GRI Institute

GRI InstituteCEE GRI 2026 Barometer: Shifting strategies for the next investment cycle

Exclusive survey results reveal industry perspectives on collaborative restructuring, hyper-selective regional conviction, and asset-class pivots

July 6, 2026Real Estate

Written by:Rory Hickman

Executive Summary

The Central and Eastern European (CEE) real estate market is transitioning to a highly disciplined, operator-led paradigm.

As captured by senior leaders at the GRI Institute’s recent CEE GRI 2026 gathering in Warsaw, investment conviction has become hyper-selective, anchoring around hubs with deep local liquidity to underwrite regional risk.

Instead of a market defined by distress, a narrative of collaborative endurance is emerging. Industry leaders are managing a looming maturity wall through strategic restructuring rather than panic selling, while confronting a stark K-shaped polarisation across legacy stock.

Success in this cycle is less about broad sector bets and more about pure operational agility - solving for regional supply gaps, executing complex asset conversions, and driving cash flows.

Ahead of further regional discussions at Europe GRI 2026 - Summer Edition in Paris on 9th-10th September, this barometer outlines the strategic mindset and structural resets shaping CEE real estate’s next investment cycle.

► Access more insights from CEE GRI 2026 in our full event report

As captured by senior leaders at the GRI Institute’s recent CEE GRI 2026 gathering in Warsaw, investment conviction has become hyper-selective, anchoring around hubs with deep local liquidity to underwrite regional risk.

Instead of a market defined by distress, a narrative of collaborative endurance is emerging. Industry leaders are managing a looming maturity wall through strategic restructuring rather than panic selling, while confronting a stark K-shaped polarisation across legacy stock.

Success in this cycle is less about broad sector bets and more about pure operational agility - solving for regional supply gaps, executing complex asset conversions, and driving cash flows.

Ahead of further regional discussions at Europe GRI 2026 - Summer Edition in Paris on 9th-10th September, this barometer outlines the strategic mindset and structural resets shaping CEE real estate’s next investment cycle.

► Access more insights from CEE GRI 2026 in our full event report

Key Takeaways

- Poland dominates regional investment conviction, drawing the vast majority of capital due to its exceptional scale, liquidity, and deep pools of local capital.

- Sponsors are overwhelmingly favouring collaborative "amend-and-extend" strategies over aggressive liquidations to navigate the looming maturity wall.

- Capital is pivoting towards resilient, high-cash-flow sectors including retail parks and living assets, whilst obsolete office spaces are increasingly targeted for functional conversion.

