core money in the German market.

Many institutional buyers remain over-allocated to real estate and are waiting for pricing to adjust before deploying fresh capital, so until buyer and seller expectations fully align on core pricing, the market will continue to be heavily steered by players willing to roll up their sleeves and take on operational or restructuring risks.

Asset Classes

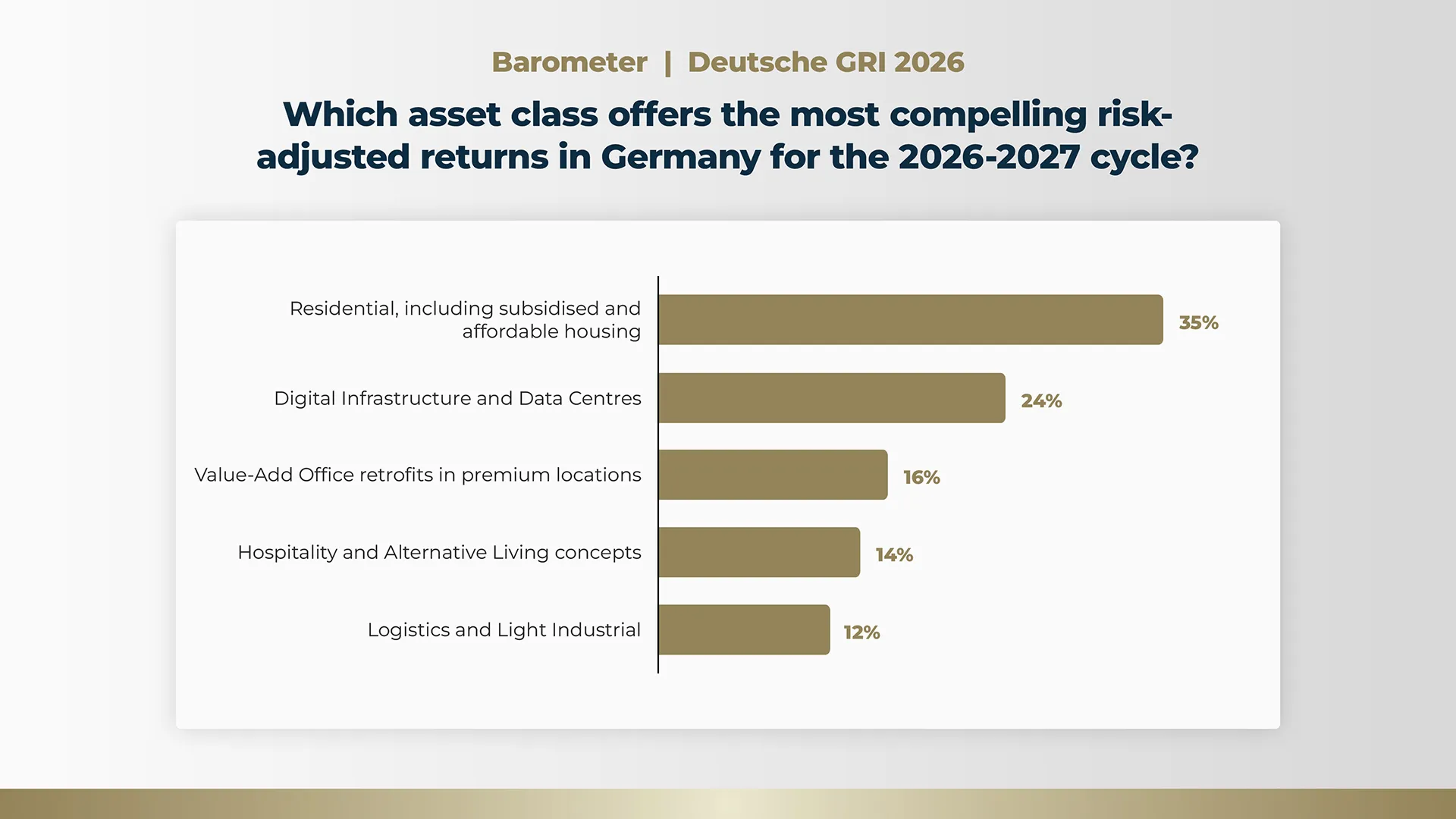

When evaluating the most compelling risk-adjusted returns for the 2026-2027 cycle, industry leaders clearly favour the residential sector, which captured 35% of the survey vote - a sentiment underpinned by Germany's acute housing shortage.

