Who's who in Antioquia's infrastructure: the players shaping Medellín's pipeline

With over $1.69 trillion pesos approved for the Tren del Río and major road megaprojects underway, Antioquia cements its role as Colombia's second infrastructur

Executive Summary

Key Takeaways

Antioquia is no longer competing with Bogotá just for political capital: it's competing for financial capital

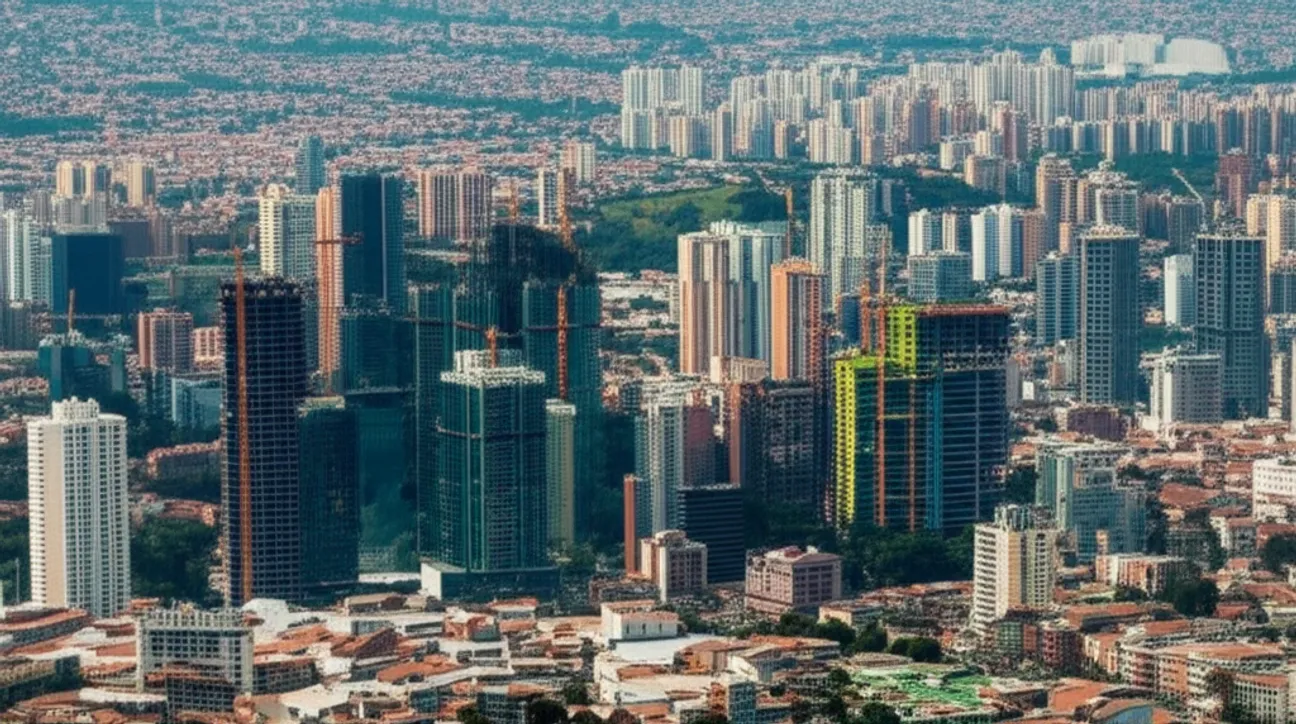

For decades, Colombia's infrastructure debate revolved around Bogotá and its metropolitan area. Fourth-generation (4G) road concessions, planned railway corridors and airport expansions concentrated attention — and resources — in the center of the country. That map is changing. Antioquia, with an approved departmental budget of $6.8 trillion pesos for fiscal year 2025 (according to the Departmental Assembly of Antioquia, Ordinance No. 44 of 2024), has built its own infrastructure agenda that rivals in scale and complexity that of any comparable Latin American region.

What sets the department apart is not just the magnitude of its pipeline, but the institutional sophistication with which it executes it. Entities such as the Medellín Metro, Empresas Públicas de Medellín (EPM) and the Promotora Ferrocarril de Antioquia operate as technical arms with financial structuring capability, international procurement capacity and risk management expertise. In practice, they are the direct counterparts for private capital.

This institutional ecosystem, combined with a pipeline spanning mass transit, regional road connectivity, energy and digitalization, makes Antioquia a case study for infrastructure investors and operators across Latin America. However, the relevant question is not whether there are projects — there are — but who the actors are that make the decisions, structure the deals and deploy the capital.

What are the megaprojects that define Antioquia's infrastructure pipeline?

Three projects form the backbone of the department's short- and medium-term infrastructure agenda, each with distinct risk, financing and procurement profiles.

The Tren del Río. In January 2026, the Antioquia Assembly approved exceptional future appropriations of $1.69 trillion pesos to finance Phase 1 of this railway system, which will connect Bello and Barbosa along 29.3 kilometers and six stations, according to data from the Promotora Ferrocarril de Antioquia and the Antioquia Governor's Office as reported by Teleantioquia. The approval of exceptional future appropriations is a long-term fiscal instrument that commits resources from future administrations, signaling a high level of political will and, at the same time, a risk of reversal in the event of government changes. The Tren del Río is not just a mobility project: it is a bet on reconfiguring the Aburrá Valley's economy northward, integrating municipalities that currently depend on the road corridor as their only functional connection to Medellín.