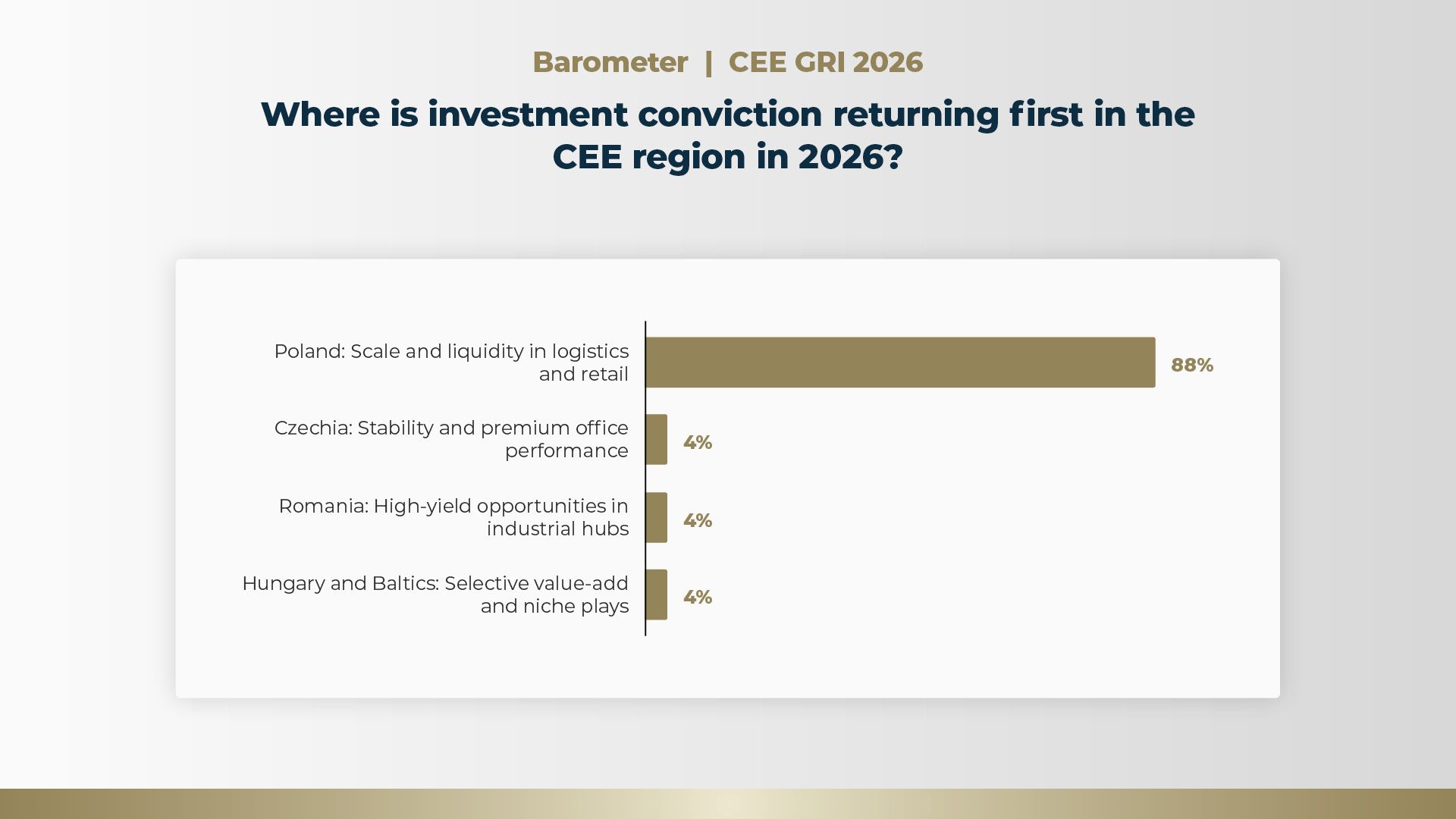

► Regional Investment Conviction

According to the CEE GRI 2026 Barometer survey conducted among senior real estate industry leaders, investment conviction in the Central and Eastern European region is overwhelmingly concentrated in Poland.

An emphatic 88% of respondents identify Poland's scale and liquidity in logistics and retail as the first harbour for returning investment conviction. This decisively outpaces Czechia, Romania, and the Baltics, which each captured just 4% of the vote.

The broader CEE region maintains a resilient 1.1% growth premium over Western Europe, largely propelled by an emerging middle class with increasing purchasing power. Poland exemplifies this robust macroeconomic backdrop.

While the Polish logistics market wrestles with some downward pressure on rents due to a lack of supply barriers, its exceptionally high occupier demand secures its position as a top-tier European hub.

The deep pools of local capital provide a critical stabilising force that underwrites localised risk, keeping Polish retail and industrial assets highly liquid and attractive despite conservative international allocations elsewhere.