Despite the hurdles of strict rent regulations and elevated construction costs, the sheer structural demand ensures high occupancy rates and resilient cash flows, making both free-market and subsidised affordable housing highly attractive to institutional capital.

Following closely behind, digital infrastructure and data centres secured 24% of the vote, reflecting the sector's rapid evolution from a niche asset class into critical digital infrastructure.

Similarly, 14% of respondents look toward hospitality and alternative living concepts, such as purpose-built student accommodation (PBSA) and serviced apartments. These operational real estate models can deliver robust profit margins and higher yields compared to traditional residential assets, provided investors partner with capable operators to manage the day-to-day complexities.

The remaining votes highlight a targeted approach to commercial assets, with 16% favouring value-add office retrofits in premium locations and 12% selecting logistics and light industrial.

While the broader office market faces severe structural headwinds, discussions revealed that well-located central business district (CBD) assets remain highly financeable and offer strong downside protection for investors willing to implement active ESG upgrades.

Meanwhile, logistics, once the unquestioned darling of the German real estate sector, has seen its rapid growth moderate. Investors maintain strong conviction in light industrial parks and urban mid-box facilities, but they are increasingly turning to brownfield redevelopments to circumvent land scarcity and deliver essential supply chain infrastructure.

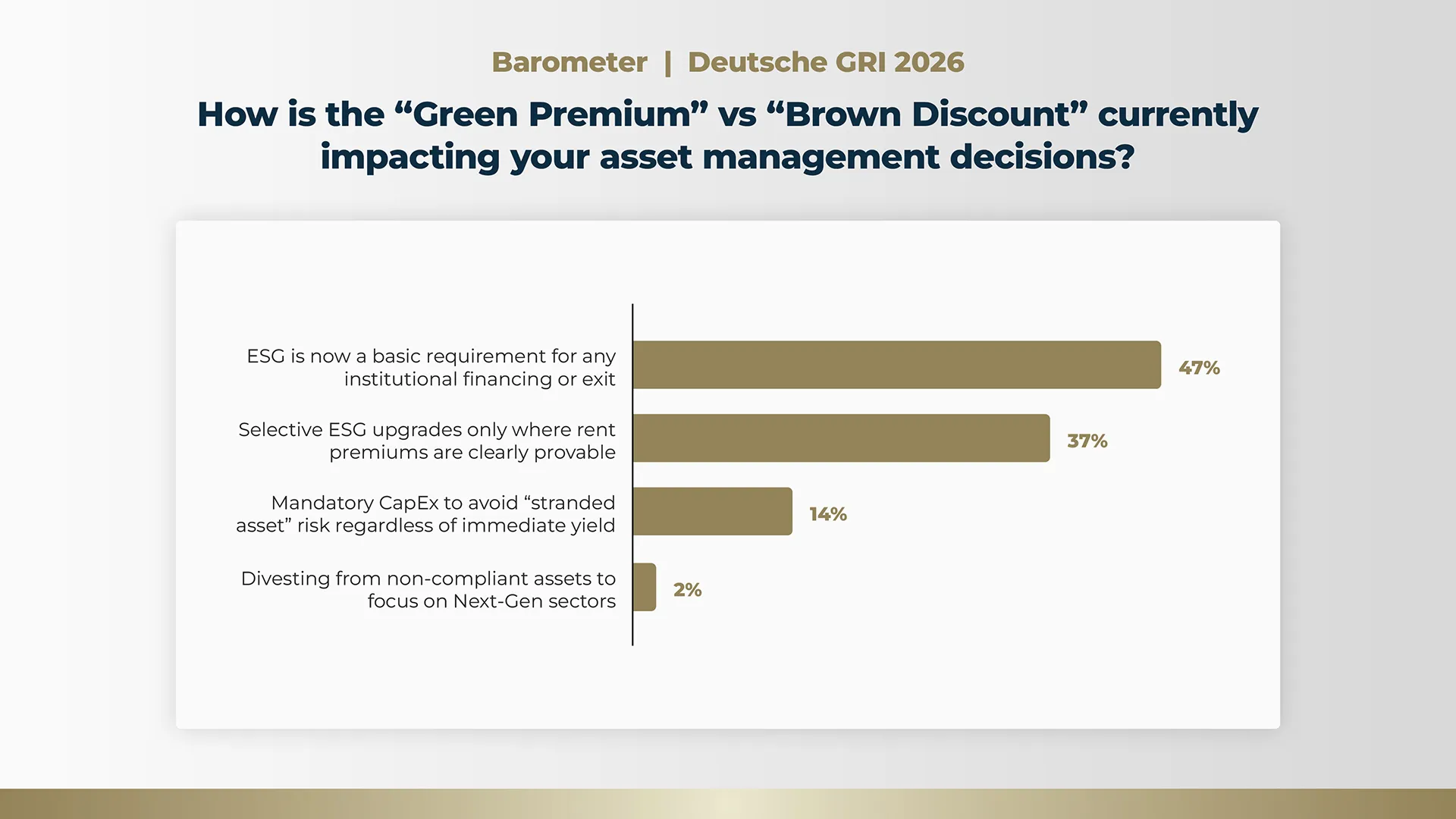

Green Premium vs Brown Discount

The impacts of green premiums versus brown discounts show that ESG compliance has shifted from an optional value driver to a fundamental prerequisite, with 47% of respondents identifying it as a basic requirement for any institutional financing or exit.

This aligns with the broader market reality where traditional banks and debt funds are increasingly unwilling to finance non-compliant assets, effectively rendering brown properties unbankable.

Institutional investors are increasingly bound by strict mandates that prohibit them from acquiring assets without clear sustainability credentials, making achieving a basic level of green compliance no longer just about seeking a premium, but rather about maintaining market liquidity and ensuring an asset can be traded or refinanced at all.

Despite this regulatory and financial pressure, asset managers remain highly pragmatic about capital expenditure, as evidenced by the 37% who are pursuing selective ESG upgrades only where rent premiums are clearly provable.