The Metro de la 80. The contract award to the Unión Temporal Metro de la 80, formed by CRRC and Mota-Engil, marked a milestone in mass transit infrastructure procurement in Colombia, according to information from the Medellín Metro. The presence of CRRC, the world's largest rolling stock manufacturer, and Mota-Engil, a Portuguese group with extensive civil works experience in Latin America, reflects Antioquia's ability to attract top-tier international consortia. This project extends the metro network westward into the Aburrá Valley, a corridor with high population density and unmet transport demand.

The Guillermo Gaviria Echeverri Tunnel (Toyo). With the opening of Phase 1 projected for 2026, according to the Antioquia Governor's Office, this project aims to reduce travel time between Medellín and the Urabá region to 4.5 hours. The connection to Urabá is no minor detail: it is the logistics corridor linking the department's interior to the Gulf of Urabá, a potential port and agroindustrial hub. Road infrastructure toward Urabá is, in essence, export competitiveness infrastructure.

Taken together, these three projects form a multisectoral pipeline that demands diverse technical capabilities: railway engineering, tunneling, urban mass transit and regional logistics. No single operator or contractor can cover them all, which creates a competitive market with multiple entry points for private capital.

Who are the financiers and operators competing for the Antioquia market?

Antioquia's infrastructure ecosystem is not limited to construction contractors. It involves a value chain that includes financial structurers, investment funds, urban developers and macroeconomic analysts whose readings of the Colombian environment directly influence capital allocation decisions.

Munir Jalil, Managing Director and Chief Economist for the Andean Region at BTG Pactual (according to BTG Pactual / GRI Institute), represents the type of macro intelligence that institutional investors consult before entering regional markets like Antioquia. His analysis of Colombia's fiscal cycle, exchange rate outlook and sovereign risk appetite directly affects the cost of capital for departmental infrastructure projects. In an environment where exceptional future appropriations commit long-term resources, the perspective of economists with access to investment banking data flows is a strategic input, not a supplement.

Juan Carlos Ostos, Managing Partner and CEO of Valfort, with prior experience in funds such as CINUK and MIRA (according to GRI Institute), embodies the profile of an infrastructure fund manager with a track record in structuring investment vehicles for long-term assets. Firms like Valfort operate at the intersection of international institutional capital and local projects, identifying opportunities where the risk-return profile justifies entry. Ostos's experience in infrastructure-mandated funds positions players like Valfort as potential conduits for capital into Antioquia's pipeline.

The Antioquia market also attracts attention for its mixed urban development component. The expansion of mass transit lines generates real estate appreciation corridors that interest developers and investors in the real estate sector. Real estate investment firms and urban project developers are closely watching how the metro extension and the Tren del Río are redefining the Aburrá Valley's value geography.

This convergence between transport infrastructure and urban development is a distinctive feature of the Antioquia market. It is not just about building rail lines or tunnels, but about capturing the value that infrastructure generates in its immediate surroundings.

Can Antioquia sustain its pipeline without structured private financing?

The short answer is no. The approval of $1.69 trillion in future appropriations for the Tren del Río demonstrates fiscal commitment, but future appropriations are a mechanism for committing future public spending, not a substitute for private investment. To close the financing gap of a pipeline that includes mass transit, road connectivity and energy projects, Antioquia needs public-private partnership (PPP) frameworks, project finance and institutional fund participation.

The challenge is not just about the volume of capital, but about structure. Colombian regional projects face a higher perceived risk premium than national projects, partly due to lower international visibility and partly due to dependence on subnational political decisions. Building a track record of successful execution — such as that of the Medellín Metro with the Metro de la 80 award to an international consortium — is the most valuable asset Antioquia has to reduce that premium.

The department has the projects, the institutions and the fiscal framework. What it needs now is an investor ecosystem that knows the territory, understands the risks and has the right time horizon. This is precisely the kind of conversation that takes shape in forums like Infra Antioquia GRI 2026, where public sector decision-makers, international contractors, infrastructure funds and urban developers sit at the same table to evaluate concrete opportunities.

The map is drawn in meetings, not in documents

Antioquia's infrastructure is not decided exclusively through decrees and ordinances. It is decided in conversations between governors and fund directors, between metro managers and rolling stock manufacturers, between chief economists and PPP structurers. Mapping who's who in this ecosystem is not an academic exercise: it is a competitive advantage for anyone looking to participate in the most dynamic pipeline in regional Colombia.

GRI Institute, through its community of infrastructure leaders and its agenda of regional gatherings, serves as a relational intelligence platform for these markets. The data and analysis produced by the institute provide a more granular understanding of investment dynamics in Latin America, beyond the national aggregates that dominate conventional analysis.

Antioquia has moved beyond being a regional promise to become an infrastructure market with scale, institutional strength and execution urgency. The players that position themselves now — contractors, financiers, operators and developers — will define the competitive landscape for the next decade.