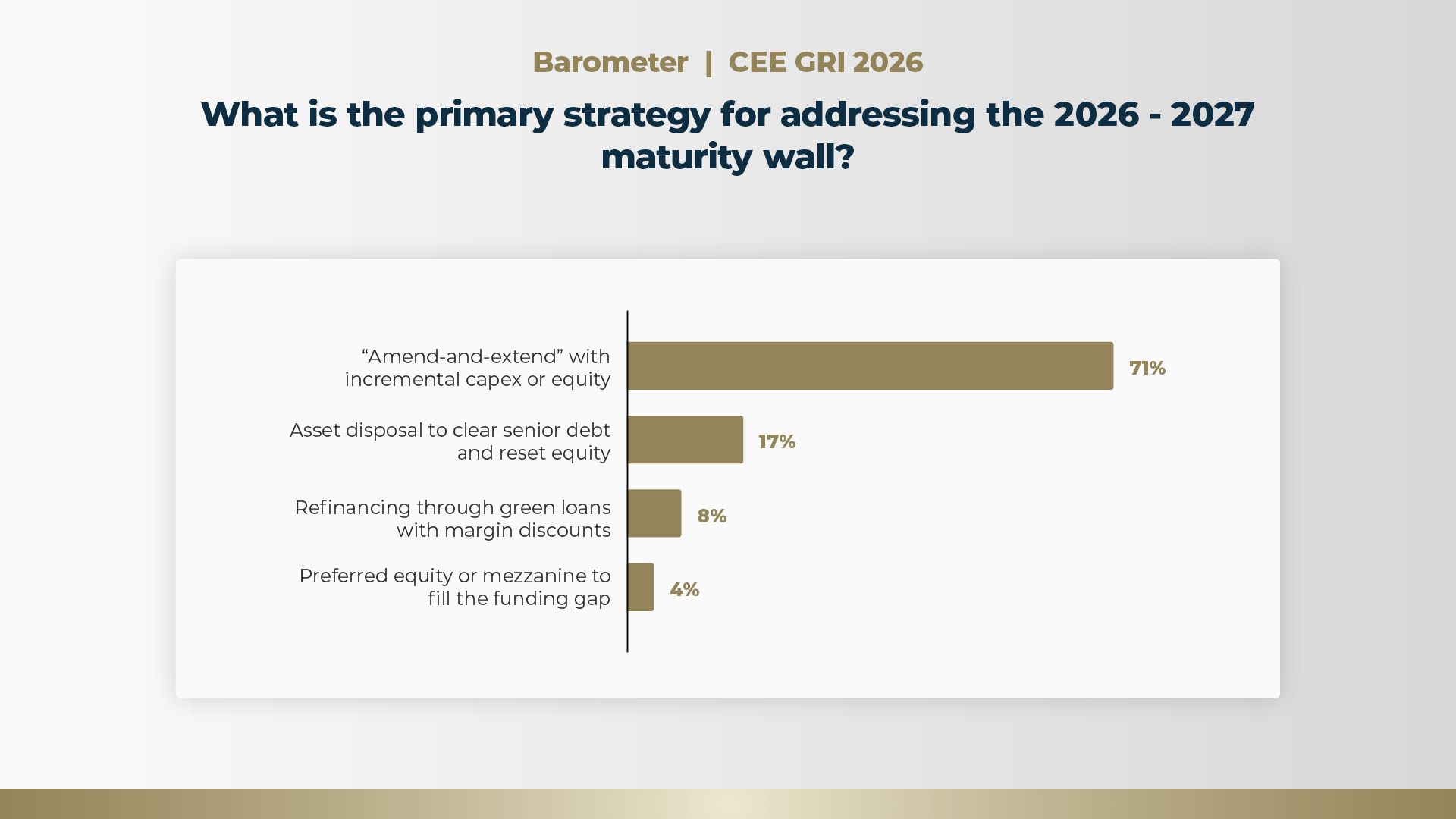

► 2026-2027 Maturity Wall

As the 2026-2027 maturity wall looms, regional real estate sponsors are heavily favouring collaborative restructuring over aggressive liquidations. The survey reveals that 71% of industry leaders view "amend-and-extend" structures, bolstered by incremental capex or equity, as their primary strategy for bridging funding gaps.

Asset disposal to clear senior debt trails at 17%, while green loan refinancing (8%) and mezzanine gap-filling (4%) remain peripheral tactics. This preference for extension aligns with the intense competition currently defining the CEE debt landscape.

Local institutions and foreign lenders are engaged in severe margin compression, driving bank terms towards borderline profitability thresholds and creating highly competitive refinancing conditions.

Rather than defaulting or dumping assets into a volatile market, owners are leveraging normalised interest rates and restored bank balance sheets to negotiate favourable extensions, preserving asset value and equity in the face of lingering inflation and localised recessionary pressures.