With construction costs remaining stubbornly high and overall margins squeezed by elevated interest rates, investors are hesitant to undertake massive retrofits if the underlying business plan cannot support the required financial outlay.

However, 14% of leaders feel compelled to undertake mandatory upgrades to avoid stranded asset risk, regardless of the immediate yield. This highlights the difficult balancing act property owners face, as they must inject capital to keep older assets legally and commercially viable, even when the short-term financial returns are difficult to justify.

Interestingly, only a marginal 2% of respondents are choosing to divest from non-compliant assets to focus on next-generation sectors. This exceptionally low figure reflects the severe pricing gap and the lack of liquidity for outdated properties in the current market.

Because selling brown assets today would require owners to accept steep discounts and significantly write down their book values, most are opting to hold onto their properties and explore creative energy management strategies instead.

Rather than taking a substantial financial hit through an immediate fire sale, asset managers are relying on targeted technological innovations, operational optimisations, and phased improvement plans to slowly bridge the gap between their existing stock and future market standards.

Conclusion

Ultimately, the German real estate market is undergoing a structural paradigm shift, transitioning away from an era of passive yield compression into a cycle that demands intense operational agility and financial creativity.Going forward, the industry is bracing for a prolonged, grinding recalibration rather than a sudden wave of distressed fire sales. Because well-capitalised owners remain reluctant to accept steep discounts, the market will increasingly be defined by a "roll-up-your-sleeves" approach, where stakeholders hold onto assets and incrementally adapt them to shifting market realities.

Success in this next phase will heavily favour active operators over traditional capital allocators. The market's eventual recovery will not be driven by a sudden macroeconomic tailwind, but rather by sponsors who can systematically unlock value in a capital-constrained environment.

Market leaders will be defined by their ability to creatively bridge complex funding gaps with alternative credit, pragmatically implement ESG upgrades to protect asset liquidity, and pivot decisively toward structurally resilient sectors such as residential housing and digital infrastructure.

► Read the full Deutsche GRI 2026 Spotlight report here

► Discover the full range of insights from the Deutsche GRI 2026 C-Circle Gathering here

This survey was conducted among the senior real estate industry leaders in attendance at Deutsche GRI 2026.