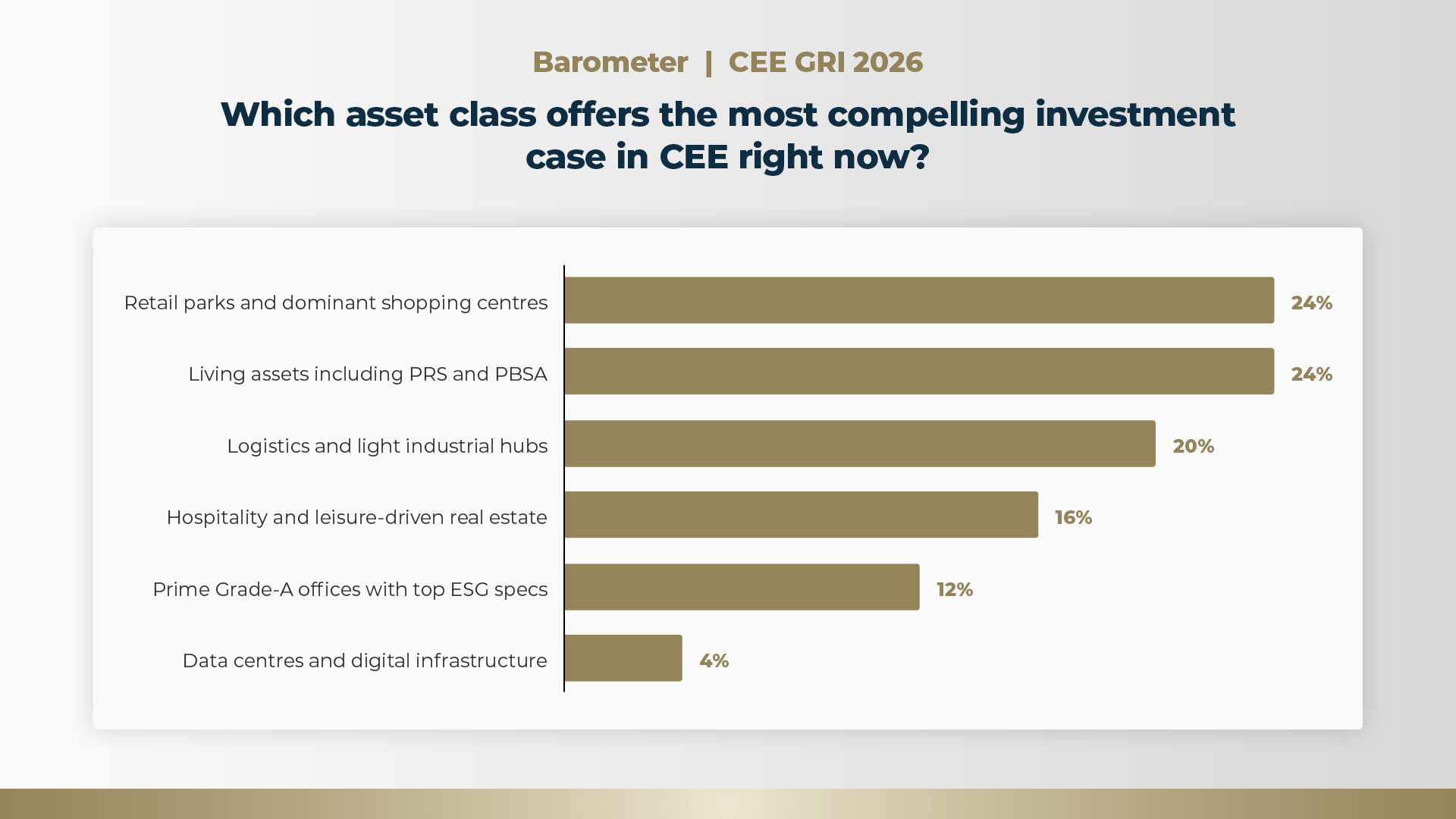

► Asset Class Performance

Capital allocations in the current cycle are pivoting towards sectors that blend counter-cyclical stability with high operational cash flows.

The survey highlights a tie for the most compelling CEE asset class, with retail parks/dominant shopping centres and living assets (including PRS and PBSA) each securing 24% of investor preference. Logistics hubs and hospitality real estate follow closely at 20% and 16% respectively, while prime Grade-A offices (12%) and data centres (4%) lag.

The strong conviction in retail parks stems from a persistent regional convenience gap; CEE markets maintain significantly less retail space per capita than Western Europe, making these assets highly resilient, low-cost to operate, and favoured by credit committees. Simultaneously, demographic shifts are driving capital into purpose-built living assets.

Conversely, while data centres present immense long-term recurring revenue potential, their lower ranking likely reflects acute bottlenecks in power accessibility and the looming EUR 250 billion energy grid transition required to make them viable.

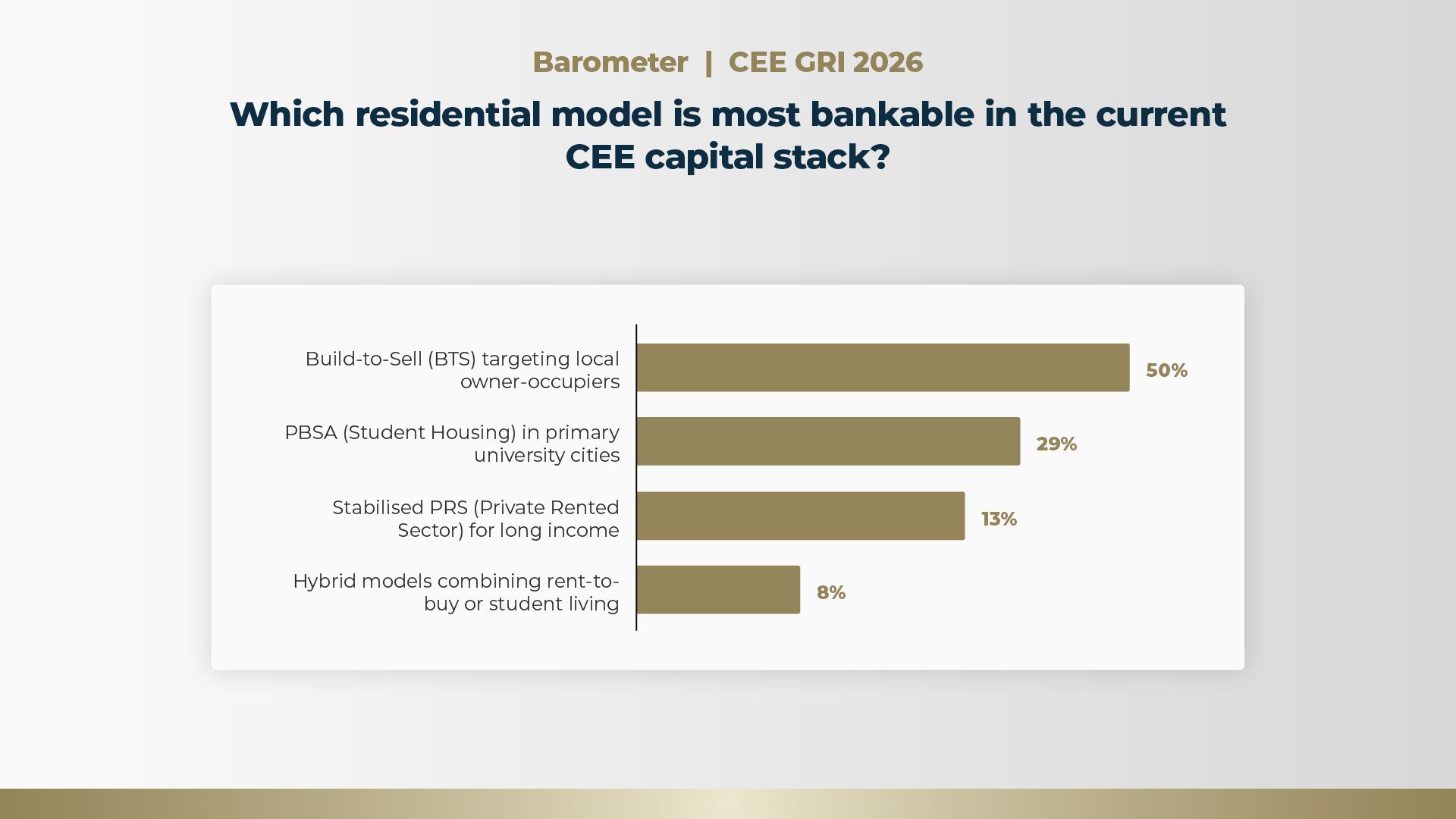

► Residential Models

Within the living sector, the path to reliable capital is starkly defined by rapid returns and lucrative margins over long-term holds.

Exactly half of the respondents (50%) pinpoint Build-to-Sell (BTS) targeting local owner-occupiers as the most bankable residential model in the current capital stack. Purpose-Built Student Accommodation (PBSA) captured 29%, while stabilised Private Rented Sector (PRS) formats received 13% and hybrid models lagged significantly at 8%.

This banking appetite perfectly mirrors the reality of CEE development margins, which frequently hit between 30% and 50% for BTS projects. Individual apartment sales generate robust double-digit internal rates of return that institutional rental frameworks simply cannot match in the current climate.

Institutional PRS is heavily burdened by skyrocketing prime land acquisition costs - often hovering around EUR 2,000 per square metre - and stubborn construction outlays. Consequently, lenders and developers are favouring the immediate liquidity of individual unit sales or the highly resilient, densely concentrated cash flows of student housing.

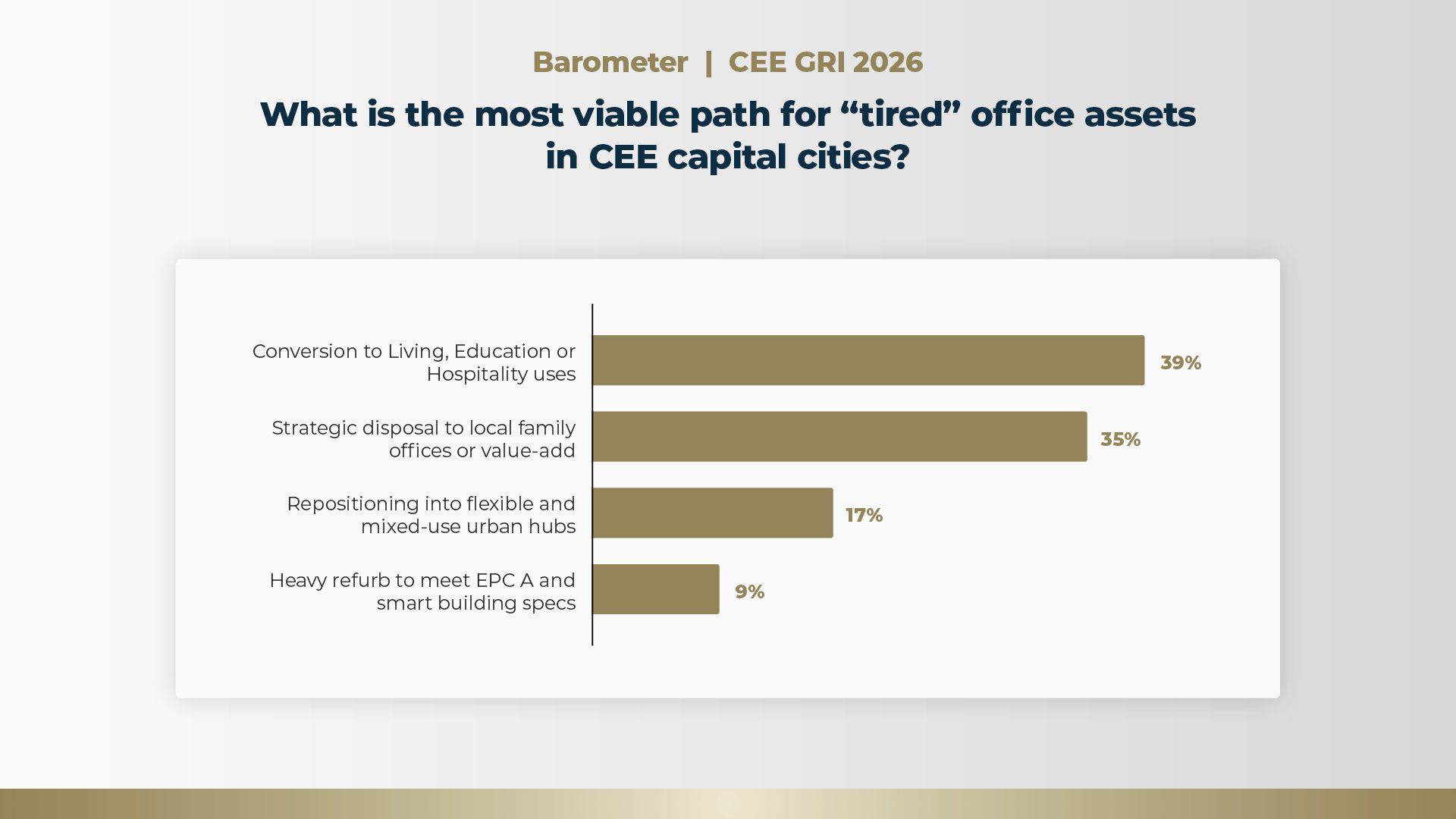

► Office Assets

The CEE office market is defined by a fierce K-shaped polarisation, leaving secondary and ageing assets in a precarious position as prime CBD vacancy drops below 5%.

For these "tired" capital city offices, 39% of survey respondents believe functional conversion to living, education, or hospitality uses is the most viable path forward. Strategic disposal to local family offices (35%) is the second most favoured route, while repositioning into mixed-use urban hubs received 17% of votes and heavy refurbishments to meet EPC A standards attract only 9% of the consensus.

This data underscores a critical tipping point in the physical degradation of legacy stock. Rather than sinking extensive capital into cosmetic upgrades for 30-year-old structures with uncompetitive layouts, opportunistic asset managers are executing aggressive value-add "flex" strategies.

Despite regulatory bottlenecks and deep floor plates that compress leasable efficiency, repurposing obsolete multi-tenant buildings into residential units or upscale hotels offers experienced operators a chance to capture steep arbitrage discounts and unlock superior IRR thresholds exceeding 20%.

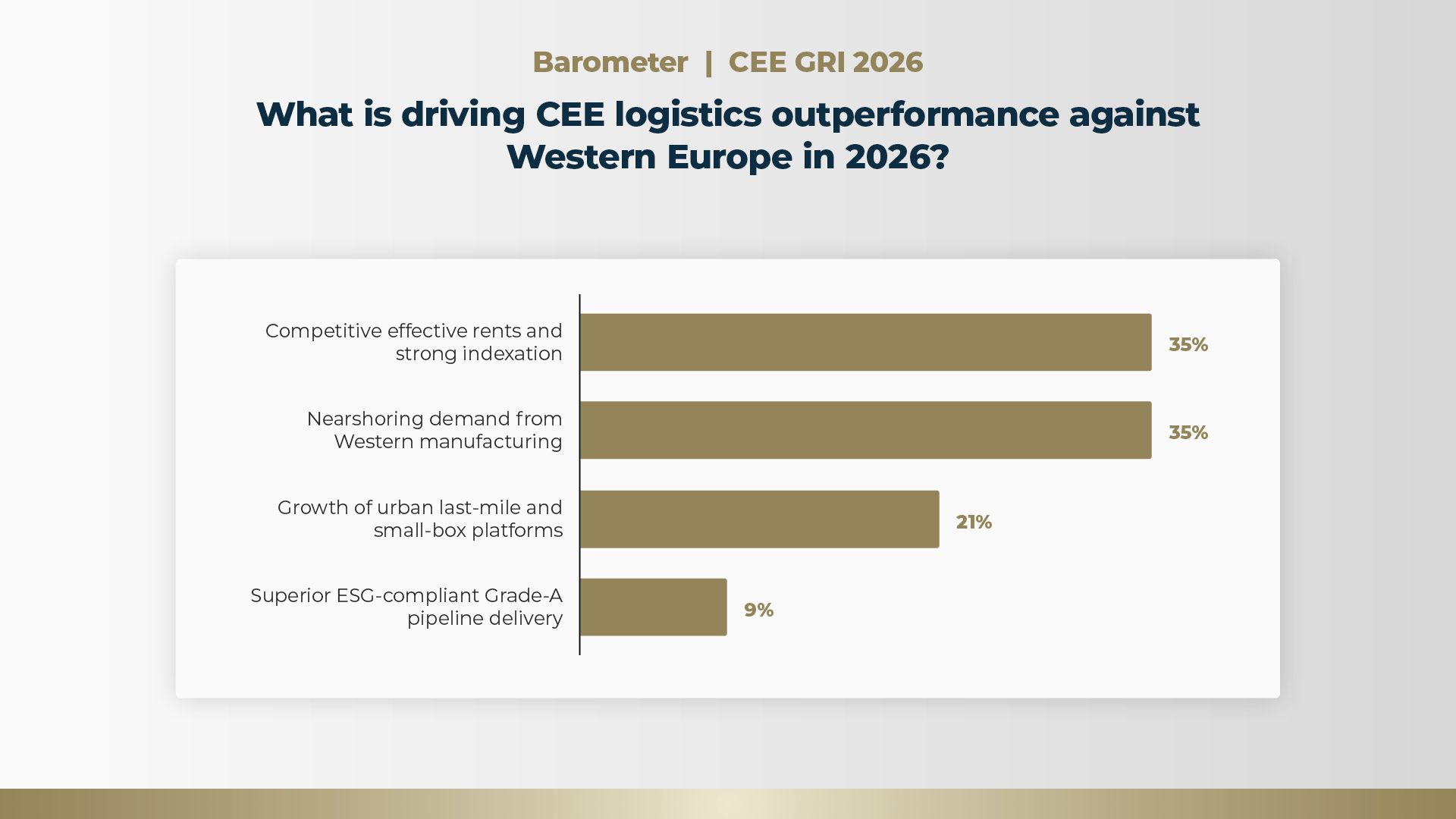

► Logistics Outperformance

The sustained outperformance of the CEE logistics sector against its Western European counterparts is being driven by a duality of localised pricing power and shifting global supply chains.

According to the barometer, competitive effective rents tied to strong indexation and nearshoring demand from Western manufacturing are the twin engines of this growth, tying at 35% each. The growth of urban last-mile platforms accounts for an additional 21%, while ESG-compliant Grade-A pipeline delivery received just 9%.

Despite a notable 20% to 25% divergence between headline and effective rents - necessitating heavy landlord incentives - the market's underlying fundamentals remain incredibly robust.

Furthermore, nearshoring has brought manufacturing and associated storage needs closer to core European consumer bases, while macroeconomic factors, such as a massive ramp-up in regional defence spending, are providing secondary stimulus for vast storage facilities.

With last-mile logistics in premium hubs such as Warsaw gaining rapid traction due to land scarcity, the sector maintains formidable resilience even as occupiers increasingly demand complex ESG and green energy infrastructure.

► Conclusion

Taken together with discussions at CEE GRI 2026, these survey results signal a definitive transition from opportunistic capital growth to a highly disciplined, operator-led investment paradigm.Going forward, the regional market will no longer reward passive ownership; success belongs to players capable of mastering localised operational complexity, executing complex functional conversions, and managing the infrastructure bottlenecks of a massive green energy transition.

As international funds remain selective, deep local capital networks, particularly across Poland and Czechia, will increasingly dictate regional liquidity and underwriting standards, while, ultimately, this stark K-shaped polarisation demonstrates that long-term resilience requires deep asset management flexibility, strategic agility, and a strict corporate flight to quality.

► Discover the full range of insights from the CEE GRI 2026 Spotlight report here

This survey was conducted among the senior industry leaders attending CEE GRI 2026.

Check out all upcoming GRI Institute Europe gatherings here.